- Sponge prices drop by up to INR 1,000/t w-o-w

- Coal portside inventories in India up 4% w-o-w

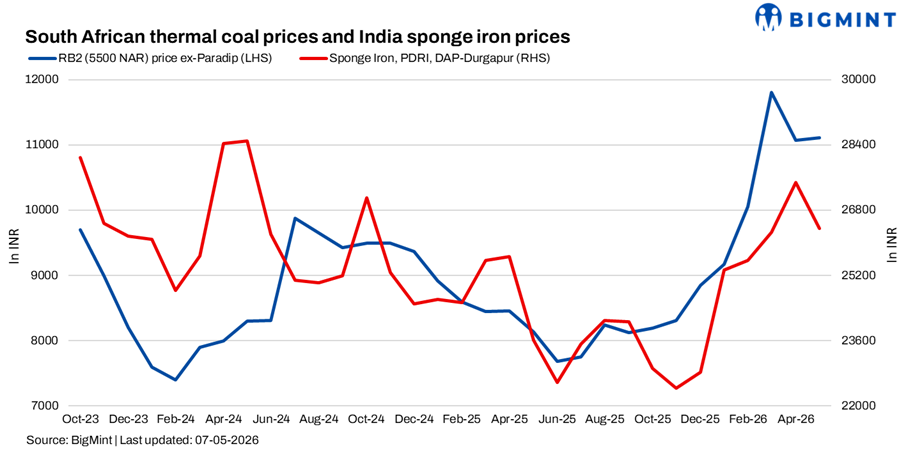

South African thermal coal prices at Indian ports showed mixed trends w-o-w as on 7 May 2026, even as international offers moved higher amid rising freight and energy costs.

As per BigMint’s assessment, ex-Paradip and ex-Vizag RB2 5,500 NAR prices increased marginally by INR 50/t w-o-w to around INR 11,050/t, while RB3 4,800 NAR prices declined by INR 50-100/t to INR 9,650-9,700/t. However, despite the increase in offers, market activity remained extremely limited with buyers showing little interest at elevated levels.

Additionally, India’s imports of South African non-coking coal declined sharply to 1.97 mnt in April from 3.48 mnt in March, reflecting a steep 43.4% m-o-m drop amid weak industrial demand and increasing preference for domestic coal.

Higher freight and global cues lift offers

Market participants highlighted that international coal prices strengthened following the recent rise in gas and crude oil prices, creating upward pressure from both Indonesian HBA benchmarks and freight markets. Freight costs remained firm, further increasing landed costs for imported cargoes.

Traders noted that offers for RB2 were initially heard around INR 11,300/t before easing to around INR 11,000/t within a day due to lack of buyer acceptance. Some upcoming vessel cargoes were also offered at higher levels, though enquiries remained negligible. Participants stated that buyers were unable to absorb higher prices amid weak downstream demand and availability of cheaper domestic alternatives.

At Mangalore, a buyer purchased around 2,000 t of premium RB3 cargo with 50% fixed carbon this week at around INR 9,500/t exw, compared with nearly INR 10,000/t for the same grade purchased a few weeks earlier and RB2 availability remained limited.

Weak sponge iron market weighs on sentiment

Demand conditions remained weak across the sponge iron and steel sectors, continuing to pressure imported coal. PDRI DAP-Durgapur prices declined sharply by INR 900/t w-o-w to INR 25,750/t on subdued enquiries and limited transactions.

Market participants noted that procurement remained strictly need-based, with buyers adopting a wait-and-watch approach amid falling steel prices and weak finished steel demand. Buying activity in both semi-finished and finished steel markets stayed muted, restricting raw material consumption.

Traders reported that despite sellers lowering offers to stimulate enquiries, overall participation remained poor. Bid-offer gaps widened further as buyers resisted elevated imported coal prices.

Domestic coal and high inventories pressure imports

Domestic coal continued to remain significantly cheaper and more attractive for consumers. The availability of lower-priced domestic material kept pressure on imported coal demand, particularly for sponge iron manufacturers facing compressed margins.

India’s non-coking coal inventories at major ports increased by 3.7% w-o-w in week 18, rising to 15.14 mnt from 14.60 mnt in week 17, indicating continued cargo inflows despite slow evacuation. Elevated inventories across ports further reduced urgency for fresh imports.

Outlook

South African coal offers may continue to remain firm in the near term due to higher freight rates, stronger international cues, and rising energy prices. However, weak sponge iron demand, elevated port inventories, and availability of cheaper domestic coal are likely to restrict buying interest.

Leave a Reply