- Mills hike HRC, CRC prices amid rising costs

- Supply tightens as fuel shortages, shutdowns loom

Leading Indian steelmakers have revised their list prices upward for early-April 2026, raising HRC and CRC prices by INR 1,000-3,500/t ($11-38/t). HRC list prices (2.5-8 mm, IS2062, Gr E250 Br) were placed in the range of INR 58,050-61,000/t ($625-656/t) ex-Mumbai, while CRCs (0.9 mm, IS513 CR1) were listed at INR 65,400-68,250/t ($704-734/t).

The upward revision reflects a broader strengthening observed in recent months. Trade-level HRC prices climbed by INR 2,850/t ($31/t) m-o-m to INR 56,600/t ($609/t) in March compared with INR 53,750/t ($579/t) in February. CRC prices posted an even sharper rise, surging by INR 3,500/t ($37/t) to INR 63,200/t ($680/t) from INR 59,700/t ($643/t) over the same period.

The rally is underpinned by a confluence of factors like constrained material supply, sustained raw material cost pressures and lingering geopolitical uncertainty, all of which continue to shape market dynamics heading into the new financial year.

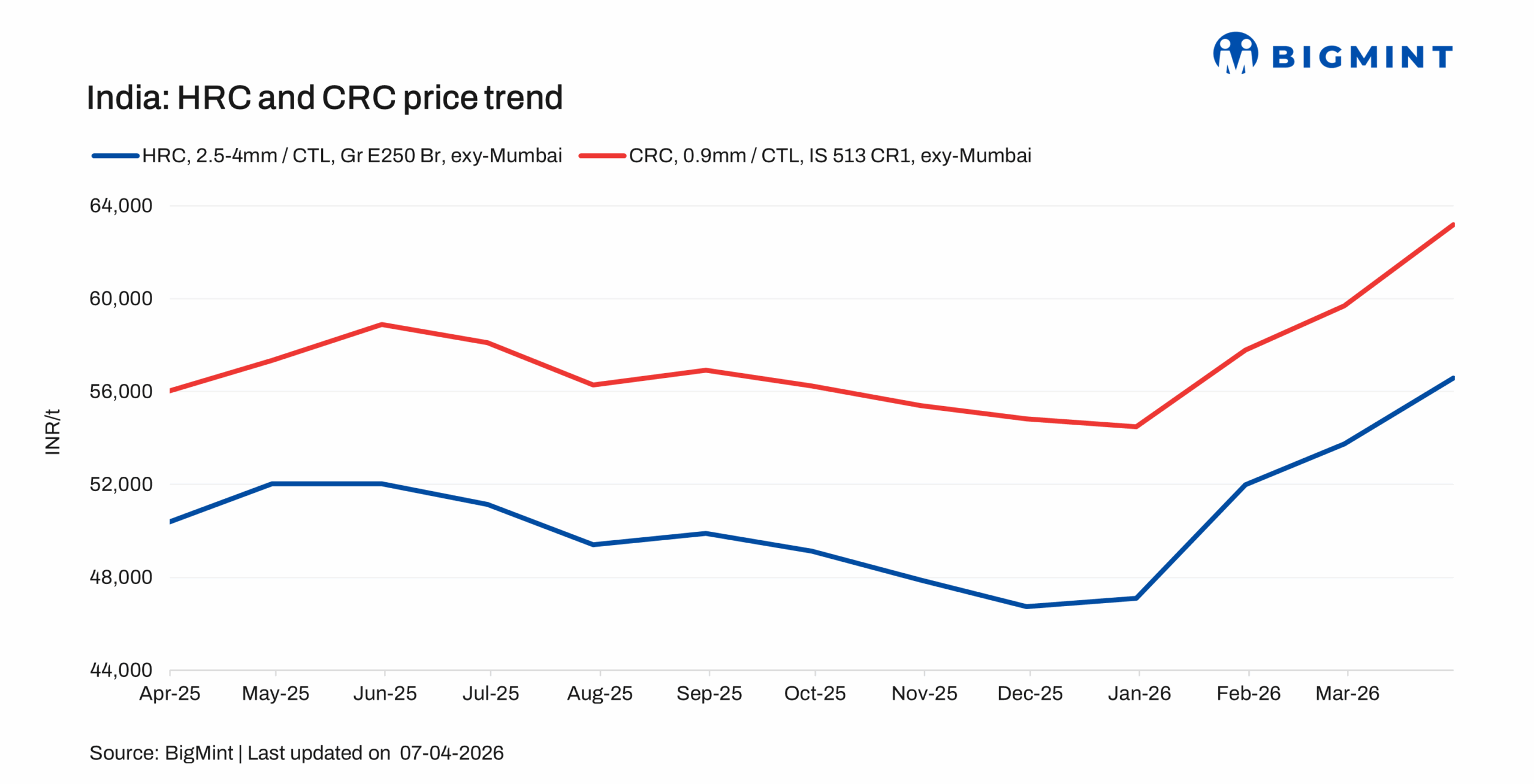

W-o-w price assessment

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices inched up by INR 400/t ($4/t) w-o-w to INR 59,900/t ($644/t) on 7 April against INR 59,500/t ($640/t) in the same period last week.

CRC (IS513, Gr O, 0.9 mm/CTL) prices stood at INR 67,500/t ($726/t) as assessed on 7 April, up by INR 500/t ($5/t) w-o-w against INR 67,000/t ($721/t) on Tuesday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Why Indian mills raised HRC and CRC prices for Apr’26?

1. Higher raw material costs squeeze margins

Domestic steelmakers are under growing pressure from rising input costs, with coking coal at the forefront. Imported coking coal prices climbed by $10/t m-o-m to $262/t in March, up from $252/t in February, adding direct pressure on production economics.

Moreover, NMDC has raised iron ore prices by INR 450-550/t ($5-6/t) for April. Market sources suggest this increase was widely anticipated, reflecting the firm recovery in semi-finished and finished steel prices seen towards the close of FY26.

2. Tight material availability adds to cost pressures

Further downstream, sentiment has turned notably tighter. Production of cold-rolled and coated steel products is constrained by limited gas and fuel availability, squeezing material supply across the value chain.

Amid these challenges, one major mill has taken a proactive step by successfully deploying syngas in its galvanizing and colour coating furnaces as a substitute for natural gas, LPG and propane. This move helped the company keep operating despite fuel disruptions, showing the industry’s ability to adapt to tough conditions.

Market update

Trade-level sentiment in the Indian market for both HRC and CRC remains bullish, buoyed by mill price hike announcements and tightening supply conditions. A market participant informed Bigmint, “Supply constraints persist across specific sizes and thicknesses, creating scarcity and limiting material availability in the spot market”.

On the demand side, however, the momentum appears measured rather than broad-based, largely driven by low inventory levels and buyers’ urgency to secure material at relatively competitive prices, rather than a strong uptick in end-use consumption.

Adding to the supply-side pressure, one of India’s steel majors is reportedly planning maintenance shutdowns at two of its facilities this month. These outages are expected to further tighten material availability, providing additional support to the ongoing price rally and reinforcing the bullish tone.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 76,450 t as of 6 April, based on vessel line-up data. Around 210,709 t of additional cargoes are expected by mid-April.

Export volumes: India’s bulk exports of HRCs touched 14,378 t as of 6 April.

Outlook

HRC and CRC prices are likely to remain firm or edge higher in the coming week, as planned mill shutdowns tighten spot availability and elevated raw material costs support mills’ pricing stance. Moreover, buying activity is expected to stay steady, largely driven by inventory replenishment, keeping the overall market bullish.

Leave a Reply