- Cautious market sentiment leads to need-based buying

- Domestic coal prices fall, limiting demand for imports

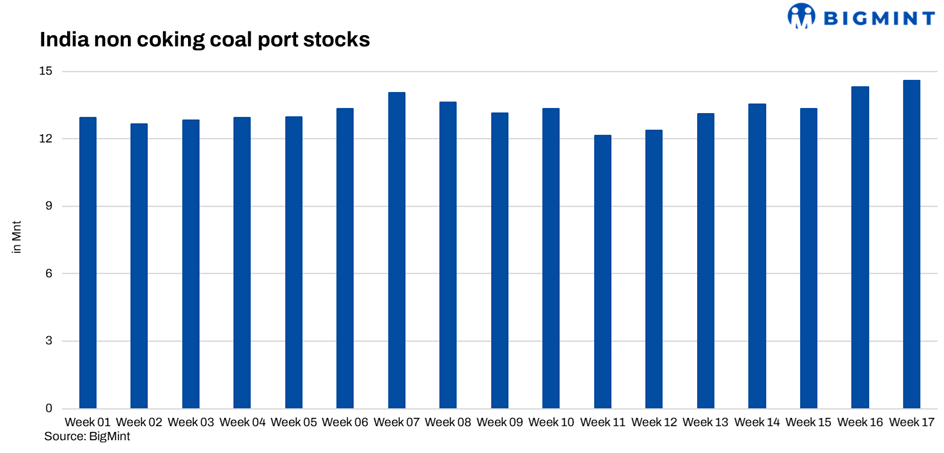

India’s non-coking coal inventories at major ports increased slightly by 2.1% in Week 17 (ended 25 April) to 14.60 mnt from 14.30 mnt in Week 16, indicating continued supply availability amid weak demand conditions. The rise remained modest compared with the previous week, suggesting that while cargo inflows continued, evacuation also remained active. Overall market sentiment stayed cautious, with buyers continuing to procure on a need basis amid falling prices across both domestic and imported coal segments.

Mixed port trends reflect balanced inflow, evacuation

Port-level trends remained mixed, highlighting a balanced market. Select ports witnessed inventory build-up supported by fresh arrivals and trader stocking, while others recorded drawdowns due to ongoing consumption and limited new inflows.

Gains at ports such as Dhamra, Haldia, Kakinada, Magdalla, and Tuna reflected continued cargo positioning, particularly by traders and industrial consumers. On the other hand, declines at Gangavaram, Krishnapatnam, Kandla, and Mundra indicated reduced arrivals and steady evacuation. Paradip remained largely stable, pointing towards balanced supply-demand dynamics at key east coast hubs.

Overall, the movement of stocks suggested no aggressive accumulation, but rather routine adjustments based on regional demand and logistics.

Weak demand across sectors weighs on sentiment

Coal market sentiment remained subdued during the week, with weak industrial buying activity. Sponge iron and steel prices weakened, with procurement remaining largely requirement-based.

Portside South African coal prices softened amid weak enquiries, while Indonesian low-CV coal continued to face demand pressure. US coal prices declined further, even as significant volumes remained in transit to India, indicating comfortable near-term supply.

Domestic coal correction impacts import demand

Domestic coal prices declined sharply following lower bids in the recent SECL auction, driven by liquidity constraints and cautious participation. This increased the competitiveness of domestic coal, leading buyers to shift away from imports.

The correction in domestic prices, combined with adequate portside inventories, further reduced interest in imported cargoes. Traders also remained cautious in building positions, given the weak downstream demand and uncertain price direction.

Supply remains comfortable; outlook cautious

The marginal rise in inventories suggests that supply remains sufficient in the near term. Continued arrivals, along with cargoes already in transit, are likely to keep stock levels comfortable across ports.

However, weak demand conditions and falling prices across segments may limit any significant build-up in the coming weeks. Market participants are expected to remain cautious, with buying activity driven mainly by immediate requirements rather than stock-building.

Going forward, recovery in industrial demand and clarity in domestic pricing trends will be key factors influencing inventory movement and overall market sentiment.

Leave a Reply