- Buyers delay purchases, expecting lower prices post 22 Sep

- Indonesian tags inch up on demand recovery in some regions

The Indian portside market for Indonesian thermal coal remained stable during the week ending 19 September 2025, with participants largely adopting a wait-and-watch approach ahead of the upcoming GST reforms deadline.

BigMint’s assessments showed the 5000 GAR grade unchanged at INR 6,950/t in Kandla and INR 6,850/t in Vizag. Similarly, the 4200 GAR grade was stable at INR 5,650/t in Kandla and INR 5,550/t in Vizag, while the 3400 GAR grade held firm at INR 4,200/t in Navlakhi.

Market participants noted that fresh deals were limited, as most buyers deferred procurement until after 22 September, when cargoes are expected to become cheaper due to reduced cess under the new GST framework. This anticipation temporarily curbed transaction volumes despite steady portside prices. A few traders may have sold material by reducing offers by INR 100-200/t to clear stocks; else, the market was mostly stable.

Freight market pressured by oversupply

Supramax freights on the Indonesia (East Kalimantan)-India (Navlakhi) route softened by $0.25/t w-o-w to $15.71/dmt. The decline was primarily attributed to an oversupply of vessels in the market and muted Indonesian export demand, which heightened competition among carriers. Volatility in fuel costs added to the downside pressure, keeping freight levels under strain.

Power plant inventories decline

Coal inventories at Indian power plants stood at 48.91 mnt as of 18 September 2025, sufficient for 16 days of consumption. Stocks declined w-o-w, with 16 plants falling under the critical stock category. This included eight plants reliant on domestic coal, seven dependent on imported coal, and one using washery rejects. The dip in inventories signals rising fuel supply concerns amid limited arrivals.

Portside inventories hit 6-month low

India’s portside thermal coal inventories slipped 1.8% to 11.88 mnt in week 37 from 12.10 mnt in the previous week. This marked the lowest level in six months, driven by sluggish arrivals and muted demand from steel and sponge iron producers. Elevated import offers, combined with weak trade sentiment, continued to discourage fresh bookings and weighed on replenishment activity at ports.

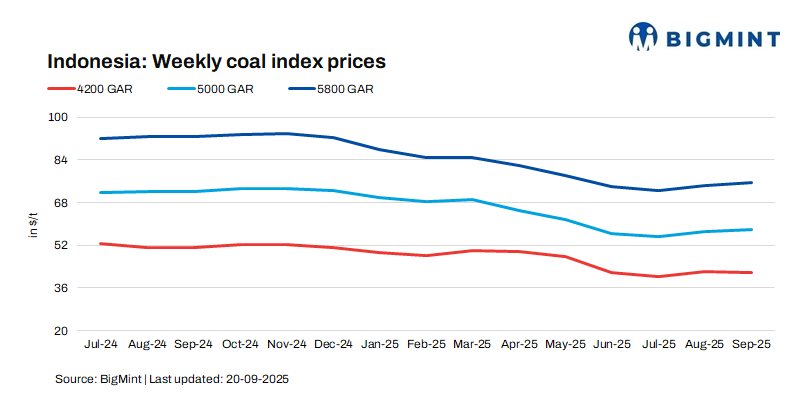

Global market registers modest gains

Contrasting with India’s subdued domestic conditions, international Indonesian coal prices posted modest gains during the week. The 5800 GAR grade rose by $0.17/t w-o-w to $75.61/t, the 4200 GAR grade increased by $0.63/t to $42.53/t, and the 3400 GAR grade edged up by $0.15/t to $30.34/t. These gains were supported by selective regional demand recovery and tightening supply pockets, although the overall momentum remained limited.

Outlook

India’s portside coal market is likely to stay subdued as buyers delay procurement ahead of GST cess cuts, with high import offers and weak industrial demand limiting activity. Globally, Indonesian coal prices could edge higher on regional demand, though gains will be capped by weak Chinese buying and ample vessel supply.

Leave a Reply