- West coast port stocks stand at over 237,000 t, weekly lifting close to 100,000 t

- Wide gap between import costs, domestic realisations suggests margin pressure

The Indian market for imported US high-calorific thermal coal is entering a phase of divergence. While international replacement costs have risen on the back of freight and tightening Atlantic supply dynamics, the prompt physical market in India, particularly along the Gujarat coast, remains weighed down by comfortable inventories and measured offtake.

At the same time, rising petcoke prices are reshaping fuel choices within the cement sector, creating a renewed but selective pull for high-CV coal.

Gujarat retail prices stabilise despite cost pressures

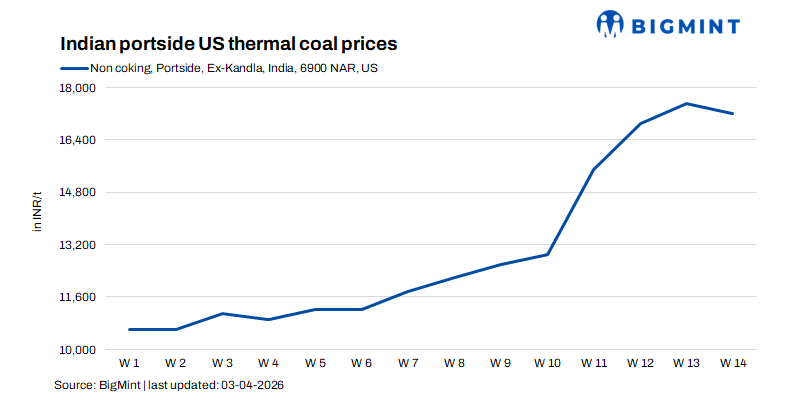

According to BigMint’s assessment, portside prices of US thermal coal (6,900 NAR) in India dropped by INR 300/t w-o-w to INR 17,200/t. Market feedback points to subdued trading activity, with limited fresh buying interest and thin margins for intermediaries. In some cases, sellers have been reluctant to push prices higher given the availability of prompt cargoes and cautious downstream demand.

Retail prices for US coal in Gujarat have remained broadly stable despite rising import costs. High-CV coal in the 6,700-6,900 NAR band was indicated in the range of INR 16,500-17,500/tonne (t) ex-Kandla and ex-Tuna on 3 April 2026, with most transactions clustering near the middle of this range.

In essence, the domestic market is decoupling from international cost escalation — at least in the short term — due to inventory comfort.

Ample stocks cap spot market

As of end-March, combined inventories of US-origin coal at the west coast ports stood at over 237,000 t, with the bulk concentrated at Kandla and the remainder at Tuna. Weekly lifting of close to 100,000 t indicates steady but not aggressive consumption, suggesting that the market is adequately supplied.

What is notable is the skew toward high-CV material, with most of the visible stock linked to premium US coal grades typically used in blending for cement kilns. Inventory remains distributed across multiple traders and stockists, with several vessels still carrying residual tonnage — particularly at Kandla — indicating that cargo absorption has lagged arrivals.

This stock overhang is directly influencing pricing behaviour in the retail market.

Freight, replacement costs move higher

On the supply side, the economics of bringing US coal into India have tightened. Freights from the US east coast to India have risen sharply, pushing delivered costs higher for both Northern Appalachian (NAPP) and Illinois Basin (ILB)-origin coal.

Earlier this week, a May-loading NAPP cargo was concluded at around $105/t FOB, indicating that replacement costs for high-CV US coal have already moved into triple-digit territory. ILB-linked material continues to trade at a discount to this level, but still reflects a structurally firm Atlantic basin.

When combined with elevated freights, the implied landed cost into India is significantly higher than prevailing portside retail prices.

This widening gap between replacement cost and domestic realisation suggests that traders are currently absorbing margin compression, rather than passing through the full cost increase to buyers.

Petcoke prices reshape fuel economics

The more important shift is taking place within the cement sector’s fuel mix.

Imported petcoke prices into India have risen to around $160/t CFR for higher-sulphur grades, with delivered costs trending even higher. Domestic petcoke prices have also moved up in response, tracking import parity.

This has materially increased fuel costs for cement producers. Estimates suggest a cost escalation of roughly INR 200-220/t of cement, prompting attempts to raise cement prices across regions. However, with demand growth still modest and pricing power limited, the ability to fully pass through these costs remains uncertain.

As a result, cement plants are increasingly optimising their fuel basket.

Coal gains share in cement kilns

With petcoke becoming more expensive, coal — particularly high-CV US coal — has regained relative competitiveness. Several plants are understood to be increasing their coal share, either by substituting petcoke partially or by optimising blends to reduce overall fuel costs. High-CV coal offers operational flexibility in this context, allowing kilns to maintain heat efficiency while managing sulphur and ash constraints.

At the same time, lower-CV coals from other origins continue to play a role in cost optimisation, particularly in regions where price sensitivity is higher. This has led to a more diversified fuel strategy across the sector rather than a wholesale shift.

Outlook: Coal to benefit, but selectively

In the near term, US high-CV coal is expected to retain its position in the Indian cement fuel mix, supported by elevated petcoke prices and the need for blending flexibility. However, the pace of demand recovery will depend on three factors: (1) inventory absorption at west coast ports, (2) direction of petcoke prices, and (3) the cement sector’s ability to pass through cost increases.

Until inventories tighten meaningfully, retail coal prices are likely to remain largely stable, even as international costs stay elevated. For now, the market is not short of coal – but it is increasingly short of cheap fuel.

Leave a Reply