- Domestic demand remains sluggish, export trade moderate

- Outokumpu surcharge hikes signal stronger global demand

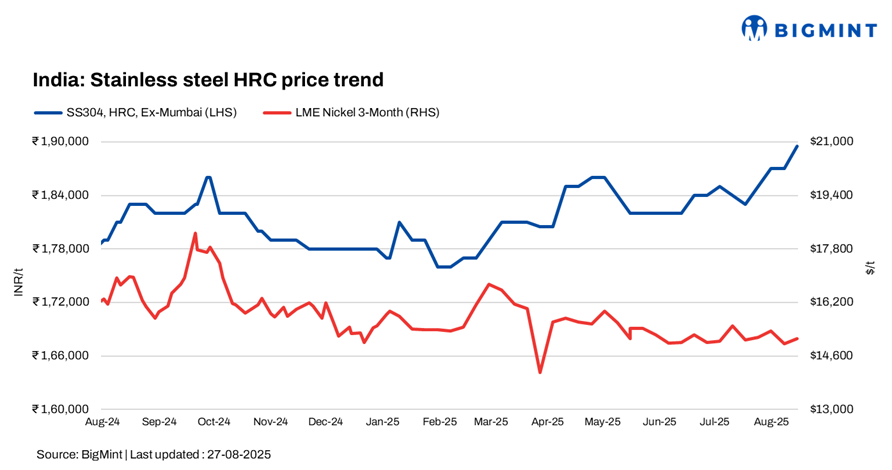

India’s stainless steel prices firmed up this week, supported by higher raw material costs and price hikes from domestic and global producers, though local demand stayed muted amid monsoon disruptions and the festive lull.

BigMint assessed 304-series hot-rolled coils (HRCs) at INR 189,500/tonne (t) ex-Mumbai, up INR 2,500/t w-o-w. 304L black round bars (25-100 mm) rose INR 1,000/t w-o-w to INR 157,000/t.

In the 316 series, HRCs stood at INR 336,000/t, up INR 1,000/t w-o-w, while CRCs held steady at INR 338,000/t.

India’s leading stainless steel coil producer raised prices, effective 20 August, lifting 304 HRC and CRC by INR 5,000/t ($57/t) and 316 grades by INR 12,000/t ($138/t). Traders said the hike reflected surging ferro molybdenum and ferro nickel prices, with the latter supported by a stronger US dollar.

Global sentiment also turned firmer after Outokumpu raised its September alloy surcharges, citing stronger demand and higher input costs. Its 304 series (EN 1.4301) surcharge rose $48/t m-o-m to $2,192/t, 316L (EN 1.4404) jumped $112/t to $3,725/t, and 430 series (EN 1.4016) gained $10/t to $1,149/t. This move by Outokumpu, a leading global producer with an annual melt capacity of 2.55 million tonnes (mnt), was echoed by peers Aperam and Acerinox, which also announced price hikes. Market participants expect this trend to improve Indian market sentiment.

Domestically, however, consumption remained sluggish, as seasonal factors slowed construction and industrial activity. Mills and traders expect demand to pick up ahead of Diwali. Export activity, particularly for longs into the Middle East and Europe, was described as moderate, helping offset weaker local sales.

Secondary stainless steel producers remained under pressure, operating well below capacity amid poor finished sales. Many small- and mid-sized mills shifted towards 200-series production using local scrap to manage costs. “The market is in a wait-and-watch mode, with no clear upward trend in sight,” one long steel manufacturer said, pointing to weak domestic momentum despite firmer global cues.

Market sources also noted heavy rainfall halted Mumbai deliveries temporarily, further weighing on local spot trade.

LME nickel tags up

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,170/t, up 1.5% w-o-w. Nickel stocks at LME-registered warehouses stood at 209,148t, down 1% w-o-w compared to 211,746 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) remained firm w-o-w at RMB 917/t ($128/t). Meanwhile, Indonesian FOB prices of NPI (12-14%) stood at $116/t.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,450/t ($1,873/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were firm at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices rose by INR 57,000/t ($650/t) in comparison to the previous assessment on 20 August. The price hike followed an increase in London Metal Exchange (LME) molybdenum oxide tags and global ferro molybdenum rates.

As per BigMint’s assessment on 27 August, ferro molybdenum prices in India were at INR 3,100,000/t ($35,324/t) exw.

Ferro silicon: Indian ferro silicon (70%) prices declined by INR 1,900/t ($22/t) w-o-w compared with the previous assessment on 18 August. The market remained quiet with limited inquiries, while rising imports further pressured sentiments.

Ferro silicon prices in India were at INR 91,600/t ($1,045/t) exw-Guwahati, as per BigMint’s assessment on 25 August. In Bhutan, prices fell slightly by INR 1,000/t ($11/t) w-o-w to INR 94,000/t ($1,073/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 109,500/t ($1,247/t) exw-Jajpur, range-bound w-o-w.

At OMC’s ferro chrome auction yesterday, 3,050 t were sold from 3,600 t offered. As per reliable sources, the 1,500-t lot (Cr: 60-64%, Si: 4%, 10-100 mm) was booked in the price range of INR 108,700-108,800/t exw, up by INR 9,100-9,200/t over base price. Another 100-t high-carbon lot (Cr: 60-63%, Si: 2%) closed at INR 111,500-111,600/t exw. Tight supplies and a rise in bids at the recent chrome ore auction likely contributed to the increase.

Ferrous scrap: India’s imported scrap market struggled, with very few inquiries, as buyers turned to cheaper local alternatives. Despite HMS 80:20 offers from the UK, Brazil, and West Africa at $330-335/t CFR and shredded at $360-365/t CFR, imports remained sidelined. The availability of competitive domestic scrap continued to refute the case for fresh overseas bookings, keeping market activity muted.

Outlook

India’s stainless steel market is expected to stay range-bound near term, with global surcharge hikes and stronger raw material costs offering support, while domestic demand remains soft due to seasonal disruptions. Exports provide some cushion, but mills remain cautious. Sentiment could improve gradually ahead of Diwali on restocking and firmer alloy prices, particularly ferro molybdenum and nickel.

Leave a Reply