- Demand remains subdued, limiting upside potential

- Cost and supply factors offer support, preventing sharp price declines

Indian portside prices of Indonesian thermal coal remained largely stable on a week-on-week basis during the week ended 02 January 2026, as subdued spot buying activity curtailed fresh price discovery across key grades. Market participants largely stayed on the sidelines amid adequate inventories and cautious near-term demand expectations.

According to BigMint’s latest assessments, 5,000 GAR coal was unchanged at INR 7,200/t at Kandla and INR 7,100/t at Vizag. Prices for 4,200 GAR softened marginally by INR 100/t, assessed at INR 5,700/t at Kandla and INR 5,600/t at Vizag, reflecting limited buying interest. Meanwhile, 3,400 GAR coal declined by INR 50/t to INR 4,450/t at Navlakhi, tracking weaker sentiment in lower CV segments.

Lower freight rates cushion landed costs

Freight rates continued to ease during the week, providing some relief to landed costs and lending support to portside prices despite softer international coal benchmarks. BigMint assessed Supramax East Kalimantan-Navlakhi freight at $12.8/dmt, down $0.11/dmt w-o-w. The decline in freight partially offset lower FOB prices, helping prevent sharper corrections in Indian portside valuations.

Portside inventories register net drawdown

India’s portside thermal coal inventories declined by 3% w-o-w to 12.91 mnt in week 52, compared with 13.31 mnt in week 51. Unlike the previous week’s rotation-heavy pattern, the latest data indicates a net stock drawdown, driven by faster evacuation at several major ports and limited fresh arrivals amid the year-end slowdown. Although a few ports reported marginal stock builds, these were insufficient to offset the broader decline across both coasts.

Power plant stocks ease, though overall levels remain adequate

Coal inventories at Indian power plants fell to 53.51 mnt as of 31 December, from 54.67 mnt a week earlier, translating to approximately 17 days of consumption cover. While aggregate stock levels remain comfortable, 15 power plants continue to operate under the critical category. This situation is primarily attributed to logistical constraints and coal quality mismatches rather than an outright supply shortage.

Indonesia revises benchmark prices upward

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) revised its thermal coal benchmark prices (HBA) for the first half of January 2026, signalling a firmer trend across all calorific value segments. The upward revision reflects improving regional demand – particularly from Asian buyers – alongside disciplined supply behaviour by Indonesian miners.

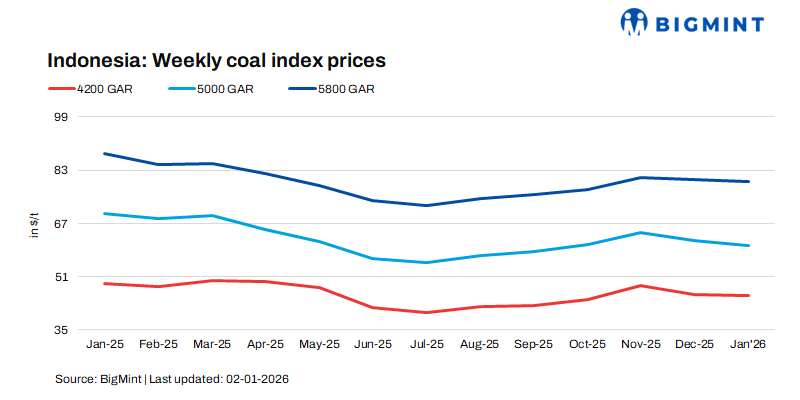

Indonesian weekly index prices edged up marginally, with 5,800 GAR rising by $0.28/t, 4,200 GAR by $0.46/t, and 3,400 GAR by $0.24/t. Despite these increases, broader international market sentiment remains cautious.

Outlook

Indian portside prices of Indonesian thermal coal are expected to stay range-bound in the near term. While weak spot demand and adequate inventories may cap gains, lower freight rates, declining port stocks, and firmer Indonesian benchmarks should support prices. Direction will hinge on restocking activity and power sector demand.

Leave a Reply