- Sponge iron prices rise INR 1,200/t in eastern India

- South Africa continues to face supply disruptions

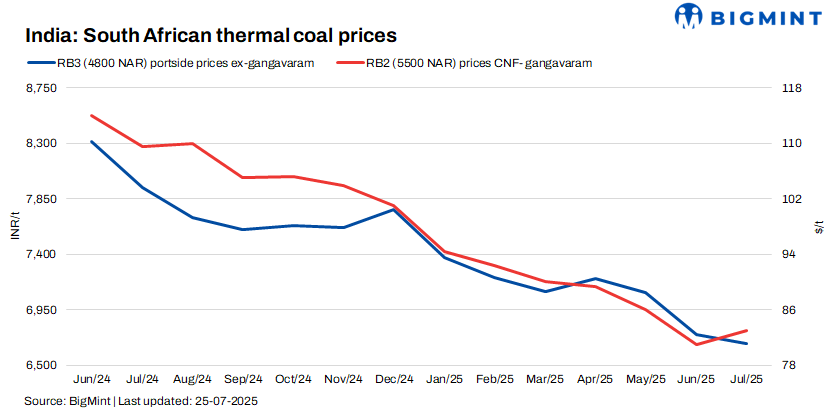

India’s portside prices of South African thermal coal continued to rise this week, driven by persistent supply disruptions in South Africa. Two key rail links to Richards Bay Coal Terminal (RBCT) remained offline, while maintenance at the port was ongoing and expected to extend up to 25 days. The constrained outbound flow pushed global index offers higher, which is now reflecting in Indian portside prices.

BigMint assessed RB2 (5500 NAR) at INR 7,800/tonne (t) and RB3 (4800 NAR) at INR 6,800/t exw-Gangavaram – both up by INR 150/t w-o-w. However, actual market activity remained sluggish as demand stayed weak despite firm offers.

Thermal coal inventories at Indian ports rose slightly to 16.13 mnt in Week 29, from 15.84 mnt last week.

Deal trends across ports

Only limited buying was seen. At Paradip, a deal for RB2 was heard at INR 7,800/t, while Mangalore saw a trade closed at INR 7,850/t.

Domestic coal prices mixed; 5000 GCV gains on sponge iron demand

Domestic coal prices saw a mixed trend. BigMint assessed 5000 GCV at INR 4,850/t, up INR 150/t w-o-w, while 4500 GCV remained unchanged at INR 4,250/t exw-Bilaspur. Prices edged up for higher grades amid increased spot inquiries from sponge iron players, as C-DRI prices surged INR 1,200/t w-o-w to INR 26,000/t exw-Rourkela. However, overall buying sentiment was weak, as SECL’s direct-to-end-user sales cut out intermediaries.

Sponge iron market active as buyers restock

The sponge iron market witnessed stronger activity. Rising steel prices and expectations of further hikes prompted buyers to restock. This helped lift demand for high-GCV coal temporarily, though long-term sentiments remain cautious amid monsoon disruptions. BigMint’s assessment for C-DRI ex-Rourkela rose by INR 1,200/t w-o-w to INR 26,000/t as on 25 July.

Outlook

South African portside offers may stay elevated in the near term amid continued export bottlenecks. However, Indian buying is less likely to improve significantly unless steel market sentiment turns more positive or inventory levels drop sharply. Most traders remain on the sidelines, watching for clearer demand cues.

Leave a Reply