- Raipur-based producer hikes offers by INR 200/t today

- NMDC raises iron ore prices by INR 100/t for Feb delivery

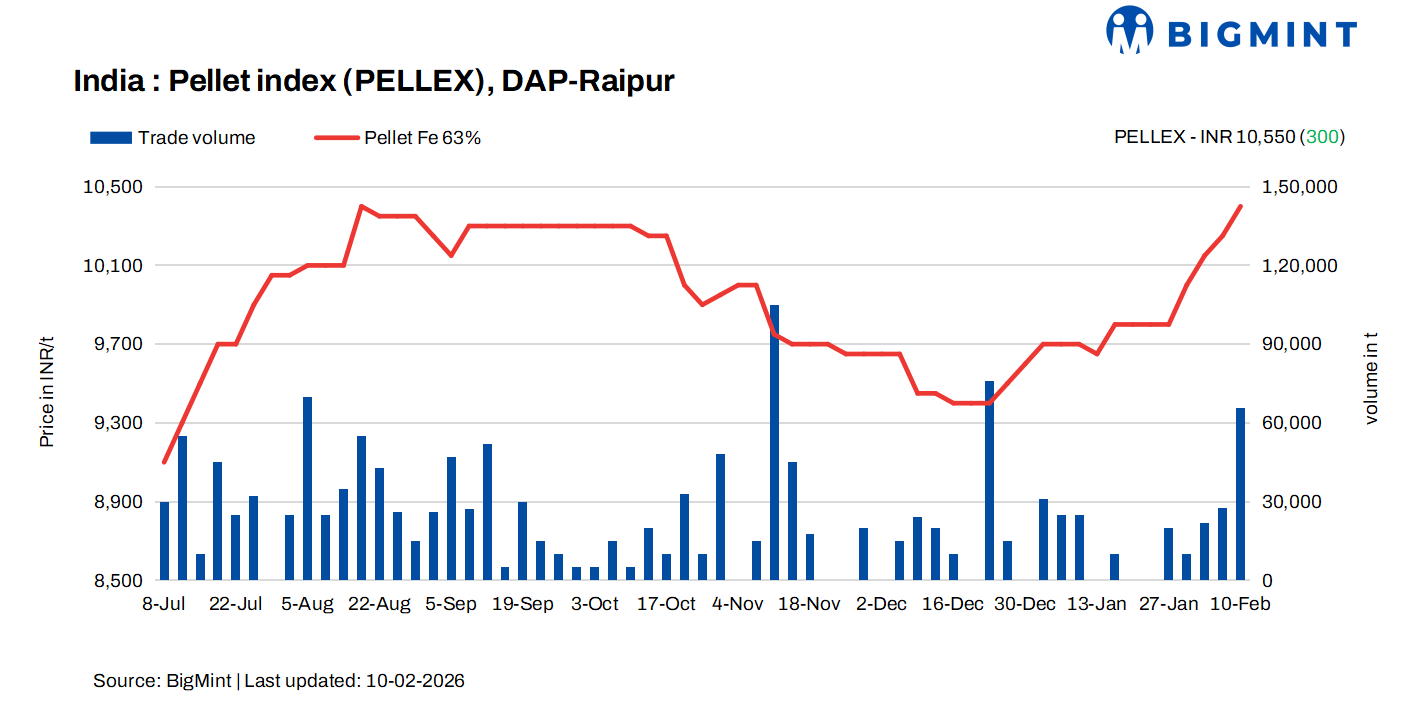

Pellet prices in the Raipur hub increased by INR 200-300/t, as assessed on 10 February, following a hike in fresh offers announced by local producers. With the latest revision, prices in the region have reached their highest level in nearly 16 months compared with around INR 10,500/t recorded in October 2024.

Trades and price movements

PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, inched up by INR 300/t ($3/t) to INR 10,550/t ($117/t) DAP on 10 February compared to the previous assessment on 6 February. Around 67,500 t of pellet (Fe 62.5-63%) deals were concluded in the market at INR 10,300-10,400/t ($114-115/t) exw Raipur, reflecting active trades during the publishing window.

Raipur-based pellet producers raised offers for Fe 62.5-63% (+/-0.5) grade pellets by INR 200/t ($2/t) to INR 10,400-10,500/t ($115-116/t) exw on 10 February. The recent increase in iron ore prices by NMDC, along with active deals at previous offers and positive sentiment in the semi-finished market, led to the price rise.

Market scenario

Sources said the upward revision was primarily supported by active trades concluded at previous offer levels, along with a sustained rise in sponge iron prices, which encouraged producers to lift their offers. A market participant said, “Trades were comfortably absorbed at earlier prices, which gave sellers the confidence to push offers higher.”

Additionally, rising raw material costs added pressure on pellet prices. Iron ore prices firmed up after NMDC revised its prices for February deliveries, which kept pellet values on the higher side. A producer noted, “The increase in iron ore prices has directly impacted pellet cost structure, leaving little room for price correction.”

However, the buying side remained cautious with offers surging. According to market sources, several buyers had already secured material at previous prices over the past few days, limiting immediate spot demand. A buyer said, “Most sponge iron units are well covered for now, so fresh buying at higher levels is being evaluated carefully.”

However, sellers reported an increase in inquiries over the last few days, supported by continued strength in sponge iron and billet prices. Trading activity during the current publishing window was described as moderate, with buyers actively tracking the market amid strong liquidity in the finished steel segment.

Some participants indicated a wait-and-watch approach, citing iron ore lumps as a potentially more cost-effective alternative at elevated pellet prices. A steelmaker informed, “At current pellet levels, lump ore economics look attractive; so we are temporarily holding off pellet purchases.”

NMDC announced its list prices of iron ore CLO (calibrated lump ore) and fines on 10 February. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 5,250/t ($58/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,000/t ($44/t). Prices are on FOR basis from the miner’s Bacheli complex and exclude royalty, DMF, and NMEDT. Prices of all grades were raised by INR 100/t.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- Six (6) deals were recorded in this publishing window, so this category was taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Fifteen (15) firm offers, bids, and indicative prices were heard. Ten (10) were taken for price calculation and given balance 50% weightage.

Key market drivers

- Sponge iron prices rise w-o-w: Sponge iron prices surged by INR 1,950/t ($22/t) w-o-w on 6 February to INR 27,900/t ($308/t) exw-Raipur. Prices in Raipur rose by INR 300/t d-o-d. Buying interest remained moderate during the day, supported by tight PDRI availability in select markets, which continued to push prices higher. However, acceptance of higher price levels was low, with buyers largely tracking further price direction and preferring to remain on the sidelines. Under the prevailing market conditions and supply tightness, the scope for any correction in prices appears limited at present.

- Billet prices inch up w-o-w: BigMint’s billet index increased by INR 1,250/t ($14/t) w-o-w to INR 42,200/t ($466/t) exw-Raipur. Meanwhile, prices also rose by INR 450/t d-o-d today. Market activity stayed restricted throughout the session, with procurement largely need-based. Most buyers refrained from fresh bookings, preferring to wait for clearer price direction. Mills reported softer enquiries from downstream segments, which weighed on billet offtake. On the supply side, producers attempted to hold offers at higher levels, supported partly by selective bookings concluded in the previous session, though this support proved insufficient to improve overall sentiment.

Outlook

Pellet prices are expected to remain stable at current levels, with some active trades expected to conclude at revised offers in the near term.

Leave a Reply