- Cautious, need-based buying persists

- Price upside remains limited

Indian portside prices of Indonesian-origin thermal coal recorded mixed movements on a week-on-week (w-o-w) basis during the week ended 23 January 2026, against the backdrop of persistently subdued spot demand across major calorific grades. While select grades witnessed marginal price firming, overall market momentum remained weak due to limited buying interest.

As per BigMint assessments, prices of 5,000 GAR coal increased by INR 50/t w-o-w to INR 7,250/t at Kandla and INR 7,150/t at Vizag. In contrast, 4,200 GAR coal prices declined by INR 50/t to INR 5,600/t at Kandla and INR 5,500/t at Vizag, reflecting weaker demand from industrial consumers and thin spot trading activity. Lower-grade 3,400 GAR coal prices rose by INR 50/t w-o-w to INR 4,500/t at Navlakhi, supported by limited availability and replacement-driven purchases.

Demand conditions and market sentiment

Market sentiment remained cautious throughout the week, with buyers largely restricting procurement to immediate operational requirements. Weak industrial offtake, coupled with seasonal disruptions and adequate stock positions, continued to suppress spot demand.

Market participants indicated that Indonesian thermal coal prices are currently stable with limited volatility; however, sellers are quoting higher offers in anticipation of price support from upstream benchmarks. Despite this, most transactions are being concluded at lower levels, as buyers maintain strong price resistance and prioritise need-based buying strategies.

Freight market dynamics

Seaborne freight rates exhibited minimal movement during the week, consistent with subdued cargo booking activity. BigMint assessed Supramax freight rates from East Kalimantan to Navlakhi at $10.8/dmt, broadly stable on a w-o-w basis. The lack of significant freight fluctuations reflects balanced vessel availability and limited incremental demand for coal shipments.

Inventory position at ports

India’s portside thermal coal inventories increased marginally by 1.4% w-o-w to 12.83 million tonnes (mnt) in week 4 of 2026 (12-17 January), compared with 12.65 mnt in week 3. Inventory trends varied across ports, as selective arrivals led to replenishment at certain locations, while faster evacuation at others prevented a broader stock build-up. Overall, inventory levels remained largely balanced and sufficient to meet near-term requirements.

Power sector stock levels

Coal inventories at Indian thermal power plants rose marginally by 0.8% w-o-w to 53.98 mnt as of 21 January 2026, translating into approximately 18 days of consumption cover. While national inventory levels remain comfortable, around 15 power plants continue to operate under critical stock conditions. These constraints are primarily attributable to logistical challenges and coal quality mismatches, rather than any structural shortage in coal supply.

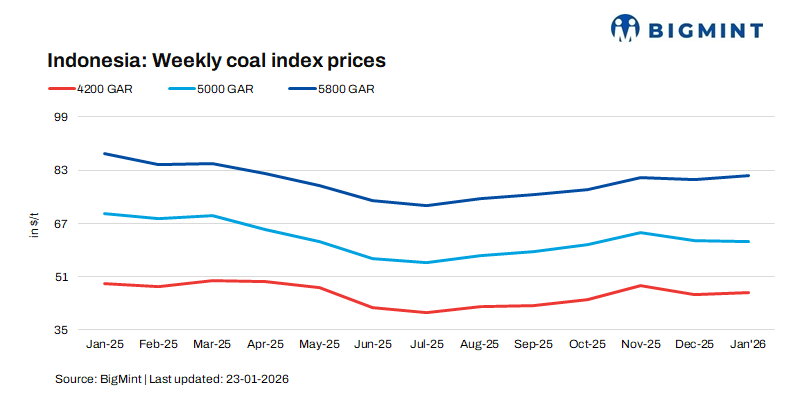

Indonesian benchmark price movements

Indonesian weekly benchmark prices registered modest gains during the week, with 5,800 GAR increasing by $0.04/t, 4,200 GAR by $0.23/t, and 3,400 GAR by $0.69/t on a w-o-w basis. However, these upstream price increases had limited pass-through into Indian portside markets, as cautious buying behaviour, adequate domestic coal availability, and comfortable inventory levels continued to cap upside potential.

Market outlook

Indian portside thermal coal prices are expected to remain muted in the near term, with only limited upside. Weak industrial demand, adequate inventories, and need-based buying are likely to cap price gains. In the absence of stronger demand or tighter supply conditions, market sentiment is expected to remain cautious.

Leave a Reply