- Stock liquidation drives market ahead of 22 Sept GST deadline

- Weak demand, rupee depreciation likely to cap post-cess price gains

The Indian portside market for Indonesian thermal coal reflected mixed sentiment during the week ending 5 September 2025. BigMint’s assessments indicated that the 5000 GAR grade slipped by INR 50/t to INR 7,100/t at Kandla and INR 7,000/t at Vizag.

The 4200 GAR grade held firm at INR 5,700/t at Kandla and INR 5,600/t at Vizag, while the 3400 GAR grade softened by INR 50/t to INR 4,400/t at Navlakhi.

Stock liquidation ahead of GST deadline

Market participants emphasized the need to clear inventories before 22 September when the 18% GST cess will come into effect. Higher inventory levels continue to be concentrated in low- and mid-GAR material, while availability of high-GAR coal remains limited.

Market participants noted that failure to liquidate stocks on time would compel sellers to add INR 400/t to recover cess costs, thereby lifting overall prices. In the interim, no significant imports or large transactions are anticipated, with the market largely in a wait-and-watch mode.

Price volatility driven by policy uncertainty

The forthcoming cess has created volatility, with portside prices fluctuating by INR 50-100/t across grades. Sufficient stock levels and subdued procurement appetite from end-users have contributed to recent downward corrections. The uncertainty around post cess pricing has further restrained active trade in the spot market.

Currency weakness adds to market pressure

The sharp depreciation of the Indian rupee has compounded challenges for importers. The exchange rate touched an all-time low of INR 88.15/USD, magnifying landed cost pressures at a time when demand remains muted.

Freight market strengthens despite thin fixtures

Shipping rates moved higher despite sluggish activity. Supramax freights on the Indonesia (East Kalimantan) – India (Navlakhi) route climbed by $0.8/t w-o-w to $17.75/dmt. The gains were underpinned by tight vessel supply, firmer bunker costs, and shipowners resistance to lower bids, supported by expectations of improved Indian coal demand later this month.

Portside inventories ease on lower arrivals

India’s portside coal inventories declined by 5.4% w-o-w, falling to 13 mnt in week 35 from 13.78 mnt in week 34. Lower arrivals contributed to this drop, while elevated import offers, weakness in the steel market, and subdued domestic demand curbed fresh bookings.

International market trends point to softness

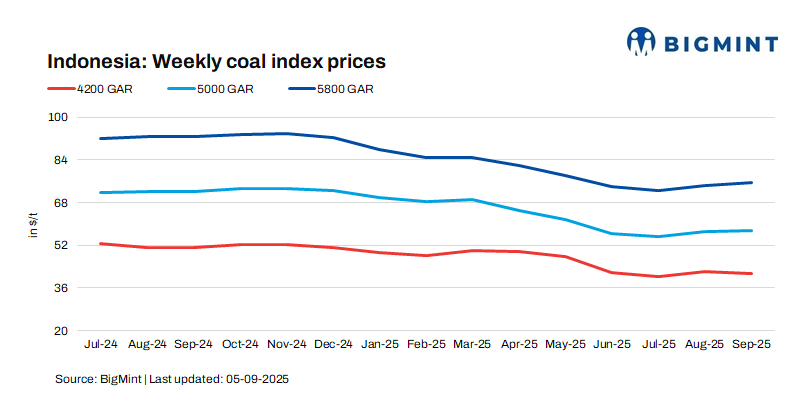

In contrast to domestic firmness, the international market for Indonesian coal registered modest declines. The 5800 GAR grade edged down by $0.09/t to $75.31/t, the 4200 GAR grade slipped by $1.04/t to $41.28/t, and the 3400 GAR grade dropped by $0.64/t to $30.10/t.

Outlook

The portside coal market will likely remain subdued until the 22 Sep’25 GST deadline, with sellers focused on stock liquidation. Post-cess costs may lift prices briefly, but weak demand, a soft rupee, and limited buying keep sentiment volatile with a downside bias.

Leave a Reply