- Dec sees selective, fragmented import recovery

- High prices limit aggressive restocking

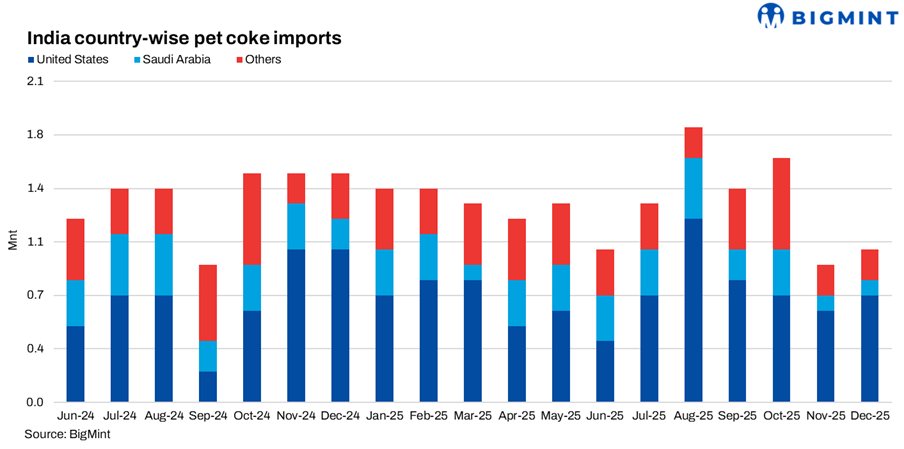

India’s pet coke imports declined sharply to 3.5 mnt in Q3 from 4.5 mnt in Q2, registering a 22% q-o-q contraction, as industrial consumers significantly reduced overseas procurement. The decline was driven by firm global pet coke prices, higher landed costs, and growing substitution toward domestic coal and imported thermal coal, particularly South African material, which offered better cost parity during the quarter.

Despite steady operating rates across cement and industrial segments, buyers displayed lower risk appetite, preferring to draw down existing inventories rather than restock at elevated prices.

US dominance weakens as volumes retreat

The US remained India’s largest pet coke supplier, though shipments fell to 2.1 mnt in Q3 from 2.5 mnt in Q2 (-16%), reflecting pullback by major cement buyers. Saudi Arabian supplies saw a steep 38% decline, falling to 0.5 mnt from 0.8 mnt, while Venezuelan cargoes dropped sharply to 0.1 mnt from 0.4 mnt (-75%), underscoring broad-based import contraction rather than origin-specific disruption.

Oman’s exports held steady at 0.3 mnt, while smaller suppliers such as Mexico, Canada, Kuwait and Brazil together contributed marginal volumes. Overall, India’s sourcing basket became narrower and more conservative, with buyers prioritising logistical certainty and contractual flexibility.

Cement majors cut intake after earlier restocking

On the demand side, UltraTech Cement reduced pet coke imports to 0.9 mnt in Q3 from 1.0 mnt in Q2 (-10%), reflecting sufficient coverage from earlier purchases. Shree Cement cut intake more sharply to 0.3 mnt from 0.4 mnt (-25%), while Reliance Industries maintained steady buying at 0.3 mnt, largely linked to refinery and captive consumption needs.

Mid-sized cement and industrial players such as Rain CII, JK Cement, Wonder Cement and Ambuja Cement maintained relatively stable but low-volume procurement, signalling a shift toward need-based buying rather than strategic stocking.

Dec imports edge up m-o-m but recovery fragile

On a monthly basis, pet coke imports rose marginally to 1.0 mnt in December 2025, up from 0.9 mnt in November (+11% m-o-m). The increase reflected selective buying rather than a broad demand revival.

US-origin shipments increased to 0.7 mnt from 0.6 mnt (+17%), while Saudi supplies remained unchanged at 0.1 mnt. Oman shipments dropped to zero from 0.1 mnt, highlighting continued volatility in monthly sourcing patterns.

Import economics remains key constraint

Import economics remained the key constraint. High pet coke offers kept landed costs elevated, prompting several cement producers to favour South African thermal coal over imported pet coke, particularly in eastern and southern India. Domestic coal availability further reduced reliance on imports, allowing buyers to optimise fuel mixes without sacrificing margins.

Structural caution, not demand collapse

The Q3 decline did not indicate a collapse in end-user demand, but rather a structural adjustment in fuel sourcing strategy. Buyers increasingly balanced pet coke against thermal coal and domestic alternatives, responding to price signals rather than supply shortages.

Outlook

Pet coke imports are expected to remain moderate and range-bound in early 2026. Unless global prices soften materially or freight costs decline further, buyers are likely to continue selective, short-term procurement, with upside capped by competition from alternative fuels.

Leave a Reply