- Freights fall on most routes amid weak demand, ample tonnage

- India-Guinea rates inch up on steady cargo flow, stronger enquiries

India’s rice export freight market remained under pressure in the week ended 27 May 2026, with bulk freight sentiment staying subdued amid limited cargo activity, port congestion, and ample vessel availability. Weak enquiry levels and cautious chartering kept rates under strain, reflecting an overall sluggish market tone.

A shipbroker told BigMint, “Market sentiment appears to be softening amid expectations of lower fuel prices, driven by ongoing US-Iran peace talks and easing concerns over potential supply disruptions in the energy market.”

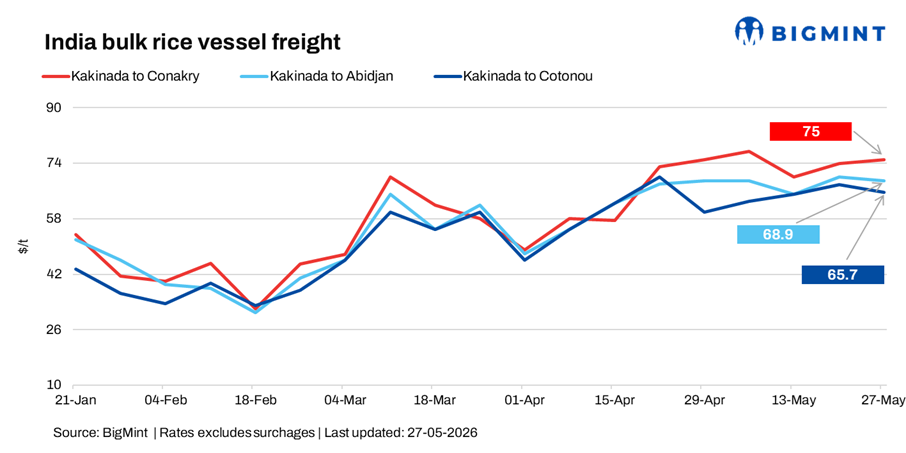

West African bulk segment struggles amid sluggish trade activity

Bulk freight sentiment on the Kakinada-West Africa route trended downward across most key corridors this week, weighed by weak cargo demand and sufficient vessel availability. However, the India-Guinea route remained relatively firm, supported by steady cargo flow and comparatively better enquiry levels.

“Demand from African markets continues to hold, but overall purchasing momentum remains weak. Despite limited activity, freights have edged higher on the Guinea route, supported by a tighter vessel supply and ongoing market uncertainty,” another shipbroker stated.

East Africa container rates mixed; India-Kenya rates surge

Container freight rates to East Africa showed a mixed trend during the week, with most routes witnessing limited momentum amid balanced demand-supply dynamics. However, the India-Kenya corridor stood out as the only positive performer, supported by relatively stronger cargo movement and firmer booking activity compared to other regional routes.

Container freight markets remained volatile amid ongoing geopolitical tensions, with uncertainty around trade flows and fuel outlook continuing to influence rate movements.

Route-wise update

Export market sentiment remains cautious

India’s rice shipments fell due to port congestion and delayed vessel clearances, with Kakinada handling most volumes. Weak African demand and higher freight costs further slowed export activity. However, a large cargo pipeline remains, with significant volumes at anchorage and berth, mainly at Kakinada, indicating potential recovery once clearances improve and demand picks up.

Outlook

Rice freight rates are expected to remain under mild pressure in the near term due to sluggish export demand and ongoing port congestion. However, elevated cargo at anchorage and a steady vessel pipeline may lend intermittent support, with any recovery likely contingent on improved buyer activity and faster vessel clearances.

Leave a Reply