- Strong dollar slows stainless steel import bookings

- Surging freights raise landed costs of imports

India’s stainless steel finished market witnessed mixed trends in the week ended 27 May 2026, with overall sentiment remaining firm despite subdued downstream demand. Market participants continued to report cautious buying activity, largely on a need-based basis, as elevated alloy costs, a stronger US dollar, and rising freights kept pricing sentiment bullish.

Import activity remained comparatively slower as rupee weakness and higher dollar-denominated transaction costs reduced import viability. In addition, freights increased sharply amid ongoing geopolitical tensions, further pressuring the landed costs of imported stainless steel products.

At the same time, aggressive policy interventions by Indonesia, the world’s largest nickel producer, continued to support global nickel prices and stainless steel production costs. Production quota controls, export-related restrictions, and proposed taxation reforms aimed at increasing state revenues have tightened overall market sentiment.

Indonesia is also considering a floating export duty and windfall taxes on low-processed nickel products to curb tax leakages and smuggling activities. Market participants noted that these developments have significantly strengthened nickel market fundamentals and maintained upward pressure on stainless steel pricing globally.

On the other hand, global stainless steel producers such as Aperam, Outokumpu, Acerinox increased their monthly surcharges for June amid higher raw material costs and geopolitical concerns.

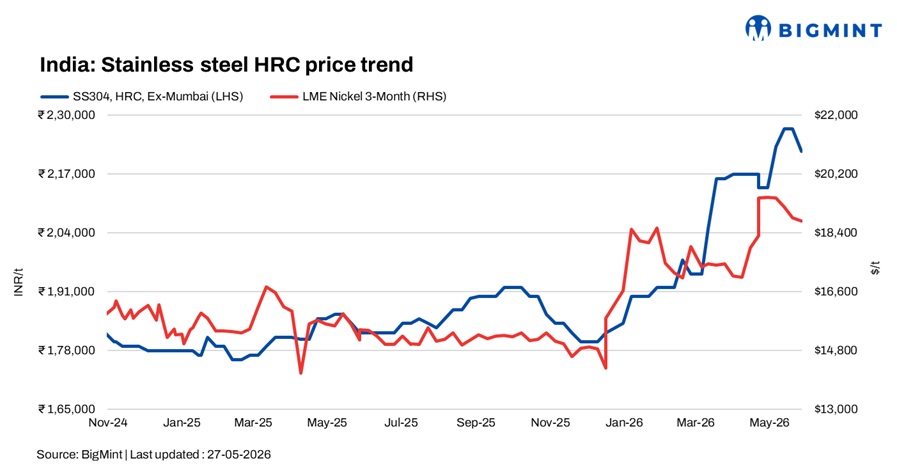

HRC market remains down

India’s stainless steel flat products prices fell w-o-w, despite higher nickel costs, elevated freight rates, and stronger Chinese stainless steel pricing trends.

A market participant stated, “Overall cost pressure remains high. Fuel costs, freight, alloy prices, and Chinese market prices have all increased, keeping domestic sentiment bullish despite moderate demand.”

As per BigMint’s assessment, 304 HRC prices stood at around INR 222,000/t ex-Mumbai (down INR 3,000/t w-o-w), while 316 HRC prices were assessed stable w-o-w at INR 408,000/t ex-Mumbai.

Market participants also indicated that import offers from Asian suppliers remained elevated due to higher raw material and logistics costs, reducing aggressive import bookings in the domestic market.

Finished longs market largely stable

India’s stainless steel longs market remained largely stable during the week, with participants maintaining a cautious stance amid volatile nickel prices. However, steady domestic demand from fabrication and engineering sectors continued to provide underlying support to prices.

BigMint’s benchmark 304L black round bar prices remained stable at around INR 200,000/t ex-Mumbai, while 316L black round bars stood at INR 347,000/t ex-Mumbai.

In the export market, 304 bright bars were at around $2,350/t FOB Nhava Sheva, while 316 bright bars stood near $3,990/t FOB Nhava Sheva.

Weak demand, softer nickel costs pressure China stainless steel market

China’s stainless steel market is expected to remain under pressure in June 2026 amid weaker raw material cost support and sluggish downstream demand. Rising nickel ore shipments from the Philippines and easing Indonesian NPI policy concerns have softened nickel market sentiment, while weak demand from sectors such as real estate and appliances continues to weigh on stainless steel consumption. Although production remains elevated, oversupply concerns and cautious procurement activity are likely to keep stainless steel prices weak in the near term.

Global market sentiment remains policy-driven amid supply concerns

Global stainless steel market sentiment remained firm amid increasing policy-driven supply concerns and elevated production costs. Although Indonesian export offers for 304/2B CRC reportedly declined by around $30/t recently, ending a six-month uptrend, market participants indicated that aggressive Indonesian export control policies and tightening nickel-related regulations continued to support prices globally. In addition, the implementation of Europe’s Carbon Border Adjustment Mechanism (CBAM) is expected to further reshape global stainless steel trade flows and increase compliance-related costs. Traders noted that the market is gradually shifting from demand-led pricing to policy- and supply-driven dynamics, limiting the possibility of any major price correction in the near term.

Raw material scenario

Outlook

India’s stainless steel market is expected to remain firm in the near term, supported by elevated nickel prices, higher freight costs, slower imports, and firm global pricing sentiment. However, weak downstream demand and cautious procurement activity may continue to limit aggressive price movements in the domestic market.

Leave a Reply