- Portside South African coal prices trading at one-year highs

- Trades remained selective despite higher prices

South African thermal coal prices at Indian ports have strengthened sharply month to date, as of 23 January, reaching one-year highs as persistent stock tightness, firmer global indices, and higher freight costs continued to push offers upward. Despite higher prices, trade activity remained selective, with only needy buyers concluding deals, while the broader market stayed cautious amid comfortable domestic coal availability.

Portside prices surge on sustained tightness

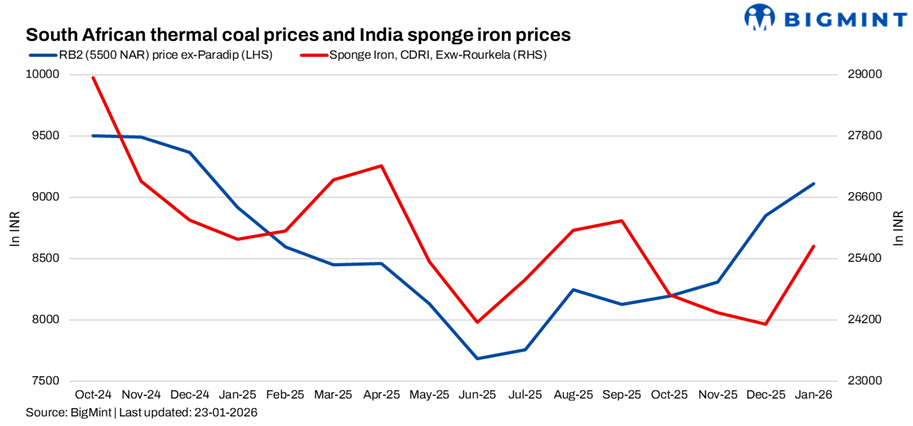

As per BigMint’s assessment, exw-Paradip 5,500 NAR rose to INR 9,400/t, up INR 250/t w-o-w, while 4,800 NAR increased to INR 8,100/t, gaining INR 300/t w-o-w. At Vizag, 5,500 NAR climbed to INR 9,250/t, up INR 250/t w-o-w, and 4,800 NAR jumped to INR 7,950/t, marking a sharper INR 350/t w-o-w rise. Portside offers across locations touched one-year highs during the month, reflecting prolonged supply-side stress rather than a sudden demand spike.

Although offers moved aggressively higher, transactions remained limited. A few deals for 5,500 NAR were reportedly concluded around INR 9,000-9,100/t exw, largely by buyers covering immediate requirements. Broader buying interest stayed restrained, with most consumers adopting a wait-and-watch approach amid elevated prices.

Export market strength feeds into Indian prices

On the export front, sentiment remained firm. RBCT-origin 5,500 NAR FOB offers hovered around $79-80/t, while CFR India levels were indicated near $93-94/t. For 4,800 NAR, CFR India prices were quoted in the range of $77-79/t. Market sources continued to flag tight January-February cargo availability, as several South African cargoes were diverted towards South American destinations, reducing prompt supply into Asia.

Rising API4 benchmarks and higher freight rates further inflated landed costs, particularly for RB3 material, reinforcing higher portside offers in India. Participants widely expected stock tightness and elevated offers to persist through March, given limited export availability and slow replenishment at Indian ports.

Domestic coal stable, sponge iron offers support

In contrast, domestic non-coking coal prices remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t, providing buyers with a relatively cheaper alternative. This continued to cap aggressive spot buying of imported coal despite the supply squeeze.

Sponge iron prices offered some cost-side support to imported coal. Sponge Iron CDRI, exw-Rourkela, increased by INR 250/t w-o-w to INR 26,250/t. However, demand response remained measured, as buyers balanced higher input costs against uncertainty in finished steel markets.

Outlook

South African thermal coal prices at Indian ports are expected to remain firm in the near term, supported by tight export availability, higher global indices, and persistent portside stock constraints. Market participants anticipate elevated offers through March, though deal activity is likely to stay selective, with only urgent demand translating into trades amid ample domestic coal supply and cautious procurement behaviour.

Leave a Reply