- Slow offtake keeps trading subdued

- Weak rupee raises caution regarding imports

India’s stainless steel market remained muted this week, with soft demand and slow offtake keeping activity subdued across flats and longs segments. Prices were largely unchanged as mills maintained limited procurement while import inflows from Southeast Asia continued to pressure domestic prices.

Finished flats market quiet

India’s stainless finished steel flat market remained quiet this week, with prices unchanged even as soft demand continued and limited mill activity was observed.

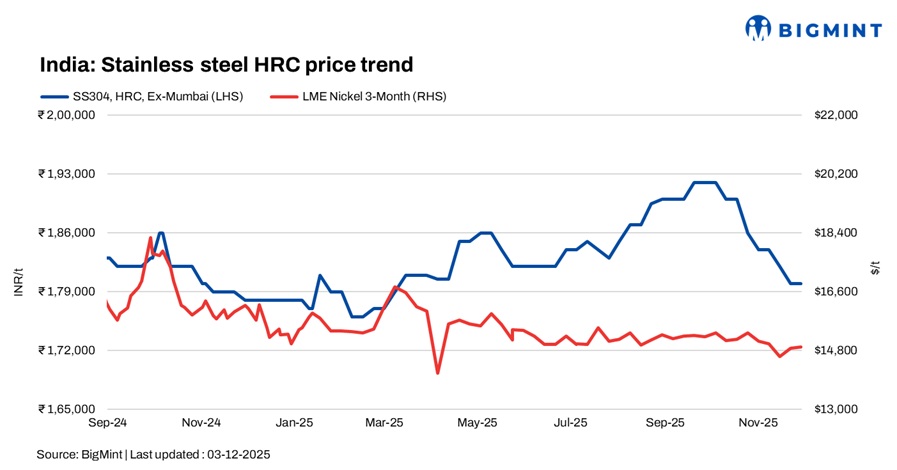

BigMint’s benchmark assessment for 304 HRC stood at INR 180,000/t ex-Mumbai, unchanged w-o-w.

Imported volumes continued to flow actively from Vietnam and Thailand adding pressure to domestic prices. Vietnam-origin 304 CRC was heard at $1,950-2,000/t, CFR India.

According to a market participant, “Some major mills have paused procurement, and further price corrections are likely expected.” Weakness in the Indian rupee has also heightened caution as costlier imports may restrict aggressive buying in the near term.

Finished longs prices soften

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars was INR 155,000/t ex-Mumbai, stable w-o-w. Meanwhile, SS 316L black round bars were at INR 274,000/t ex-Mumbai, down INR 1,000/t w-o-w.

Market participants noted that the slowdown in finished product offtake continued to weigh on sentiment. Indicative FOB prices of stainless steel longs were as follows: Indian 304 bright bars were at $2,050-2,100/t and 316 bright bars at $3,600-3,650/t, while Vietnam’s 304 bright bars were quoted at $1,880-1,950/t and 316 bright bars at $3,400-3,450/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices dropped by INR 69,000/t ($765/t) w-o-w from the previous assessment on 3 December. The decline was mainly driven by soft end-user demand and a drop in LME prices, which kept overall domestic market activity muted.

According to BigMint’s assessment on 3 December, ferro molybdenum prices in India stood at INR 2,614,000/t ($28,959/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,200/t w-o-w to INR 110,000/t ($1,212/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices fell by INR 500/t ($6/t) on 1 December as compared to the assessment on 24 November. Ferro silicon prices in India were INR 98,000/t ($1,090/t) exw-Guwahati, as per BigMint’s assessment on 1 December. In Bhutan, prices edged up by INR 700/t ($8/t) w-o-w to INR 98,500/t ($1,096/t) exw.

Ferrous scrap: India’s imported ferrous scrap market stayed selective, with ongoing cargo sales into Nhava Sheva, Mundra, and Chennai. Workable Brazil HMS was heard at $325-340/t CFR depending on loading terms, while turnings traded near $302/t CFR. Buyers maintained that HMS was not transacting at the widely quoted $330-340/t levels, with PNS workable at $340-345/t, around $10-15/t below usual ranges, reflecting cautious buying despite some firmer trade feedback. Material flows from Australia slowed due to winter yard closures, tightening supply, while rising Turkish prices reduced India’s appeal for exporters.

Outlook

The market is expected to stay cautious in the near term, with prices likely to remain range-bound on weak demand. A depreciating rupee against the US dollar may make imports costlier, limiting demand.

Leave a Reply