- Raipur’s offers stay firm amid limited material availability

- Sponge iron, billet tags fall amid soft finished steel demand

Pellet prices in the Raipur region remained largely stable this week as market activity continued to be sluggish amid declining sponge iron and billet tags. Market participants highlighted that the ongoing weakness in the semi-finished steel segment has dampened buying interest among sponge iron and steel producers.

Price movements, trades

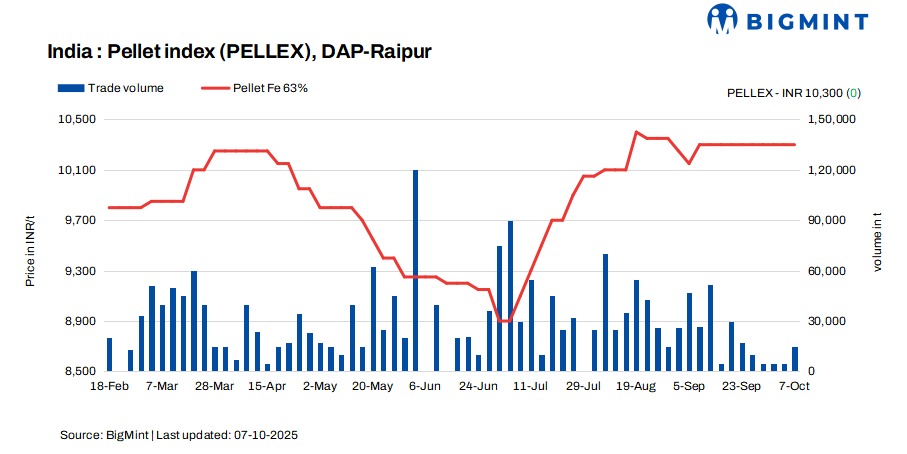

PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable at INR 10,300/t ($116/t) DAP on 7 October 2025 compared to the previous assessment on 3 October. Deals for around 10,000 t of Odisha-origin material were recorded in the Raipur market in the last couple of days. Meanwhile, deals for 5,000 t were concluded by local sellers.

Raipur-based pellet producers kept their offers for Fe 63/63.5% (+/-0.5%) material stable at INR 10,200/t ($115/t) exw. The prices were stable while buying inquiries were limited.

Some Odisha-based suppliers offered pellets at INR 9,700-10,400/t ($109-117/t) DAP Raipur, with a few deals concluded by Raipur-based buyers.

Market scenario

A Raipur-based buyer said, “Current pellet prices are not viable for us, given the continuous fall in sponge iron and billet rates. We are purchasing only on a need basis as margins remain under pressure.”

On the supply side, a few pellet producers have kept their sales closed due to ongoing maintenance shutdowns and pending dispatches from previous bookings. This limited supply prevent any sharp correction in local prices despite muted demand. Market participants noted that the recent maintenance shutdown of a prominent Raipur-based supplier has indirectly supported prices, as other sellers are holding their offers firm despite the weakened market sentiment.

A trader noted, “Some suppliers are keeping their offers in place to protect their profit margins, even though demand remains weak. However, once new supply enters the market, we may experience increased selling pressure. Additionally, we have learned that another plant has been commissioned with a capacity of 0.8 MTPA.”

Meanwhile, a few buyers were reportedly able to secure material from Odisha-based suppliers at more competitive prices, taking advantage of the widened price gap between Odisha and Raipur offers. This cross-regional buying is expected to increase if Raipur’s prices remain firm.

Additionally, many buyers are awaiting the announcement of NMDC’s iron ore price revision for October deliveries, which could influence pellet pricing trends.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- One (2) deal was reported in this publishing window; one was taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Twenty-five (25) firm offers, bids, and indicative prices were heard. Twenty-three (23) were taken for price calculation and given a balance of 50% weightage.

Key market drivers

- Sponge iron tags down w-o-w: P-DRI prices declined by INR 750/t ($8/t) w-o-w to INR 23,350/t ($263/t) exw-Raipur on 7 October while falling by INR 250/t ($2.5/t) d-o-d. The bearish trend was intensified by sluggish movement in the semi-finished and finished steel segments, contributing to the overall cautious market tone.

- Billet prices drop w-o-w: Billet prices in Raipur decreased by INR 650/t ($7/t) w-o-w to INR 35,500/t ($400/t) exw today. Prices fell by INR 300/t ($3.5/t) d-o-d. Weak cues from the neighbouring regions and persistent softness in finished steel demand weighed on spot offers. While a few modest bookings were concluded at lower levels, overall market activity remained need-based. Slight d-o-d volatility offered temporary support, but the broader downward trend continued.

Outlook

Pellet prices are expected to remain volatile in the coming days, with mixed sentiments prevailing in the Raipur pellet market.

Leave a Reply