- Africa-led demand continues to support freight rates

- Elevated domestic prices limit export volumes

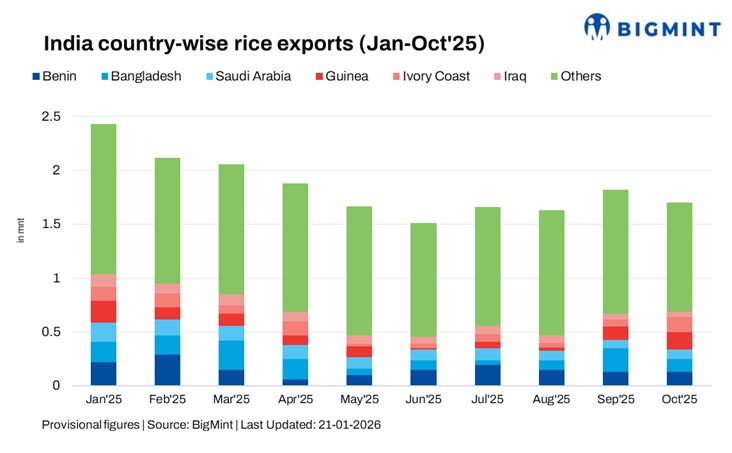

India’s rice export freight sentiment remained mixed this week, with bulk freight easing on Africa-bound routes and container freights showing positive trends across the Middle Eastern and East African routes, except JNPT, India to Tamatave, Madagascar. While Africa continued to anchor India’s rice exports, high domestic rice prices, weak fresh enquiries, and destination-side risks limited any upside in freight rates.

Bulk shipments from India’s east coast, especially Kakinada, remained active for African destinations, but spot sentiment weakened due to limited fresh cargoes, subdued demand and ample Supramax availability. This capped any near-term recovery in bulk freights. On the container side, shipments from Mundra and JNPT to the Middle East and East Africa stayed largely rangebound, with selective firmness on Gulf routes as liner operators maintained disciplined pricing through space management and blank sailings.

“Sentiment remained weak due to high domestic prices and soft global demand”, a source informed BigMint,

Another source noted, “Stronger basmati prices have supported domestic demand but hurt exports, while non-basmati remains slightly positive with limited impact.”

“The market remains weak with limited cargo availability. Shipments are expected to stay at current levels until mid-February, after which a mild correction is possible,” a source said.

Market participants also pointed to rising global competition for rice exports, with a trader adding, “Buyers are benchmarking Indian prices against alternative origins such as Vietnam, Pakistan, and Thailand, with some shifting to lower-cost options. Meanwhile, domestic supply requirements on millers are constraining exportable surplus and tightening cargo availability.”

Meanwhile, India’s rice exports have remained supported structurally following the easing of earlier export restrictions. However, near-term shipment momentum has slowed as high prices, policy costs and weak global demand have made Indian rice less competitive versus other origins. Exporters are therefore adopting a more cautious approach, focusing on regular buyers and smaller parcels rather than aggressive forward sales.

Payment risk and currency considerations also continued to influence trade sentiment. Exports to destinations such as Iraq and parts of Africa remained selective due to LC confirmation timelines and counterparty risk. Uncertainty around Iran-bound trade, amid geopolitical tensions and payment-related challenges, has further added caution to Middle East-facing shipments, prompting exporters to prioritise established buyers.

However, some market participants reported higher freight levels, particularly on the Mundra-Umm Qasr and Mundra-Jebel Ali routes at around $31/t and $15.5/t, respectively, as sources claimed that certain buyers were ready to pay premium for faster deliveries despite overall weak demand.

Market highlights:

- Africa-led demand supports rice freights: Steady buying interest from West Africa continues to support India’s rice export flows, helping prevent a sharper fall in both bulk and container freights despite weak global demand.

- Weak cargo availability caps freight upside: Limited fresh cargoes, high domestic prices and cautious buying have reduced shipment urgency, keeping freight rates under pressure as buyers delay purchases and resist higher offers.

- Capacity discipline and vessel supply cap rates: Liner operators are managing container capacity through space control and blank sailings, while ample Supramax availability, reflected in a soft Baltic market, has limited owners’ pricing power on bulk routes.

- Stable bunkers and Red Sea uncertainty: Stable bunker prices have reduced cost-push pressure on freights, while ongoing Red Sea uncertainty and cautious routing decisions continue to influence global vessel availability and freight sentiment.

Outlook

Looking ahead, India’s rice export freight rates are expected to remain largely stable in the near term. While steady demand from Africa is expected to provide a base level of support, upside potential is likely to remain capped by high domestic rice prices, weak global demand, limited fresh cargo availability and ample vessel supply.

Market participants expect shipment activity to stay subdued until mid-February, with only a mild improvement possible thereafter if prices soften and buying interest returns. Ongoing competition from other origins, destination-side payment risks and uncertainty around Iran-bound trade are likely to keep overall freight sentiment cautious.

Leave a Reply