- Prices trend up in auctions across regions

- Primary mills increase HRC, CRC prices

CR busheling scrap auction results reveal an upward trend in prices across regions, with the western zone leading gains amid strong original equipment manufacturer (OEM) participation. Prices also firmed up at auctions held in the eastern and the northern regions, reflecting moderate supply and robust secondary mill demand.

Auctions in north India draw competitive premiums

Two key auctions in the final week of December supported a stronger price trend. A leading OEM in Gurugram sold 4,000 t of low-manganese CR-busheling under a seven-day lifting window at INR 36,300/t exw, while another OEM in Uttarakhand closed 1,000 t at INR 35,600/t. Both lots recorded higher bids of around 2,000-2,300/t compared with November as mills in Ludhiana stepped up procurement.

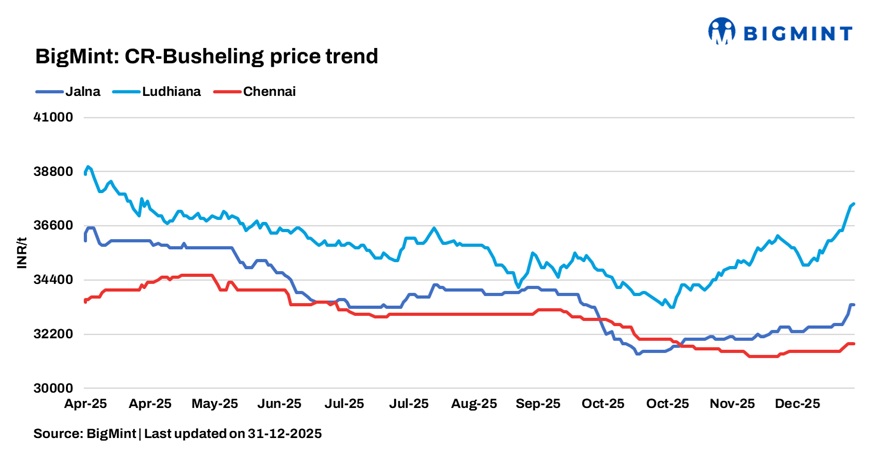

Prices reflect varied regional momentum in Dec’25

As per BigMint’s analysis, CR busheling scrap prices displayed positive trends across key hubs in December. The northern market, led by Ludhiana, recorded a strong upswing, with monthly average prices rising by INR 1,150/t m-o-m to INR 35,900/t DAP, supported by improved mill demand and tight supply. In contrast, western India’s Jalna market saw a moderate increase of INR 500/t m-o-m to INR 32,500/t, driven by active secondary melting operations, while in Chennai prices remained steady at INR 31,500/t amid balanced trade dynamics.

HRC, CRC trends

Indian steel producers maintained list prices in early December but introduced sequential increases later in the month, lifting prices by INR 750-1,000/t ($8-11/t) in mid-December and a further INR 750/t ($8/t) toward the end of the month. These consecutive hikes, supported by elevated raw material costs and improved market confidence during the year-end period, drove HRC and CRC trade prices sharply higher. Distributors reported moderate inventory levels, while sentiment across key trading hubs turned bullish. Meanwhile, the price gap between CRC and HRC narrowed to around INR 7,400/t ($82/t) in December from INR 8,087/t ($90/t) a month earlier.

Domestic scrap cheaper than imports

Imported CR-busheling arriving at Kandla and Mundra was assessed at CNF $372-375/t, equivalent to INR 33,500-33,600/t. After adding duties and inland freight, the delivered cost to Ludhiana and Mandi rose to INR 37,400-37,600/t. With domestic material available around INR 36,700/t DAP, the import-to-domestic price spread kept import bookings limited. Mills continued to prefer domestic scrap, reinforcing weak import demand into the prime-scrap segment.

Foundry scrap market

Foundry-grade ferrous scrap prices in India showed mixed trends during the last week of December, easing in western India amid ample supply while firming in southern and eastern India on improved buying interest and tighter availability. Kolhapur saw slight corrections, whereas Chennai recorded modest gains supported by steady automotive demand. Kolkata emerged strongest, with prices rising on limited supply. Overall sentiment stayed cautiously optimistic, underpinned by stable offtake from automotive, engineering, and the agricultural machinery segments.

Upcoming scrap auctions

Scrap supply outlook for Jan-Feb

CR-busheling availability is expected to remain stable for the next couple of months as most OEM auctions have concluded and lifting has commenced. However, scheduled maintenance shutdowns at select tier-1 mills in the third week of December may reduce generation in early January, potentially tightening supply for a brief period but it is unlikely to hamper the market or create any shortage. As auto sector performance in India is improving after GST rate cuts, demand in the coming months in expected to remain robust.

Leave a Reply