- Stainless steel flats prices drop by INR 2,000/t

- LME 3-month nickel prices down 3% w-o-w

India’s stainless steel (SS) finished flats prices dropped slightly by INR 2,000/t w-o-w while longs remained stable this week amid persistent weak demand.

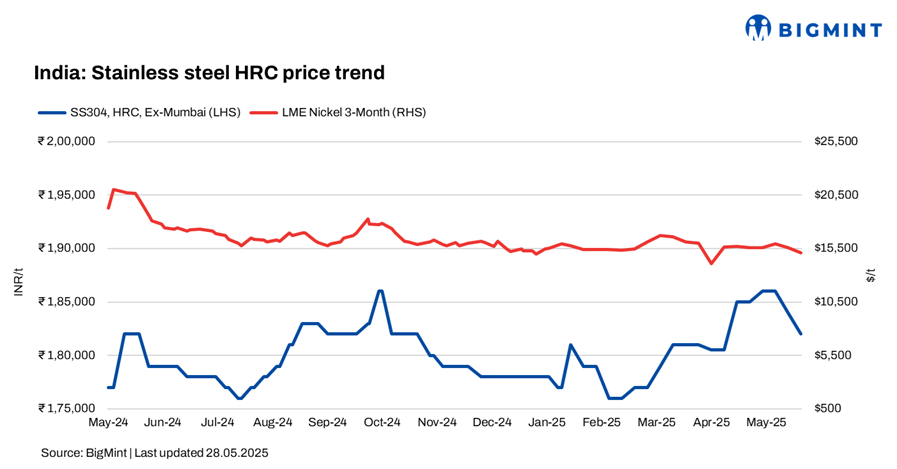

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) dropped by INR 2,000/t to INR 184,000/tonne (t), while 304L (25-100 mm) black round bars stood at INR 160,000/t, both ex-Mumbai.

LME nickel tags dip, Asian NPI stable w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,115/t, down 3.1% against last week’s $15,605/t. Nickel stocks in LME-registered warehouses stood at 199,998 t, a 1% drop compared to 202,098 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 960/t ($133/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $115/t.

Market insights

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 321,000/t and 316 cold-rolled coils (CRCs) at INR 329,000/t ex-Mumbai, both down by INR 2,000/t w-o-w.

A trade source said, “As the monsoon season begins, market activity has slowed considerably. Only need-based buying is happening, especially from Mumbai, where heavy rains have further dampened demand.”

Another source mentioned, “The stainless long segment remains slow and steady, with prices largely unchanged. IF-route mills are operating below full capacity, and overall market sentiment is subdued, with limited trading activity.”

Meanwhile, SS 316L black round bars were priced at INR 270,000/t, while 316L (25-100 mm) bright bars were at INR 286,000-288,000/t, both ex-Mumbai. Furthermore, SS 304 (5-16 mm) wire rods stood at INR 156,000/t ex-Mumbai. Prices of all products were steady w-o-w.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,950/t ($1,936/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices witnessed an increase of INR 56,000/t ($654/t) as compared to the last assessment on 21 May.

Ferro molybdenum prices in India were at INR 2,553,000/t ($29,805/t) exw-India, as per BigMints assessment on 28 May.

Changes in the global market scenario influenced the Indian market as well. Offers went up and trades were also concluded at elevated levels. Additionally, sources indicated that ferro molybdenum and molybdenum oxide import volumes have gone down, supporting the price increase.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,300/t ($1,173/t) exw-Jajpur, largely stable w-o-w.

Ferro silicon: Indian ferro silicon (70%) prices remained largely stable last week, moving down slightly by INR 200/t ($2/t) in comparison to the assessment on 19 May 2025.

As per BigMint’s assessment on 26 May, ferro silicon prices in India were at INR 94,500/t ($1,108/t) exw-Guwahati.

A key domestic buyer, with a monthly procurement volume of around 4,000 t, informed BigMint, there is lot of material coming in from Russia at present and which is available in the domestic market at around INR 93,000-93,500/t ($1,090-1,096/t) exw levels.

Imported ferrous scrap market weak: India’s imported ferrous scrap market remained weak this week, with limited trading activity amid sluggish finished steel demand. EU-origin shredded scrap held steady at $366-368/t CFR Nhava Sheva, while HMS 80:20 was assessed at $348-350/t CFR.

Unseasonal rainfall and availability of cheaper raw material alternatives such as DRI and pellets further dampened buying interest. Mills continued to operate on tight margins and largely avoided fresh bookings, unable to absorb higher scrap costs in the current market environment.

Outlook

In the near term, stainless steel prices are expected to remain stable within a narrow range, with moderate market activity likely to persist.

![]()

Leave a Reply