- Sellers maintain firm offers, anticipating pre-monsoon restocking

- Buyers show resistance on expectations of lower raw material prices

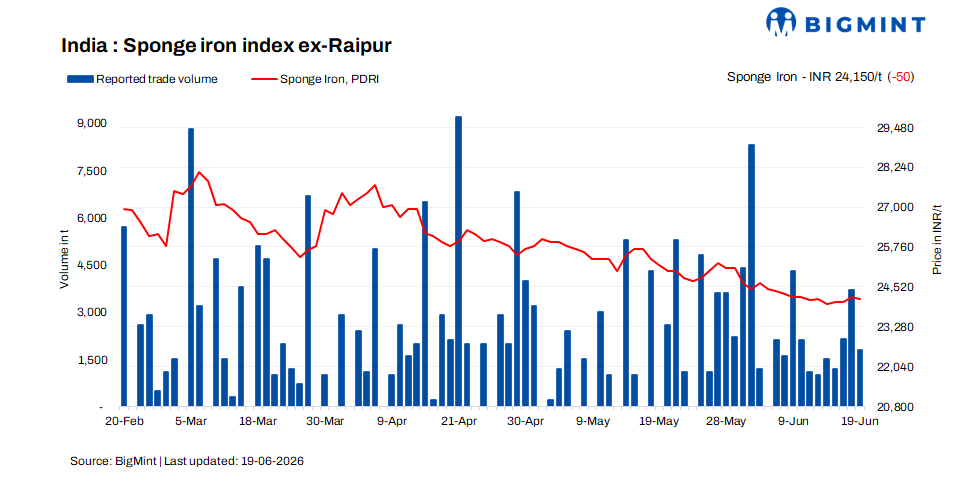

India’s sponge iron market remained under pressure during the week ended 19 June 2026, as weak downstream demand, cautious buying behaviour, and increasing regional competition continued to influence trade activity. Although benchmark pellet-based sponge iron (PDRI, FeM 79 +/-1) prices in Raipur remained unchanged w-o-w, prices edged lower by INR 50/t d-o-d to INR 24,150/t exw on 19 June 2026.

During the week, buyers largely maintained lower bids in the range of INR 24,000-24,100/t exw-Raipur, while sellers continued quoting higher offers at INR 24,300-24,500/t exw. The persistent bid-offer gap restricted fresh bookings and kept overall market sentiment subdued. Across India, sponge iron markets displayed mixed trends w-o-w, reflecting varied regional buying patterns and demand conditions.

Supply adjustments emerge as key drivers

Some major sponge iron producers in Chhattisgarh region have opted for planned maintenance shutdowns ranging between 10-15 days, reducing immediate supply pressure. At the same time, producers are increasingly shifting away from conventional offerings and focusing on product diversification to address evolving customer requirements.

Market participants reported greater availability of specialised grades, including high-phos CDRI, low-phos PDRI, mixed fines, mixed lumps, CDRI-NMDC material, CDRI-mix material, and improvement in DR-CLO grade sponge iron offers. Producers indicated that customised grade offerings are helping sustain volumes in a market characterised by weak demand and intense competition.

Weekly sentiment remains cautious

The week began on a subdued note, with weak finished steel demand and concerns surrounding the upcoming monsoon season limiting aggressive procurement. Sellers kept offers firm, anticipating pre-monsoon restocking, while buyers remained cautious amid expectations of softer raw material costs. Higher freight expenses and logistical challenges also curtailed procurement from neighbouring consumption centres, particularly Maharashtra and Punjab.

By mid-week, modest improvements in billet and finished steel demand supported slight gains in sponge iron prices. However, transaction volumes remained constrained due to the widening bid-offer disparity, prompting producers to focus on retaining market share rather than pursuing aggressive price hikes.

Regional competition intensifies

Competition among key sponge iron-producing hubs, including Raipur, Raigarh, Rourkela, and Durgapur, intensified during the week as suppliers adjusted offers to secure orders.

Market sources indicated that approximately 9,000-12,000 t of sponge iron lumps were dispatched via rake movement to the Maharashtra region from eastern India at comparatively competitive prices from nearby producing regions, reflecting the growing importance of logistics-led trade flows and regional price arbitrage.

Trade volumes were estimated at around 12,750 t on 19 June, compared with 14,050 t in the previous session, highlighting the marginal slowdown in spot market activity. Trade volumes for approximately 61,566 t were recorded this week, compared to 66,200 t last week.

Rationale

Prices have been derived based on transactions, offers, bids, and indicative price data sets. Transactions are considered as T1 and given a weightage of 50%, whereas other data sets are considered as T2 and given a weightage of the balance 50%.

Click here for detailed methodology

Share on WhatsApp

Business Account

Leave a Reply