- Tight supply and strong Chinese demand continue to support imported coal prices

- Coal inventories at Indian power plants drop w-o-w

Indian portside prices of Indonesian-origin thermal coal remained firm during the week ended 05 June 2026, with most imported grades holding near their highest levels in almost three years. The market continued to derive support from elevated international coal benchmarks, limited spot cargo availability, and increasing replacement costs.

Market participants learned that sentiment was strengthened by aggressive procurement from Chinese buyers and uncertainty surrounding Indonesia’s newly introduced export governance framework, prompting sellers to adopt a cautious approach toward fresh cargo commitments.

High-CV coal supported by tight spot availability

Prices of premium 5,000 GAR coal remained stable week-on-week at around INR 10,900/t at Kandla and INR 10,800/t at Visakhapatnam. Despite muted domestic buying activity, prices were supported by constrained spot availability from Indonesia, higher landed costs, and firm international benchmarks. Similarly, 4,200 GAR coal prices remained unchanged at approximately INR 9,000/t at Kandla and INR 8,900/t at Visakhapatnam, reflecting balanced market fundamentals and limited downside pressure.

Industrial demand lifts low-CV coal segment

The lower-calorific 3,400 GAR segment outperformed other grades, with prices rising by around INR 50/t week-on-week to nearly INR 6,850/t at Navlakhi. Demand from sponge iron manufacturers, brick kilns, and captive industrial consumers remained steady as buyers increasingly sought cost-efficient fuel alternatives amid elevated prices of higher-grade imported coal. This sustained industrial consumption continued to provide support to the lower-grade segment.

Indonesia’s export reforms create supply-side caution

Market participants remained focused on Indonesia’s new export governance mechanism, which came into effect on 1 June 2026. Although the framework is designed to improve pricing transparency, strengthen compliance, and safeguard export revenues without disrupting trade flows, the transition period has introduced operational uncertainty across the supply chain. Exporters have reportedly adopted a cautious stance on releasing fresh tonnage until greater clarity emerges regarding implementation procedures, resulting in tighter spot market liquidity and supporting coal prices.

Freight costs ease but remain elevated

Freight rates for Supramax vessels from East Kalimantan to India’s west coast softened marginally during the week. However, freight costs remain elevated relative to long-term averages, continuing to increase landed coal costs for Indian importers and limiting the scope for any meaningful correction in domestic portside prices.

Port stocks signal adequate availability

Thermal coal inventories at major Indian ports increased marginally to 15.61 million tonnes during Week 22, indicating comfortable overall supply availability. However, inventory accumulation reflects cautious procurement behaviour rather than weak supply. Industrial consumers largely restricted purchases to immediate requirements, while traders avoided significant inventory build-up ahead of the monsoon season and amid prevailing policy uncertainty in Indonesia.

Declining power plant stocks expose distribution challenges

Coal inventories at Indian thermal power plants declined w-o-w to around 48 million tonnes, equivalent to approximately 16 days of consumption. Despite adequate coal availability at ports and within the broader supply system, nearly 25 power plants continued to operate with critical stock levels. This highlights persistent logistical bottlenecks, regional supply mismatches, and inefficiencies in coal evacuation and distribution rather than an outright shortage of material at the national level.

Global market fundamentals remain supportive

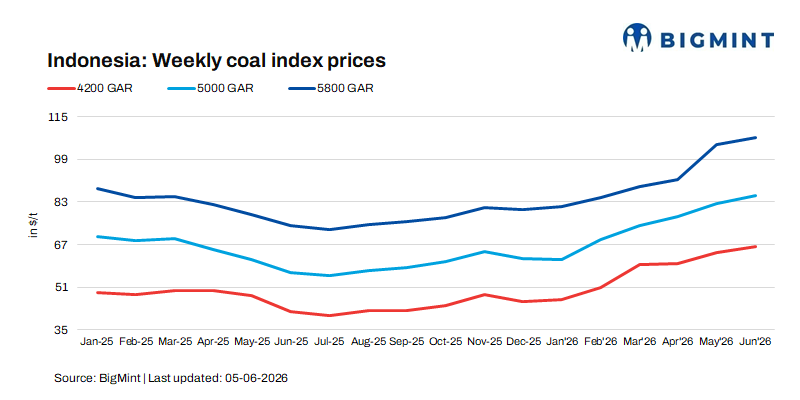

The international thermal coal market continued to exhibit resilience, underpinned by steady Asian demand and tightening availability of Indonesian spot cargoes. Benchmark 5,800 GAR coal prices increased marginally by around $0.5-1/t w-o-w, while 4,200 GAR rose marginally by $1/t and 3,400 GAR grades rose by approximately $0.5/t.

Strong procurement interest from China and other regional consumers has helped offset softer demand from certain import markets. The resulting firmness in seaborne coal prices has continued to support Indian portside values despite relatively cautious domestic purchasing activity.

Outlook

The Indian thermal coal market is expected to maintain a firm-to-stable trend in the near term. Continued uncertainty surrounding Indonesia’s export policy implementation, limited spot cargo availability, and sustained Chinese buying interest are likely to keep replacement costs elevated and support imported coal prices.

While comfortable port inventories, seasonal monsoon-related demand moderation, and cautious procurement strategies may restrict significant price upside, any disruption to Indonesian export flows or further tightening in seaborne supply could provide additional upward momentum.

Overall, prices are expected to remain well supported, with market participants closely monitoring Indonesian export developments and regional demand trends for further direction.

Leave a Reply