- BALCO remained the largest bidder, followed by Vedanta, Sarda

- High competition for G11 and mid-CV grades

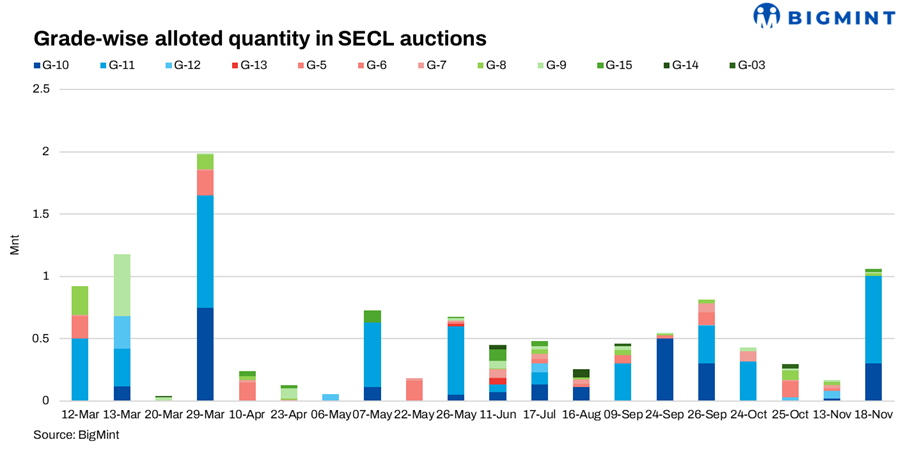

South Eastern Coalfields Ltd (SECL) sold 1.06 million tonnes (mnt) of non-coking coal in a spot auction held on 18 November, 2025, achieving one of its highest allocation ratios in recent weeks, with 98% of the 1.078 mnt on offer quantity getting booked. The auction saw broad-based participation from primary industrial buyers, especially power, aluminium and sponge iron units, reflecting renewed procurement interest after weeks of tight arrivals and rising spot demand.

Grade-wise performance: G11 dominates; strong premiums for mid-CV grades

G11 emerged as the most traded grade, contributing 700,000 t at INR 2,114/t, significantly above its floor price of INR 1,418/t.

This grade, with a calorific value (CV) range of 4000-4300 kcal/kg, continues to attract robust demand from captive power and aluminium refineries.

G10 was the second-largest category with 304,000 t, clearing at INR 1,908/t, around 17% above the floor level. Consistent premiums indicate steady blending demand and improved buying confidence among industrial users.

Higher-grade materials also saw strong interest:

- G8 (4900-5200 kcal/kg): 19,000 t at INR 2,877/t

- G9 (4600-4900 kcal/kg): 13,000 t at INR 2,771/t

Both grades commanded sizeable premiums as sponge iron and small industrial units sought better CV coal amid tightening regional availability.

Lower-CV G15 (2800-3100 kcal/kg) saw 24,000 t booked at INR 1,269/t, indicating moderate demand but meaningful participation due to competitive pricing.

Across grades, the average auction premium reached INR 2,201/t, signalling firm market sentiment and improving restocking activity.

Mine-wise allocations: Gevra and RLS Laxman drive majority of supply

SECL drew material from large open-cast and select underground mines, with notable price variations reflecting quality and demand intensity.

Gevra OC: Supplied 500,000 t of G11, cleared at INR 2,102/t, indicating strong but price-disciplined buying

RLS Laxman: Supplied 200,000 t of high-demand G11, recorded a much higher clearing price of INR 2,284/t, reflecting superior grade consistency and competitive bidding

Chhal OC: Offered 320,000 t (G10 & G15), cleared at INR 1,871/t on average, showing steady interest for mid-CV grades

Premiums were notably higher at:

- Damini UG (G8): INR 3,455/t

- Bhatgaon UG (G9): INR 2,790/t

These higher UG prices highlight increasing competition for higher-CV materials with better combustion efficiency.

Buyer-wise allocations: BALCO, Vedanta and SMAL among top procurers

BALCO (Bharat Aluminium Co. Ltd.) emerged as the largest buyer, securing 120,300 t at INR 1,998/t, mainly in G11-G10 grades to support captive power consumption.

Vedanta Ltd procured 80,000 t at INR 2,003/t, while Sarda Metals & Alloys Ltd purchased 50,000 t at INR 2,188/t, reflecting aggressive competition for mid-CV grades used in metallurgical operations.

The diversity in buyer categories – aluminium, sponge iron, traders and beneficiation units – indicates broad-based procurement across industrial segments.

Market insight: stronger premiums signal revival in demand

The auction reflected a clear improvement in buying sentiment compared with early November:

- High competition for G11 suggests tightening supply and rising captive consumption needs.

- Strong premiums for G8-G9 point to firmer sponge iron sentiment and blending demand.

- High UG prices reflect preference for consistent-quality coal amid volatile imported coal markets.

- Near-complete sell-through (98%) indicates active restocking after several weeks of subdued procurement.

Overall, the auction dynamics suggest buyers are positioning ahead of December demand, with expectations of limited spot availability and potential firmness in coal consumption from key industrial sectors.

Outlook

SECL auctions are likely to maintain firm premiums through late November due to tight supply of high-CV and underground grades, rising demand from sponge iron and aluminium sectors, and falling reliance on imported coal of mid-CV grades due to higher landing costs.

While bulk buyers such as BALCO and Vedanta may remain consistent participants, competition from small traders may rise if domestic portside prices increase further. Overall, auction sentiment is expected to stay firm in the near term.

Leave a Reply