- FOB offers dip on muted Indian demand, despite high freights

- Portside stocks decline 7% w-o-w amid active stock clearance

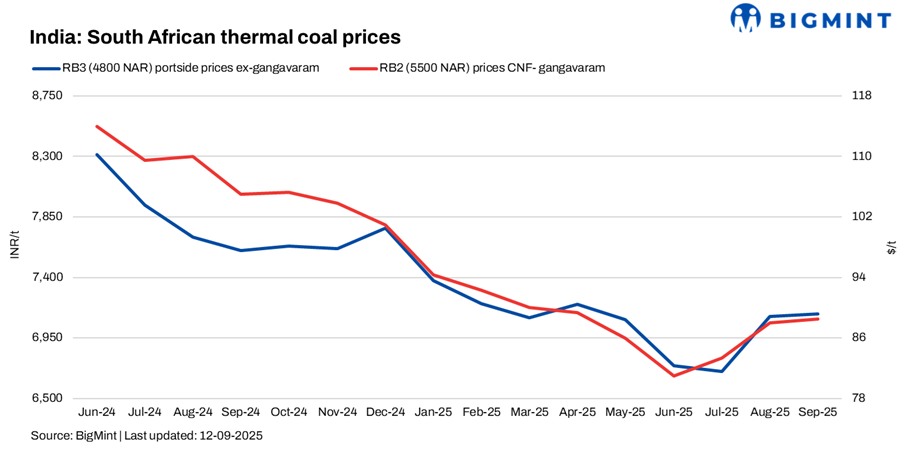

Indian portside South African thermal coal prices registered sharp declines this week. At Vizag, RB2 fell by INR 650/tonne (t) w-o-w to INR 7,750/t, while RB3 slipped INR 500/t to INR 6,800/t. At Gangavaram, RB2 dropped INR 400/t to INR 7,900/t and RB3 decreased INR 300/t to INR 6,900/t. Prices weakened as traders rushed to liquidate stocks ahead of the 22 September GST implementation, with cess burdens accelerating pressure selling and leading to uncertain offers in the market.

In a recent deal, a trader sold around 10,000 t of RB2 at INR 8,000/t ex-Mangalore. Some deals were also heard concluded at the Vizag Port at a lower rate.

“Traders are trying to clear their books ahead of the new GST rates implementation. Hence, we are selling off inventories at lower prices,” stated a participant from a trading house.

India’s portside thermal coal inventories slipped 7.1% w-o-w to 12.10 million tonnes (mnt) in Week 36 from 13.03 mnt in the previous one, reflecting slower arrivals and active stock clearance.

Export offers

South African FOB Richards Bay offers eased modestly, as overseas sellers reacted to thin Indian demand and portside selling. RB2 was assessed at around $71/t FOB and RB3 near $60/t FOB, softer by $1/t w-o-w. High ocean freights kept quotes firm, but the domestic rush to sell ahead of the GST change reduced near-term buying appetite, leaving export bids largely static to a touch weaker.

Domestic market

Domestic coal tags held at current levels amid the uncertainty. BigMint assessed 5,000 GCV at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. SECL e-auctions and spot activity witnessed muted bidding behaviour this week, with no broad uptick in bids. Most buying remained need based.

Sponge iron market

In the sponge iron market, BigMint’s C-DRI index (ex-Rourkela) inched up by INR 150/t w-o-w to INR 26,200/t. However, demand stayed subdued, and transactions were mostly concluded at lower ranges, highlighting weak sentiment and a lack of price clarity. Overall, the market remained under selling pressure, with participants restricting purchases to immediate needs and avoiding bulk bookings.

Outlook

The market will likely stay volatile into the GST transition on 22 September as sellers race to clear inventories and buyers hold off bookings in expectation of fresh offers. There is likely to be continued pressure on portside prices and thin, opportunistic trades; export bids may remain soft until Indian buying resumes. Post-deadline, volatility should persist while participants digest the tax impact and adjust price sheets.

Leave a Reply