- Sales volumes rise by 5% in FY’25

- Capex drive to achieve 35 mnt/year target by 2030

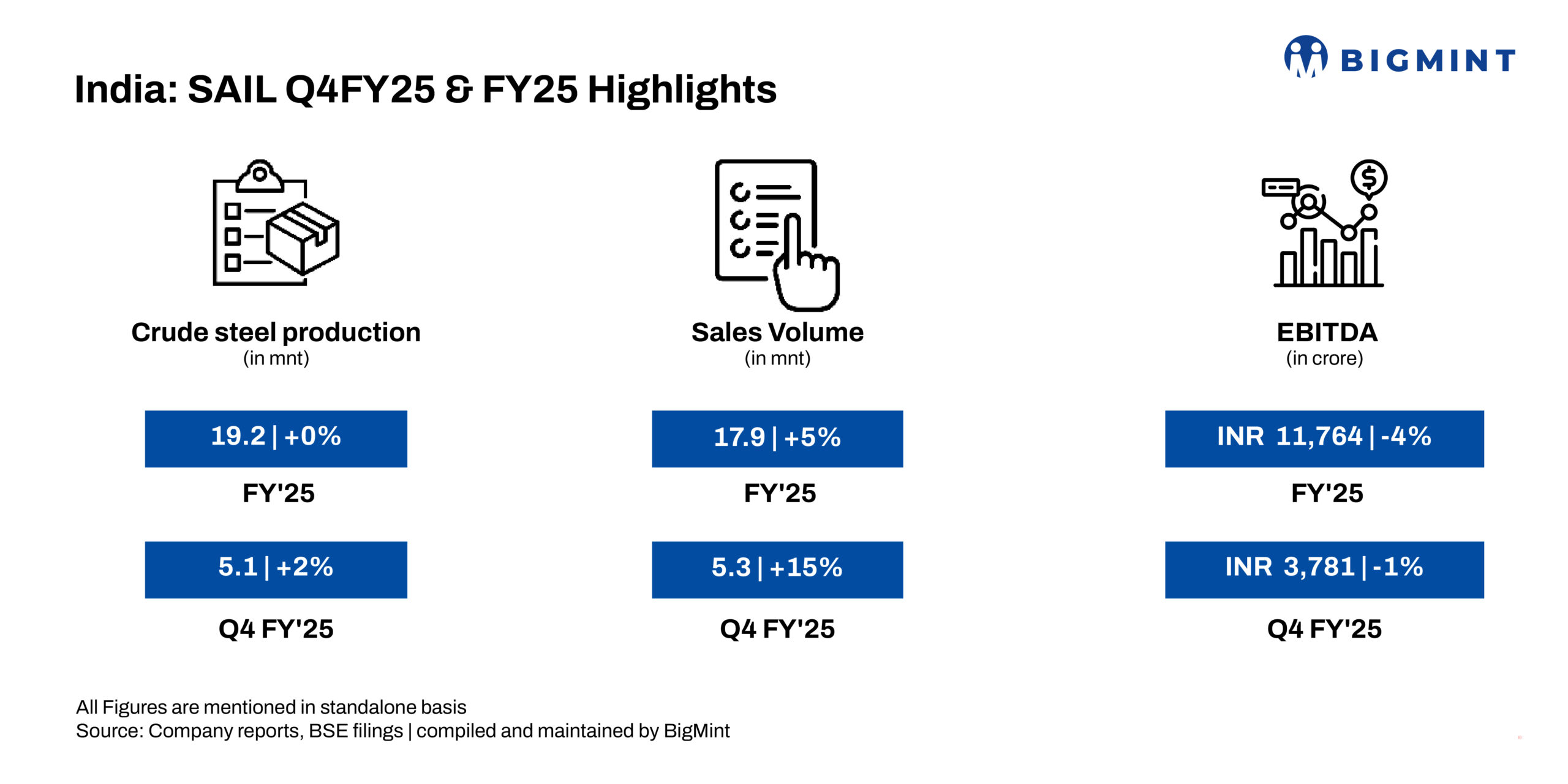

PSU Steelmaker, Steel Authority of India Limited (SAIL), has reported flat production y-o-y, while sales volumes increased 5% to 17.9 mnt in FY’25. With a capex of INR 7,500 crore planned for FY’26, the company aims to boost capacity and sustain long-term growth.

Highlights

Crude steel production stable y-o-y: SAIL’s crude steel production remained stable y-o-y at 19.2 mnt in FY’25. Meanwhile, the same edged higher by 2% y-o-y to 5.1 mnt in Q4FY’25 from 5 mnt in the same period last year.

Sales rise 5% in FY’25: The company’s sales volumes rose 5% on the year to 17.9 mnt in FY’25 from 17 mnt in FY’24. Similarly, sales increased 15% y-o-y to 5.3 mnt in Q4FY’25 as compared with 4.6 mnt in Q4FY’24.

EBITDA drops y-o-y: The company’s EBITDA witnessed a drop of 4% y-o-y to INR 11,764 crore in FY’25 from INR 12,280 crore in FY’24. Likewise, EBITDA edged down 1% on the year to INR 3,781 crore in Q4FY’25 as against INR 3,829 crore in Q4FY’24.

Revenue from operations down 3% y-o-y: Revenue from operations fell by 3% on the year to INR 1,02,478 crore in FY’25 from INR 1,05,375 crore in FY’24. In Q4, the same increased y-o-y by 5% to INR 29,316 crore as against INR 27,958 crore in Q4 of the previous year.

Capex for FY’26: The company has set a capital expenditure (capex) target of INR 7,500 crore for FY’26, marking the start of its phased expansion to raise crude steel capacity from 20 to 35 mnt by 2030. Initial spending has begun, with major disbursements expected to ramp up from FY’27 onwards.

Coking coal cost: Coking coal costs eased in Q4FY’25, with average imported coal prices falling from INR 20,000/t in Q3FY’25 to INR 18,500/t in Q4FY’25. Prices are currently stable at INR 17,000-17,500/t, offering cost relief to steel producers. Minor fluctuations are expected in the near term.

Net sales realisations (NSR): In Q4FY’25, flat product NSR improved from INR 46,800-47,300/t. Long product NSR remained stable at around INR 53,500/t. For April–May FY’26, NSRs rose to INR 50,500-50,700/t for flats and INR 55,000 for longs, supported by safeguard duties and improved demand.

Outlook

The company anticipates steady demand, improved realisations, and stable input costs to support margins in Q1FY’26, with infrastructure growth and safeguard duties boosting domestic steel consumption despite seasonal monsoon challenges.

Leave a Reply