- Mid-CV coal grades in demand

- Broader supply base normalizes price discovery

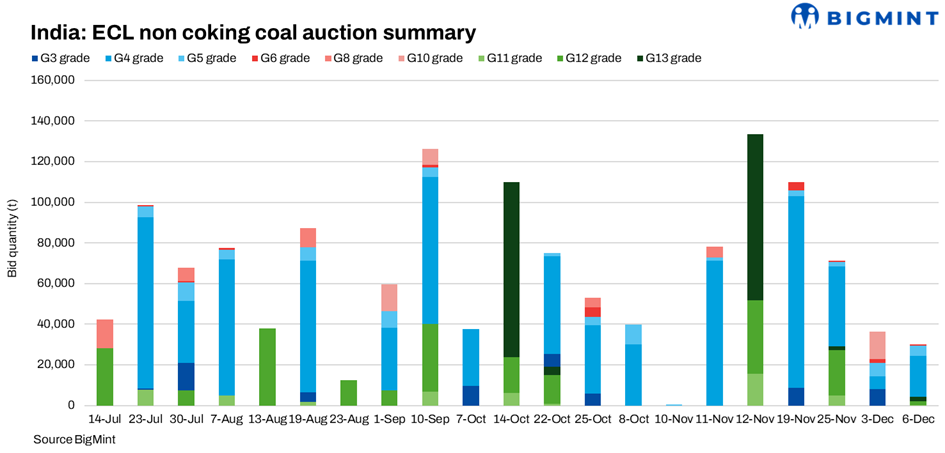

Eastern Coalfields Ltd (ECL) sold 34,250 t of non-coking coal in its auction held on 6 December 2025, marginally lower than 36,300 t offered on 3 December. Unlike the previous round, which was marked by extreme underground-origin premium distortion, the latest auction showed a more balanced price structure, with G4 grade coal premiums normalising as supply diversified across opencast (OC) and underground (UG) mines.

G4 anchors volumes

G4 (6,100-6,400 GCV) dominated the auction with 24,300 t sold at an average of INR 4,570/t, sharply lower than the INR 6,794/t average on 3 December. The correction reflected the absence of ultra-high-priced underground outliers such as Nimcha UG seen earlier.

G5 grade (5,800-6,100 GCV) of around 5,100 t was sold at INR 4,090/t, stable compared with INR 4,087/t on 3 December, indicating steady mid-CV demand.

Lower grade prices remained range-bound. G12 (3,700-4,000 GCV) and G13 (3,400-3,700 GCV) were sold at INR 1,798/t and INR 1,713/t, respectively, aligning with prior auction levels. G6 (5,500-5,800 GCV) cleared 700 t at INR 3,024/t, unchanged versus earlier trends. Small parcels of W03 fetched INR 4,203/t.

Mine-wise allocations

Supply in this auction was more evenly distributed across mines. Chitra OC anchored volumes with 14,450 t at INR 4,437/t, supported by Nakrakonda OC (3,250 t) at similar levels. Bhanora OC stood out with 2,000 t at INR 5,618/t, reflecting selective premium for quality OC material.

UG mines such as Khandra UG (2,000 t at INR 5,114/t), Kalidaspur UG (1,000 t at INR 4,747/t), and Lakhimata UG (1,900 t at INR 4,085/t) attracted healthy bids but stayed well below the extreme INR 10,840/t recorded for G4 UG material on 3 December. The wider spread of UG parcels diluted scarcity-driven aggression.

Buyer-wise allocations

Gagan Ferrotech emerged as the largest buyer with 2,500 t at INR 4,437/t, followed closely by SS Enterprises with 2,450 t at INR 4,319/t. Other buyers such as Shree Bahubali Mercantile and BR Sales selectively booked higher-quality parcels, with BR Sales paying up to INR 4,844/t for limited volumes. Participation remained broad but disciplined compared with the previous auction.

Market scenario

Compared with the 3 December auction, the 6 December round marked a clear normalization phase. The removal of ultra-scarce UG-origin G4 parcels prevented artificial inflation of averages, bringing G4 premiums back in line with CV fundamentals. Mid-CV grades held steady, while lower grades continued to clear at realistic price points. Overall, the auction reflected healthier price discovery, with demand remaining firm but more rational ahead of ECL’s larger mid-December offerings.

Note: All prices mentioned above are exclusive of GST, additional statutory taxes, and freight charges.

Leave a Reply