- Domestic output declines further

- Imports continue bridging gap

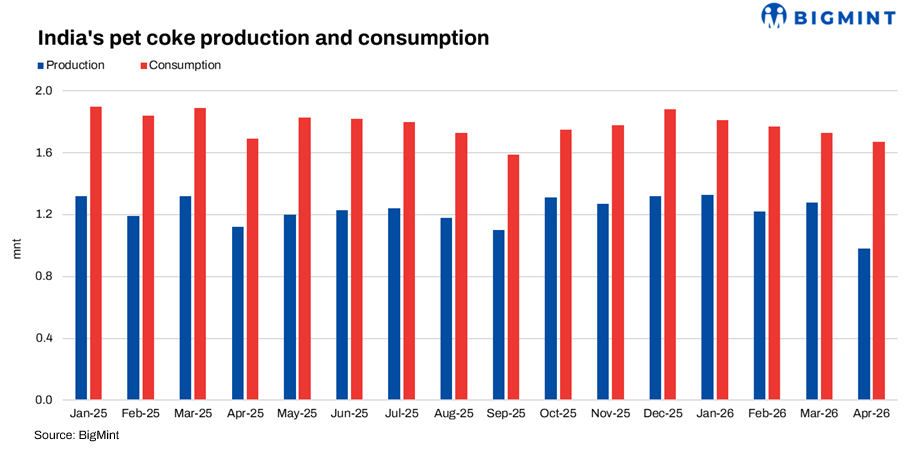

India’s petcoke market presented a mixed picture in April 2026, with consumption recovering while domestic production remained under pressure. Petcoke consumption increased to 1.67 mnt from 1.56 mnt in April 2025, registering a 7% y-o-y rise, indicating gradual normalisation in fuel usage after the disruptions witnessed in recent months. However, domestic production declined to 0.98 mnt from 1.12 mnt a year ago, reflecting continued constraints in refinery operations and crude sourcing dynamics.

Consumption improves while production remains weak

Petcoke consumption recovered during April as industrial activity gradually normalised and demand from key end-users improved. Consumption represented around 8.57% of total petroleum product consumption of 19.47 mnt during the month, compared with 7.72% in April 2025, when petcoke consumption stood at 1.56 mnt against overall petroleum product consumption of 20.28 mnt.

Despite the monthly improvement, the broader trend remained subdued. Total petcoke consumption during FY 2025-26 stood at 19.85 mnt, down 10% from 22.06 mnt recorded in FY 2024-25. Average monthly consumption declined to around 1.65 mnt, compared with 1.83 mnt in the previous fiscal year.

Market participants stated that cement producers, the largest consumers of petcoke, continued optimising their fuel mix depending on economics. Higher imported petcoke prices in recent months encouraged greater use of domestic and imported coal, particularly US NAPP coal, as an alternative fuel. However, the recent correction in imported petcoke prices and easing geopolitical concerns supported a gradual improvement in consumption.

DGFT regulations also continued influencing consumption patterns. Imports of raw petcoke (RPC) and calcined petcoke (CPC) remained regulated for specific industries, while cement sector imports continued without quantity restrictions, making the sector the largest contributor to overall petcoke demand.

Domestic output falls, import dependence persists

Domestic petcoke production remained weak during April. Output declined by 12.9% y-o-y to 0.98 mnt from 1.12 mnt in April 2025.

During FY 2025-26, total domestic petcoke production stood at 14.77 mnt, marginally lower than 14.96 mnt in FY 2024-25, indicating a 1.3% decline. Petcoke accounted for around 5.2% of total petroleum product output of 284.88 mnt, compared with 5.27% in the previous fiscal year.

As a refinery by-product generated through delayed coking units (DCUs), petcoke production continued to depend largely on refinery product-mix decisions rather than direct demand. Production priorities remained linked to transportation fuels such as diesel, petrol and ATF, which offer higher margins.

The widening gap between domestic output and demand reinforced India’s dependence on imports. Domestic production met only around 58.7% of April’s consumption, with the balance supplied through imports. On an annual basis, domestic production covered approximately 74.4% of FY 2025-26 consumption, improving from 67.8% in FY 2024-25.

Market participants noted that geopolitical tensions surrounding crude trade routes and elevated freight costs had affected refinery operations over recent months. However, easing international volatility and improved crude availability may help stabilise domestic production going forward.

Outlook

India’s petcoke market is expected to remain balanced in the near term. Consumption may continue recovering as industrial activity improves, although cement producers are likely to maintain flexible fuel strategies based on coal and petcoke economics. Meanwhile, domestic production is expected to remain dependent on refinery operating decisions and crude market developments, ensuring that imports continue to play an important role in meeting the country’s petcoke requirements.

Leave a Reply