- Freight hikes wipe out August cargo availability

- Portside inventories drop 5% w-o-w in Week 30

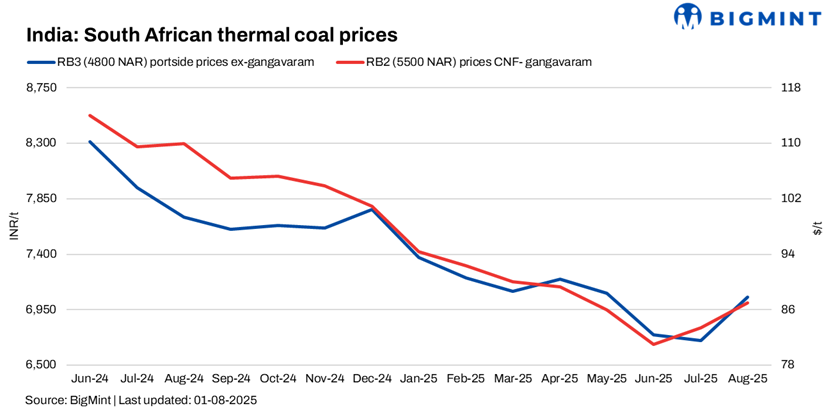

Indian portside offers for South African thermal coal surged this week, with traders citing a sharp increase in freights and expectations of further price hikes. BigMint assessed RB2 (5500 NAR) at INR 8,100/tonne (t) and RB3 (4800 NAR) at INR 7,050/t exw-Gangavaram – up by INR 300/t and INR 250/t w-o-w, respectively.

However, the most aggressive rise was seen at Vizag, where RB2 jumped INR 650/t d-o-d to INR 8,500/t, and RB3 rose INR 350/t d-o-d to INR 7,200/t. No offers below INR 8,500/t were heard for RB2 at Vizag, amid tight vessel supply and a steep rise in Panamax freights over the past week.

Notably, Panamax freights from Richards Bay, South Africa, to Paradip, India, rose by $1.3/dry metric tonne (dmt) w-o-w to $16.33/dmt.

Freight hikes wiped out August cargo availability, and traders are now actively offering September shipments, expecting continued firmness. A few sponge iron producers have started booking in advance, banking on demand recovery post-monsoon.

Portside thermal coal inventories fell by 5.3% w-o-w to 14.77 mnt in Week 30, reflecting lower fresh arrivals.

Export offers also strengthened – RB2 rose by $1.5/t w-o-w to $71.5/t, while RB3 gained $2/t to $59.5/t FOB South Africa, amid tight loading windows at Richards Bay.

Domestic coal prices continued their uptrend despite weak sentiment. BigMint assessed 5000 GCV at INR 5,000/t and 4500 GCV at INR 4,400/t exw-Bilaspur, both up by INR 150/t w-o-w. Reduced SECL auctions due to monsoon disruptions led to tightened supply.

However, the sponge iron market turned slightly cautious. BigMint’s C-DRI assessment for ex-Rourkela dropped INR 700/t w-o-w to INR 25,800/t as of 1 August, with buyer inquiries remaining subdued. Sellers attempted to revive interest through selective price adjustments but saw limited success.

Outlook

Portside South African coal offers are expected to stay firm, particularly at active trading hubs such as Vizag, where no fresh August material is available. If freights continue to rise and September cargo interest builds up, RB2 offers may climb further. Domestic buying could improve post-monsoon, especially if sponge iron production picks up. However, short-term activity may still be range-bound amid resistance to higher landed costs.

Leave a Reply