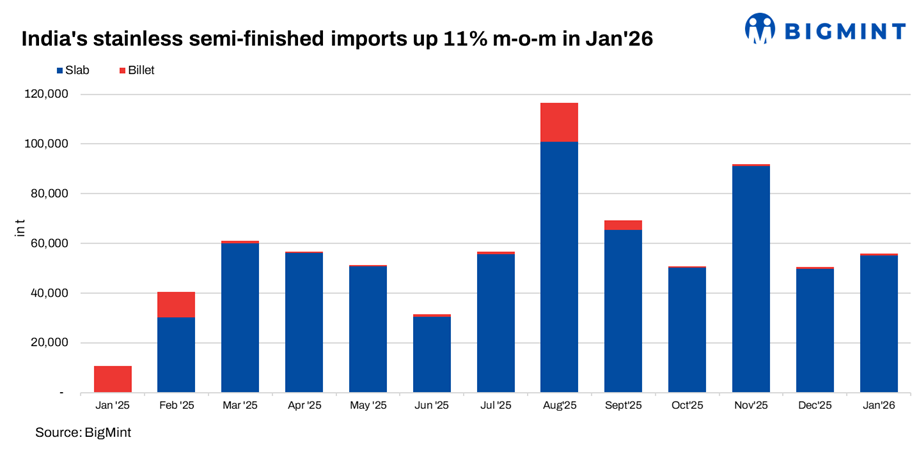

- Slabs dominate import basket at over 98% share

- Billet imports remain marginal amid domestic availability

India’s stainless steel semi-finished imports rose 11% month-on-month to 56,004 t in January 2026, compared with 49,747 t in December, driven almost entirely by slab inflows. Slabs accounted for 55,104 t, or over 98% of total arrivals, underlining a clear structural preference for slab-based rolling over billet procurement.

Indonesian slabs anchor growth

Indonesia supplied the entire slab volume during the month, consolidating its position as India’s primary semi-finished supplier. The trade flow reflects integrated upstream economics in Indonesia, where access to captive nickel and NPI, coupled with large-scale melt shops, continues to offer conversion cost advantages.

For Indian flat producers, importing slabs remains commercially viable amid firm nickel prices and elevated alloy surcharges. Instead of increasing domestic melting – exposed to ferroalloy volatility and power costs – mills opted to secure imported feedstock to optimise rolling margins and working capital cycles.

Industry participants suggest that slab imports are increasingly becoming part of structured intra-group trade flows, ensuring supply stability and shielding domestic operations from raw material price swings.

Additionally, imported slab prices hovered at around $1,575-1,630/t CFR Paradip and Dhamra.

Billet imports shift to Europe

Billet imports increased modestly by 8% m-o-m to 900 t. Sweden emerged as the key supplier, with minor volumes from Spain and France. In January, import prices were heard at $1,500-1,510/t CFR, while domestic billets stood near INR 150,000/t exw-Delhi, keeping arbitrage limited and volumes contained.

Outlook

Slab inflows are expected to remain elevated in the near term as Indonesian melt capacity ramps up further. Billet imports are likely to stay subdued, reflecting adequate domestic supply and a structural shift toward slab-led flat production.

Leave a Reply