- Muted industrial demand keeps buying activity low

- Adequate portside and power plant stocks limit price movement

Indian portside prices of Indonesian-origin thermal coal remained largely stable w-o-w as of 17 April, reflecting subdued buying interest across key consuming sectors. Market participants reported limited bulk trade activity, with transactions largely restricted to need-based procurement.

Weak demand from the ceramic sector, particularly in Morbi, Gujarat – India’s largest ceramic manufacturing hub – continues to weigh on market sentiment. However, industry sources indicate that some ceramic units are likely to gradually resume operations by next month, which may lend some support to demand in the near term.

Portside prices stable across key grades

Portside prices across major Indonesian coal grades showed limited movement during the week. According to latest BigMint assessment, 5,000 GAR Indonesian coal prices remained stable at around INR 9,300/t at Kandla and INR 9,200/t at Visakhapatnam.

Similarly, 4,200 GAR coal prices held steady at around INR 7,550/t at Kandla and INR 7,450/t at Visakhapatnam. Meanwhile, lower-grade 3,400 GAR coal prices edged down marginally by around INR 50/t w-o-w to nearly INR 5,250/t at Navlakhi Port, reflecting softer demand for lower-calorific cargoes.

Portside coal inventories ease slightly

India’s portside thermal coal inventories declined modestly in week 15, falling by 1.5% w-o-w to 13.33 mnt compared with 13.53 mnt in the previous week. The marginal correction follows consecutive inventory build-ups in earlier weeks and was primarily driven by slower cargo arrivals and ongoing evacuation at select ports.

Inventory trends remained mixed across regions, with some ports witnessing stock accumulation supported by steady inflows, while others recorded drawdowns due to continued consumption and limited fresh arrivals. Overall, stock movement remained dynamic, reflecting a balance between incoming supply and evacuation, while buyers continued to adopt a cautious procurement approach.

Thermal power plants maintain comfortable stock levels

Coal inventories at Indian thermal power plants declined slightly during the week but remain broadly comfortable. As of 15 April, total coal stocks at thermal power plants stood at around 58.83 mnt, equivalent to nearly 19 days of consumption. Nevertheless, inventory distribution across plants remains uneven. Around 18 thermal power plants are currently operating with critical stock levels, including nine dependent on domestic coal supply, six reliant on imported coal, and three operating on washery rejects, indicating localised supply pressures despite adequate overall availability.

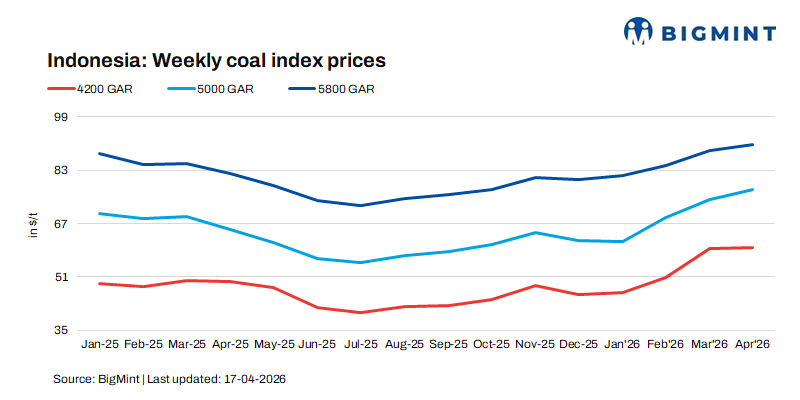

Global coal benchmarks edge up; freight rates rise

International coal market indicators presented mixed signals during the week. Indonesian benchmark prices increased marginally following stronger Asian demand and tighter supply conditions. Prices of 5,800 GAR coal rose by around $1-2/t w-o-w, while 4,200 GAR coal gained approximately $0.5-1/t.

Meanwhile, 3,400 GAR coal prices remained largely stable, even as Indonesia’s HBA benchmark for this grade reached record levels.

On the logistics side, freight costs increased modestly, with Supramax freight rates from East Kalimantan to Navlakhi rising by about $1.6/t w-o-w to approximately $19.9/t.

Outlook

In the near term, Indian portside prices of Indonesian thermal coal are expected to remain largely rangebound, supported by stable international benchmarks but capped by weak domestic spot demand. Market activity may gradually improve if ceramic manufacturing units in Morbi resume operations as anticipated and seasonal power demand strengthens ahead of the summer peak. However, comfortable coal inventories at thermal power plants and cautious procurement strategies by buyers may continue to limit any sharp price movements in the short term.

Leave a Reply