- NE Asian demand, tight supply keep FOB prices elevated

- Cost advantage over scrap sustains demand for SA coal

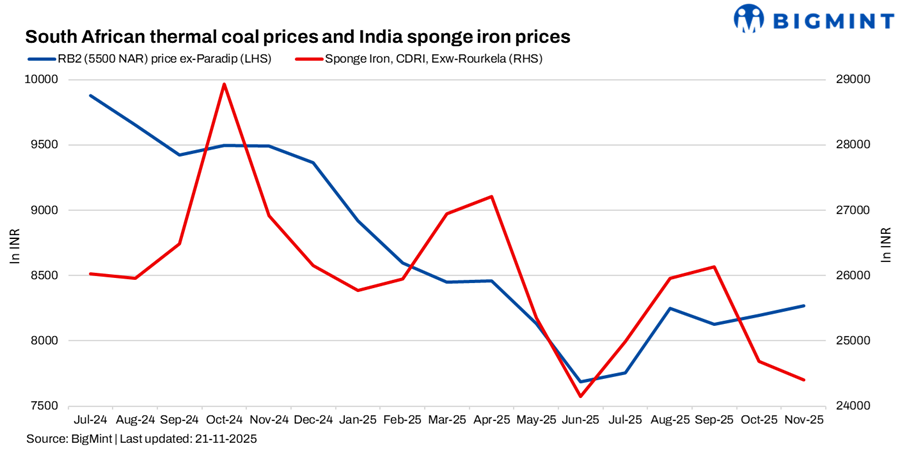

South African thermal coal prices at Indian ports remained firm w-o-w on 19 November amid tight supply. RB2 rose by INR 100/tonne (t) w-o-w to INR 8,400/t ex-Paradip, while prices in Vizag remained steady at INR 8,350/t and Gangavaram remained unchanged at INR 8,400/t. RB3 prices were flat across major east coast ports.

Offers remained at elevated levels as 5500 NAR cargoes hovered at $76-77/t FOB, supported by firmer forward markets and recent bulk buying from northeast Asia. South Korea purchased nearly 2 million tonnes (mnt) last week, while Japan floated tenders for 8-10 mnt, tightening vessel and cargo availability and pushing offers higher. Freights on the South Africa-India route also inched up w-o-w to $15.5-16/t, adding to landed costs.

Defying the broader weakness in Indian thermal coal demand, sponge iron prices recently gained momentum, resulting in improved buying inquiries for specific South African coal grades. BigMint’s C-DRI index (ex-Rourkela) stood at INR 24,200/t.

Market momentum remained constructive, with higher inquiries and active participation from traders and mills. Renewed confidence from stronger steel prices encouraged producers to raise offers, supported by steady procurement interest from integrated and secondary manufacturers.

Market data indicates that South African coal, particularly the 4800 and 5500 NAR grades, is effectively sold out for December loading. This demand is so firm that even bids in the range of $60-61/t FOB Richards Bay for 4800 NAR material are failing to secure spot tonnage. This is occurring despite weak local sponge iron prices, which typically would discourage production.

The resilience is attributed to a cost advantage over the primary alternative, scrap. The consistent demand from this sector is providing a crucial floor for South African exporters, especially as European demand for high-calorific value coal has dwindled.

Outlook

South African offers are expected to remain elevated in the near term owing to tight cargo availability, strong northeast Asian demand, and firm freight. Indian buying may stay muted unless the bid-offer gap narrows or vessel supply improves.

Looking forward, market participants anticipate further price appreciation for South African coal. The combination of strong Asian demand, a changing of ownership at several mines potentially leading to more dynamic marketing, and limited competition from other origins has led to forecasts of a 7-10% price increase for South African coal between now and March 2026.

This trend highlights how niche industrial demand can create a bullish micro-climate within an otherwise bearish or stagnant broader market.

Leave a Reply