- Landed costs of imported cotton rise by INR 6,000-7,000/t post duty

- Spot prices in several mandis still below MSP, signalling soft demand

India has reinstated the 11% import duty on raw cotton from 1 January 2026 after the expiry of the temporary duty-free import window that had been in place since August 2025. The policy shift has immediately raised landed costs of imported cotton and altered near-term price dynamics in the domestic market, particularly during the peak arrival phase of the 2025-26 season.

Price dynamics

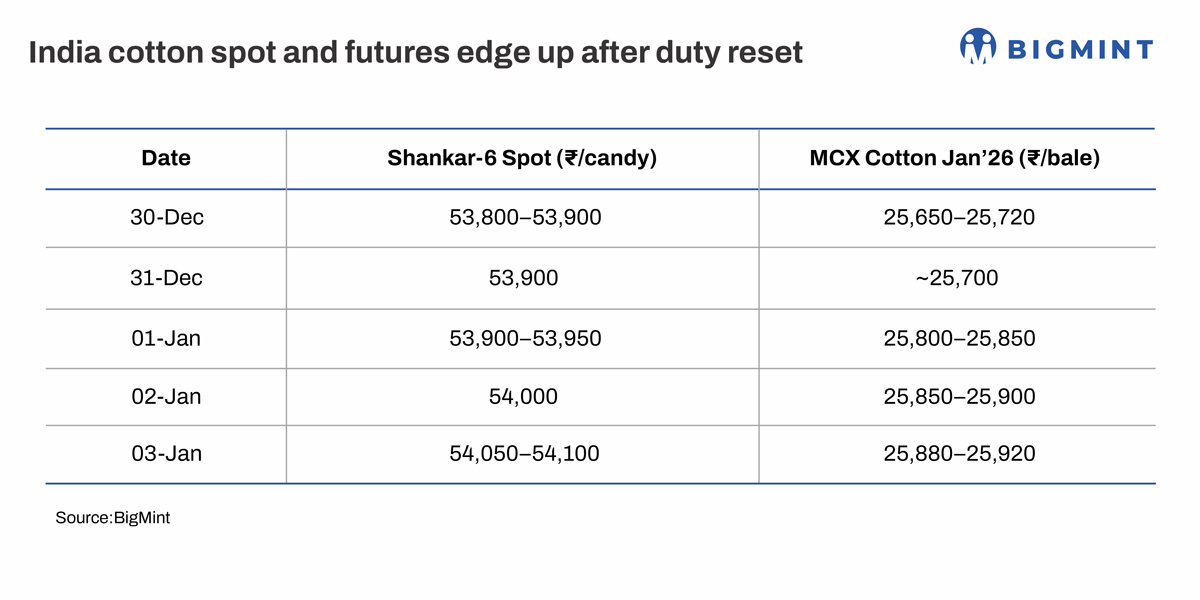

Domestic cotton prices showed early signs of stabilisation after 1 January. Gujarat benchmark Shankar-6 prices, which were trading near INR 53,800-53,900 per candy at the end of December, moved up to around INR 54,000-54,100 per candy in the first week of January. On the futures side, MCX cotton (near-month), which had slipped below INR 25,700 per bale in late December, recovered to the INR 25,850-25,900 range post-duty, indicating reduced downside pressure rather than a strong bullish shift.

The duty reinstatement follows heavy imports during the exemption period, with industry estimates placing total imports at 35-36 lakh bales, largely from Brazil, the US, and Australia. With the duty back, the landed cost of imported cotton has increased by roughly INR 6,000-7,000/tonne (t), narrowing the discount versus domestic cotton and discouraging fresh import bookings. This has helped domestic prices hold firm even as arrivals remain seasonally high.

However, weak downstream demand and heavy government intervention have prevented a sharp surge in prices. In Maharashtra’s Vidarbha region, spot prices in several mandis are still reported below the MSP of INR 8,110 per quintal, often in the INR 7,400-7,800/quintal range, reflecting limited private buying interest. To cushion farmers, CCI procurement has scaled up sharply, with cumulative buying estimated at around 65 lakh bales by early January, accounting for a significant share of arrivals. While this has strengthened the price floor, it has also reduced open-market liquidity and limited aggressive participation by traders.

Spinning millers remain cautious buyers. Yarn demand is uneven, export orders have not recovered meaningfully, and mills are struggling to pass on higher fibre costs. Although the duty reset reduces competition from imported cotton, it simultaneously raises raw material costs for mills, tightening margins further and keeping procurement strictly hand-to-mouth.

Outlook

Prices may remain at around current levels or firm up mildly. Domestic cotton prices are likely to remain supported by MSP procurement and weaker import competitiveness, but futures are expected to trade within a narrow band unless yarn demand improves materially. For ginners, higher CCI buying and reduced import pressure improve price realisation prospects. For spinning millers, sourcing will remain cautious, with a greater focus on cost control. Overall, the cotton market is expected to stay supported by policy but limited by demand, with price discovery driven more by procurement and duty structures than by consumption recovery in the near term.

Leave a Reply