- Logistics disruptions in South Africa push up prices

- Thermal coal stocks at Indian ports remain firm w-o-w

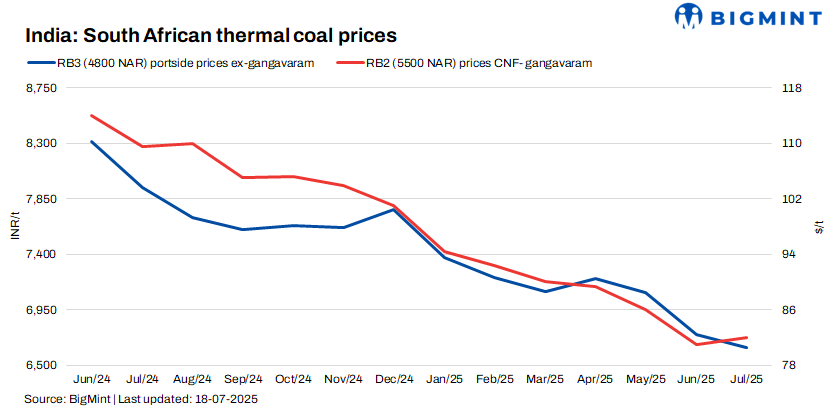

Portside prices for South African thermal coal continued to increase this week amid severe supply disruptions in South Africa. Two major rail lines were down, and maintenance at the Richards Bay Coal Terminal (RBCT) is scheduled for 20-25 days, disrupting inbound flow for nearly a month.

BigMint assessed RB2 (5500 NAR) at INR 7,650/tonne (t) and RB3 (4800 NAR) at INR 6,650/t exw-Gangavaram, up by INR 50/t w-o-w. Index levels surged, but actual buying was thin, with no major deals heard amid tepid demand and fluctuating offers.

South African export offers saw mixed trends, with RB2 (FOB Richards Bay) rising by $1.5/t w-o-w to $69/t, while RB3 fell by $0.5/t to $56/t.

Portside inventories stable w-o-w

Portside thermal coal inventories in India remained largely unchanged at 15.84 mnt in Week 28 versus 15.92 mnt the previous week, as steady arrivals matched sluggish offtake.

Domestic coal prices unchanged amid limited activity

Domestic coal prices remained flat w-o-w, with BigMint assessing 5000 GCV and 4500 GCV grades at INR 4,700/t and INR 4,250/t exw-Bilaspur. SECL’s latest auction saw improved response for select high-grade lots, but most bids for grades hovered close to notified levels, reflecting cautious procurement amid steady supply and subdued end-user buying.

Sponge iron prices ease as prior bookings weigh

The sponge iron market remained quiet, with C-DRI prices falling by INR 700/t w-o-w to INR 24,800/t exw-Rourkela. Buying interest was moderate, as many participants had secured material in earlier weeks at lower prices.

Outlook

South African coal prices may remain supported due to ongoing logistics issues in South Africa and RBCT maintenance. However, weak demand and high domestic availability in India are likely to limit aggressive price movements. Traders are expected to adopt a wait-and-watch approach until fresh demand signals emerge.

Leave a Reply