- Coal inventories at Indian thermal power plants fell sharply by around 6% w-o-w

- High inventories and weak demand may cap further gains

Indian portside prices for Indonesian-origin thermal coal rose sharply week-on-week as of 22 May 2026, with gains of INR 300-500/t recorded across major calorific value (CV) grades. The increase was primarily driven by the continued depreciation of the Indian rupee against the US dollar, with the exchange rate hovering near historic lows of over INR 96/USD. It also dropped to 96.6 against $ earlier this week.

The weaker currency significantly inflated import parity costs for Indian buyers, even as international coal benchmarks and freight markets remained firm. Rising Indonesian index price levels further reinforced the upward pressure on landed coal costs.

Higher-CV grades witness strongest gains amid tight availability

Among key imported grades, high-grade 5,000 GAR coal prices increased by nearly INR 500/t w-o-w to around INR 10,800/t at Kandla and INR 10,700/t at Visakhapatnam, supported by limited spot availability and stronger replacement costs.

Mid-grade 4,200 GAR coal prices also rose sharply by approximately INR 400/t to INR 8,400/t at Kandla and INR 8,300/t at Visakhapatnam. Meanwhile, lower-grade 3,400 GAR coal prices advanced by nearly INR 350/t to around INR 6,450/t at Navlakhi, supported by firm low-rank coal demand from sponge iron and industrial consumers.

Indonesia’s proposed export reform creates market uncertainty

Yesterday, the Indonesian government announced that it is set to introduce a new regulatory framework aimed at centralising natural resource (SDA) exports under State-Owned Enterprises (BUMN). The transition will be implemented progressively throughout 2026, significantly reducing the role of private exporters in overseas trade activities.Market sentiment also remained influenced by Indonesia’s proposed regulatory overhaul aimed at centralizing coal exports under State-Owned Enterprises (BUMN). Under the phased transition plan scheduled throughout 2026, the role of private exporters in overseas coal trade is expected to reduce progressively.

However, as per updates received today, the implementation has been delayed till next year. Effective 1 January 2027, private companies may no longer be permitted to directly export coal to international buyers. All export-related operations — including contracts, customs processing, shipment handling, and payment settlements — are expected to be routed exclusively through BUMN-controlled channels.

The proposed policy has created concerns among Indian importers regarding reduced pricing flexibility, tighter spot availability, and possible shipment disruptions during the transition phase. However, market participants largely believe that major supply disruptions remain unlikely, given India’s structural dependence on Indonesian coal due to its competitive pricing, favourable freight economics, and geographical proximity.

Another market participant noted that the policy initiative is also aimed at Indonesia’s tightening financial oversight and curbing capital outflows linked to offshore shell entities associated with miners and traders, particularly amid ongoing pressure on the Indonesian currency and the country’s export-driven economic structure.

Freight costs add further support to portside prices

Freight markets also contributed significantly to the bullish pricing environment. Supramax freight rates from East Kalimantan to Navlakhi increased by around $1/t w-o-w to nearly $22/t, further elevating landed import costs. Higher bunker fuel prices and expectations of increased inland transportation expenses during the upcoming monsoon season continued to support freight sentiment.

Port inventories decline, but overall supply remains comfortable

India’s thermal coal inventories at major ports declined by 4.5% w-o-w during week 20 to around 15.16 mnt, compared with 15.87 mnt in the previous week, indicating improved cargo evacuation across key ports. Despite the decline, inventory levels remained relatively comfortable overall, reflecting cautious procurement activity amid subdued industrial demand and adequate domestic coal availability.

Thermal coal stocks fall amid supply imbalances

Coal inventories at Indian thermal power plants fell sharply by around 6% w-o-w to nearly 50 mnt as of 21 May, equivalent to roughly 16 days of consumption. However, stock distribution remained uneven across regions and plant categories. Around 22 thermal power plants continued operating at critical inventory levels, including facilities dependent on domestic coal, imported coal, and washery rejects, highlighting persistent logistical inefficiencies and regional supply imbalances despite healthy aggregate national stock levels.

Strong international market fundamentals continue to support prices

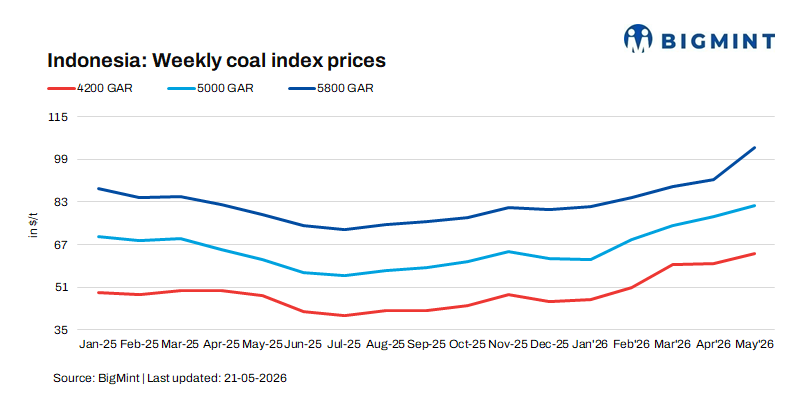

International thermal coal markets also maintained firm undertones during the week, supported by stronger Asian demand and tightening Indonesian spot availability. Benchmark 5,800 GAR coal prices increased sharply by around $2-2.5/t week-on-week, while 4,200 GAR coal prices remained largely stable. Lower-grade 3,400 GAR coal prices also strengthened modestly by around $0.5-1/t, further supporting bullish sentiment across the Indian import market.

Outlook

Indian portside thermal coal prices are expected to remain firm, supported by rupee weakness, higher freight costs, firm global benchmarks, and uncertainty over Indonesia’s export policy transition. However, comfortable inventories and subdued demand may limit further sharp price increases.

Leave a Reply