- Global alloy surcharges lift stainless steel costs

- Firm dollar, higher inputs keep prices elevated

India’s stainless steel market remained on the higher side during the week, supported by a sharp rise in global stainless prices, elevated raw material costs, and a firm US dollar.

Despite these strong external drivers and a firm dollar, Indian domestic demand remained moderate amid tight liquidity and cautious spot buying, creating a clear divergence between firm price sentiment and subdued physical consumption.

The cost push was reinforced globally, particularly in Europe, where leading producers such as Aperam, Outokumpu, and Acerinox sharply raised February alloy surcharges across key grades including 304 and 316L. These hikes, driven by higher nickel and alloy costs, strengthened global benchmarks and fed into Asian pricing sentiment.

Finished flats

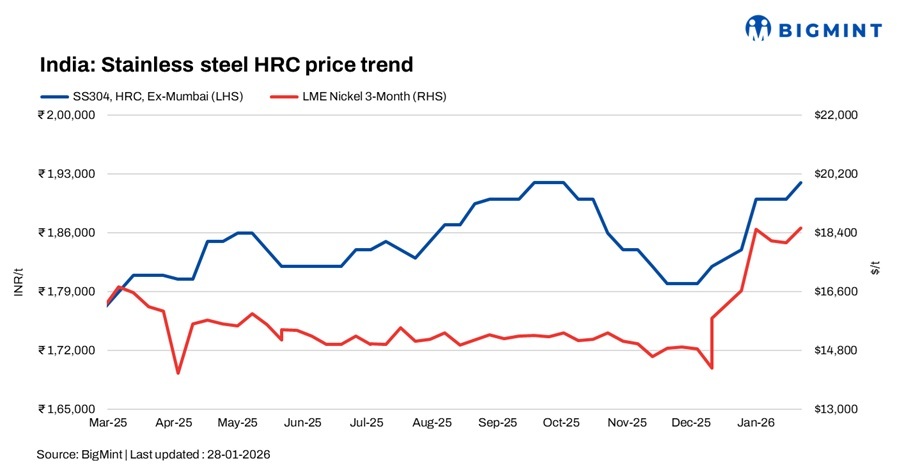

India’s stainless steel flat prices remained bullish, led by currency depreciation and rising input costs.

Additionally, India’s leading stainless steel coil producer announced price hikes effective 22 January, citing strong global cues and higher nickel and copper costs. Prices were raised by INR 2,500/t for 304 HR/CR, INR 4,000/t for 316 HR/CR, INR 1,500/t for 430 grades, and INR 2,000/t for 204Cu grades.

BigMint’s benchmark assessment pegged 304 HRC at INR 192,000/t ex-Mumbai, up by INR 2,000/t while 316 HRC was assessed at INR 340,000/t, up by INR 4,000/t w-o-w. A trader noted that while price sentiment remains bullish, demand is constrained by cold weather, liquidity stress, and geopolitical uncertainty.

Globally, Indonesia’s Tsingshan announced its fourth January hike, lifting 304 export offers by $30/t and pushing cumulative monthly gains close to $180/t. Asian CR prices also strengthened, with Taiwan seeing a rise of $50/t and China $100/t on higher nickel prices.

Cold-rolled stainless steel coil prices in Asia extended their upward trend, supported by rising nickel prices and firm quotations offered by steel mills.

In Taiwan, prices increased as high nickel prices kept mill quotations strong. Meanwhile, tighter nickel production restrictions in Indonesia also provided support to the stainless steel market. Prices are expected to remain at high levels till the Chinese New Year.

Finished longs

Finished longs prices stayed elevated on the back of higher raw material costs, but domestic demand remained sluggish. Market participants were largely cautious, with limited buying activity amid ongoing price volatility.

BigMint’s benchmark assessment for stainless steel 304L (25 to 100 mm) black round bars was at INR 163,000/t ex-Mumbai, up by INR 3,000/t. Meanwhile, SS 316L black round bars were at INR 280,000/t ex-Mumbai, up INR 2,000/t w-o-w.

A market participant said that finished steel demand in the merchant segment remains subdued despite recent price hikes, as buyers are reluctant to commit at elevated levels. The foundry segment also continues to stay weak, offering little support to trading activity in the near term.

Chinese stainless steel, NPI prices

In China, prices of domestic stainless steel 304-grade CRC stood at RMB 15,050/t ($2,167/t) exw, while FOB tags of 304-grade CRC were firm at $2,060/t. Indonesian FOB prices of nickel pig iron (NPI) (12-14%) were at $136/t, and NPI (10-12%) stood at $135/t.

LME nickel prices

Benchmark three-month contract nickel prices on the London Metal Exchange (LME) were at $18,545/t on 28 January, up 3% from $18,060/t in the previous week. LME-registered nickel stocks stood at 285,736 t, largely stable as compared to 283,738 t in the previous week.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices edged up a little by INR 14,500/t ($158/t) as compared to the assessment on 21 January, supported by steady domestic demand, stable supply conditions, and firm LME futures.

As per BigMint’s assessment on 28 January, ferro molybdenum prices stood at INR 2,989,500/t ($32,607/t) exw-India.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices remained steady w-o-w at INR 115,000/t exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices remained largely steady on 27 January, inching down slightly by INR 200/t ($2/t) in comparison to the assessment on 19 January. Due to the month-end, trades were limited, as most sellers were out of stock, and the market mostly operated at earlier prevailing prices.

Ferro silicon prices in India were at INR 93,600/t ($1,022/t) exw-Guwahati, as per BigMint’s assessment on 27 January.

Ferrous scrap: Imported scrap demand in India remained subdued, weighed down by rupee depreciation and sluggish finished steel sales that kept buyers cautious. Chilean HMS 80:20 was heard around $350/t CFR Mundra and $335/t CFR Chennai, while PNS indications were relatively firmer at about $370/t CFR Mundra (Ludhiana) and $345/t CFR Chennai; however, deal activity stayed thin as buyers and sellers failed to converge on workable levels. Overall sentiment remained soft, with mills favouring domestic scrap and short-term bookings, steering clear of bulk imported volumes until currency conditions stabilise and steel demand shows clearer improvement.

Outlook

Stainless steel prices are expected to remain supported in the near term on a strong dollar and firm global cues. However, sustained upside may be limited unless domestic demand improves and liquidity conditions ease.

Leave a Reply