- Baltic recovery and higher bunkers support coal freight rates

- Few fixtures reported as high tonnage keeps owners cautious

A recovery in the Baltic Index for Panamax and Supramax vessels throughout the week, together with higher bunker prices and firmer crude oil futures, supported dry bulk coal freight rates in the week under review. However, fixing activity stayed muted as a wide bid-offer gap between shipowners and charterers kept most market participants on the sidelines. Fixtures were largely by SAIL, with only one Australia-India coal shipment reported during the period.

“Asia-Pacific Supramax freight rates were largely flat to softer. In the Indian Ocean, ample tonnage continued to cap rates, particularly along India’s East Coast. Bunker prices, meanwhile, edged slightly higher during the day,” a person with knowledge of the matter told BigMint.

Another ship-operator noted, “Asia-Pacific Panamax freight rates moved higher, supported by a steady market outlook in the Pacific basin. Freight derivative rates firmed during Asian trading hours, while bunker prices rose d-o-d.”

Highlighting the limited number of fixtures concluded at higher levels, a charterer noted, “Market conditions remain slow and challenging, with sentiment weighed down by ongoing geopolitical uncertainties, though cautious optimism for improvement persists.”

Meanwhile, The Baltic Dry Index (BDI) surged sharply by 229 points (15%) w-o-w to 1,761 on 22 January 2026, driven by stronger cargo demand and tighter vessel availability. Panamax rates climbed 216 points to 1,614, while Supramax gained 56 points to 1,019, reflecting firming activity across key routes and improved sentiment in the dry bulk market.

Crude-led bunker gains tighten freight margins

Bunker prices rose this week in tandem with firmer crude oil futures, driven by tightening supply conditions and steady demand across key energy markets. Expectations of constrained oil output, coupled with geopolitical risks and improving refinery margins, supported crude prices, which in turn lifted marine fuel costs. The increase in bunker prices added upward pressure on vessel operating expenses, prompting shipowners to resist lower freight levels and seek rate adjustments, particularly in segments where tonnage supply is tightening. However, weak cargo demand in some regions limited the extent to which higher fuel costs could be passed through to freight rates.

Route-wise updates

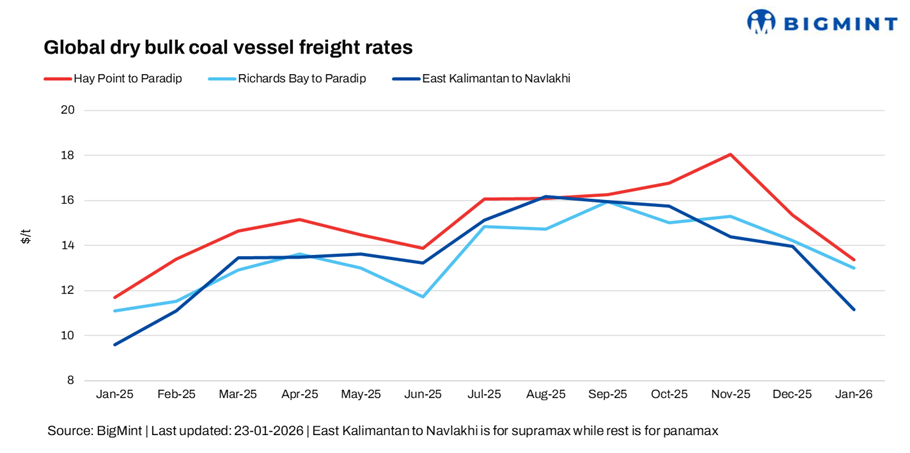

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up by around 1.2/dry metric tonne (dmt) w-o-w to $14.1/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route increased by $1.5/dmt w-o-w to $13.9/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood stable w-o-w at $10.8/dmt.

Outlook

Near-term dry bulk coal freight rates to India are expected to remain soft to range-bound. Ample vessel availability across the Pacific and Indian Ocean continues to cap rates, while subdued cargo inquiries from Indian importers are limiting upward momentum. Fixing activity remains thin, and high prompt tonnage keeps owners cautious. Some support could emerge if seasonal buying picks up or vessel lists tighten, but without a clear surge in coal demand, any recovery is likely to be gradual rather than sharp.

Leave a Reply