- Weak demand, cautious sentiment limit price movements

- Power plant stocks ease by 1% but remain adequate overall

Indian portside prices of Indonesian-origin thermal coal remained largely stable w-o-w during the week ended 9 January 2026, as subdued spot buying activity continued across key grades.

Market participants largely adopted a wait-and-watch approach, supported by comfortable inventory levels at ports and cautious near-term demand expectations, particularly from the power and industrial sectors.

According to BigMint’s assessments, prices of 5,000 GAR coal were unchanged w-o-w at INR 7,200/t at Kandla and INR 7,100/t at Vizag, reflecting the absence of aggressive buying interest. Meanwhile, 4,200 GAR coal prices softened marginally by INR 50/t to INR 5,650/t at Kandla and INR 5,550/t at Vizag amid limited trade activity. Lower-grade 3,400 GAR coal also remained stable at INR 4,450/t at Navlakhi, supported by steady offtake from price-sensitive buyers.

Freights stable as trade activity remains muted

Seaborne freights showed little movement during the week, in line with muted cargo bookings. BigMint assessed Supramax freights from East Kalimantan to Navlakhi at $11.01/dmt, remaining unchanged w-o-w. The stability in freights reflects a balance between adequate vessel availability and limited incremental demand from Indian importers.

Portside coal inventories remain comfortable

India’s portside thermal coal inventories were marginally higher by 0.3% w-o-w at 12.95 mnt in week 1 of 2026 (week ended 2 January) from 12.91 mnt in week 52 of 2025. Trading and evacuation activity remained subdued, largely due to year-end holiday-related disruptions, which curtailed both fresh arrivals and dispatches. Adequate stock availability further reduced urgency for spot purchases.

Power plant stocks ease, though overall levels remain adequate

Coal inventories at Indian power plants declined by 1% to 52.92 mnt as of 7 January 2026 from 53.51 mnt a week earlier, providing around 17 days of consumption cover. While aggregate stock levels remained comfortable at the national level, 16 power plants continue to operate under the critical category. This is largely attributed to logistical bottlenecks and coal quality mismatches, rather than any structural supply constraint.

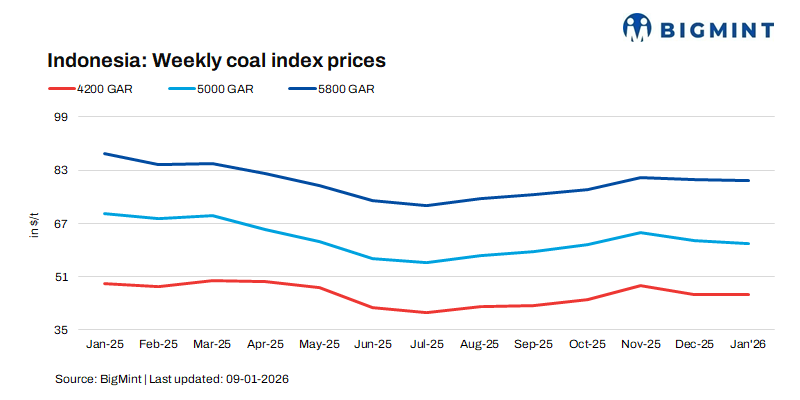

Indonesian benchmark prices edge higher

Indonesian weekly benchmark prices registered a slight uptrend, with 5,800 GAR rising by $0.76/t w-o-w, 4,200 GAR by $0.79/t, and 3,400 GAR by $0.27/t. However, these increases had limited immediate impact on Indian portside prices, as international market sentiment remains cautious and buying appetite subdued.

Outlook

Indian portside prices of Indonesian thermal coal are expected to remain at around current levels next week, supported by comfortable inventories, stable freights, and weak spot demand. Limited buying interest is likely to cap upside despite firmer Indonesian benchmarks, with clearer direction emerging only as post-holiday industrial and power-sector demand improves.

Leave a Reply