- US largest supplier despite declining shipments

- US Gulf freight surges to $50+/t during peak periods

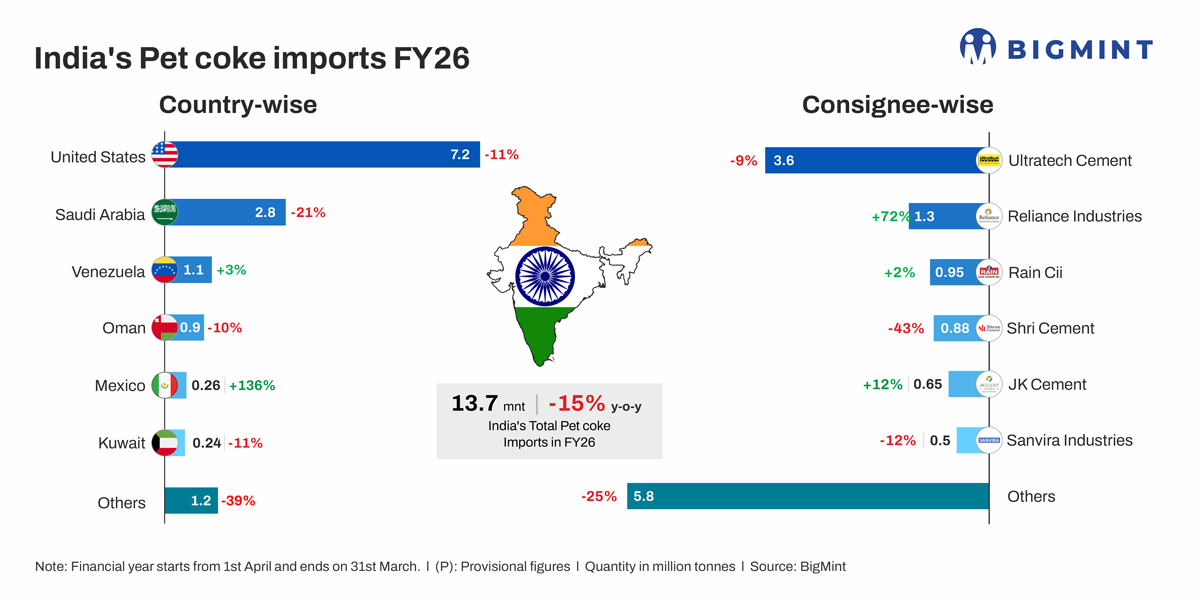

India’s pet coke imports declined 15% y-o-y to 13.7 mnt in FY’26, compared with 16.1 mnt in FY’25, reflecting sustained pressure from elevated global prices, rising freight costs, and increasing substitution by coal.

The decline was not uniform through the year but driven by phased changes in pricing, demand cycles, and procurement strategies, particularly from the cement sector – the largest consumer.

Top exporters

The United States remained the largest supplier despite shipments declining 11% y-o-y to 7.2 mnt from 8.1 mnt. Saudi Arabia imports fell sharply by 21% to 2.8 mnt, while Oman also declined 10% to 0.9 mnt. Venezuela remained largely stable at 1.1 mnt. Notably, Mexico recorded a sharp increase to 0.26 mnt (up 136%), indicating diversification in sourcing. Imports from Kuwait declined 11%, while volumes from other regions dropped significantly by 39%.

Top buyers

Ultratech Cement remained the largest importer at 3.6 mnt, though volumes declined 9% y-o-y. Reliance Industries increased imports sharply by 72% to 1.3 mnt, supported by trading and blending requirements. Rain CII remained stable at 0.95 mnt, while Shri Cement recorded a sharp drop of 43% to 0.88 mnt. JK Cement increased imports by 12%, whereas Sanvira Industries declined by 12%. Imports by other buyers fell 25%, indicating overall cautious procurement.

Price trend: From stability to sharp rally

At the start of FY’26 (April-June), imported pet coke prices in India remained relatively stable in the $100-110/t CFR range, supported by adequate US availability and weak Chinese demand due to trade tensions.

During the monsoon period (June-September), demand weakened further, keeping prices largely range-bound as cement activity slowed. Buyers remained cautious, and procurement was largely need-based.

However, from Q3 onwards (October-December), the market tightened:

- Prices firmed to $118-120/t CFR amid reduced domestic availability and steady post-festive demand

- Freight costs increased, adding cost pressure

- Indian buyers began advance bookings, anticipating further upside

The real shift came in Q4 (January-March):

- Prices surged to $150-165/t CFR in March, from ~$120-125/t earlier

- Driven by geopolitical tensions (US-Iran), higher freight, and supply constraints

- Replacement cost economics pushed the market significantly higher

- Freight, geopolitics and supply disruptions reshape market

A key driver through FY’26 was freight volatility.

- US Gulf freight surged to $50+/t during peak periods

- Middle East tensions increased marine insurance and rerouting costs

- Supply tightened due to refinery disruptions and limited prompt cargo availability

These factors pushed landed costs sharply higher, even when FOB prices remained relatively stable.

Coal emerges as strong competitor

One of the most defining trends of FY’26 was the growing competition from coal.

- High-CV coal (especially US NAPP) was often $10-15/t cheaper than pet coke

- Cement plants increasingly: Shifted to coal blends, optimised fuel mix, reduced reliance on imported pet coke

This shift became more visible in Q4, when pet coke prices surged sharply.

Cement sector strategy limits import demand

The cement industry played a crucial role in shaping import trends. Early in the year, many players secured cargoes at lower prices (mid-2025). This advance stocking reduced spot demand later

During price rallies, buyers relied on inventories, delayed purchases, shifted to coal

By February-March: Procurement became highly price-sensitive. Imports dropped sharply, reflecting inventory drawdown and cost control

Market structure: Seller strength vs buyer resistance

By the end of FY’26, the market evolved into a two-sided structure:

Sellers: Holding firm offers due to tight supply, supported by freight and geopolitical factors

Buyers: Price-sensitive and cautious, shifting to coal and managing inventories

This resulted in: Wide bid-offer gaps, limited spot deals and a replacement-cost-driven market

Outlook

Imports are expected to remain volatile but constrained in the near term. If supply tightness persists, prices may stay firm

However, coal competitiveness and cautious buying will limit upside Cement sector fuel flexibility will remain a key factor. Overall, FY’26 reflects a transition phase — where the pet coke market moved from demand-driven to cost-driven and strategy-driven procurement behaviour.

Leave a Reply