- Port inventories in India decline w-o-w

- Sponge prices remain range-bound

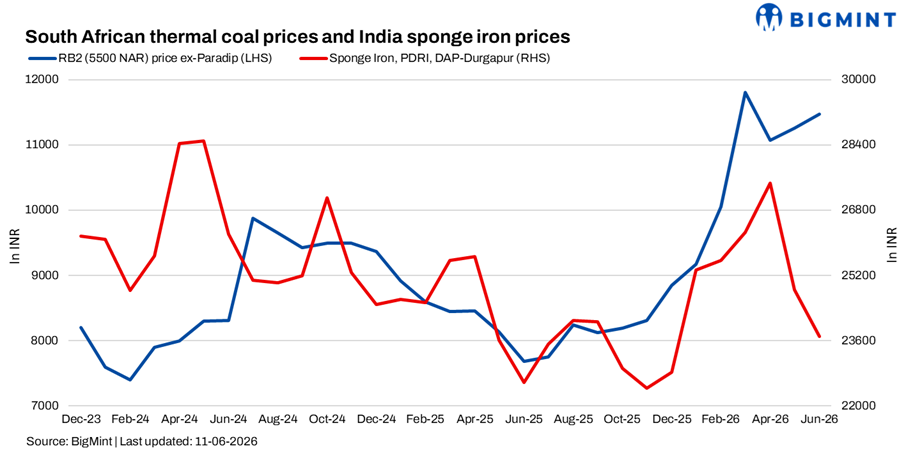

South African thermal coal sentiment remained subdued during the week ended 11 June despite firmer global cues. As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) remained stable w-o-w at INR 11,500/t, while RB3 (4,800 NAR) was unchanged at INR 9,900/t. At Vizag, RB2 declined by INR 100/t to INR 11,000/t, while RB3 increased by INR 50/t to INR 9,850/t.

India’s thermal coal inventories at major ports declined by 1.9% w-o-w to 15.31 mnt in Week 23 from 15.61 mnt in Week 22, indicating a slight drawdown despite mixed movement across ports.

Spot trades emerge selectively

Although overall trade activity remained weak, a few transactions were reported during the week. A buyer booked around 2,000 t of premium-quality RB3 (around 50 FC) at INR 9,700/t ex-Mangalore. Another trader sold approximately 10,000 t of RB3 at INR 9,700/t ex-Dhamra, while a buyer procured 5,000 t of RB3 at INR 9,900/t from Krishnapatnam, citing unaffordable RB2 prices.

At Vizag, a trader reportedly sold around 5,000 t of 5,500 NAR coal at INR 10,900/t. Meanwhile, Paradip RB2 offers were heard near INR 11,200/t, although participants stated that enquiries remained almost absent.

Firm offers struggle to attract buyers

Market participants reported that vessel offers remained firm despite poor buying interest. An unconfirmed deal for 75,000 t of South African 5,500 NAR coal was heard at around $115-116/t CFR east coast India, while fresh offers remained higher at $118-120/t CFR. Offers for 4,800 NAR coal were heard near $100/t CFR.

One trader noted that stock-and-sale material was available around $109/t, making vessel purchases unattractive. “Why would end-users buy vessels when traders are already selling at losses?” the participant said.

At Dhamra, RB2 offers were heard near INR 12,000/t. Buyers also indicated offers around INR 12,400/t at Krishnapatnam, INR 12,200/t at New Mangalore, and INR 12,000/t at Ennore, but demand remained extremely weak.

Global support fails to lift sentiment

International fundamentals continued supporting seller confidence. API4 prices reportedly increased by $3-4/t to around $124-125/t, while freight remained elevated at $21-22/t amid geopolitical concerns. Market participants also pointed to the upcoming seven-day RBCT maintenance shutdown as a supportive factor.

FOB RBCT indications were heard at $96-97/t for 5,500 NAR and $76-78/t for 4,800 NAR, while RB1 6,000 NAR continued trading at around index minus $4-5/t.

Despite these supportive factors, traders stated that weak Indian demand continued outweighing supply-side concerns.

Domestic coal keeps pressure on imports

Domestic coal remained the preferred choice for industrial consumers due to better economics and adequate availability. BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t w-o-w.

Participants noted that regular auctions and comfortable supplies continued limiting interest in imported cargoes, with procurement largely restricted to immediate requirements.

Sponge iron prices remain range-bound

Weak downstream steel demand continued weighing on coal consumption. PDRI DAP-Durgapur prices declined by INR 50/t w-o-w to INR 23,600/t. Finished and semi-finished steel segments also witnessed subdued participation, with buyers staying away from fresh bookings.

Several sponge iron producers reported severe margin pressure due to elevated pellet and raw material costs alongside weak TMT demand. According to market participants, many plants were currently incurring losses of around INR 2,000-2,500/t, with some units already operating at reduced capacities. Participants warned that additional shutdowns could occur by July if market conditions fail to improve.

Outlook

South African coal sentiment is expected to remain weak in the near term despite firm international prices and freight support. Domestic coal availability, poor sponge iron economics and limited steel demand are likely to keep procurement need-based. While lower inventories and upcoming RBCT maintenance may support offers, meaningful buying interest may remain elusive unless downstream industrial demand improves.

Leave a Reply