- Ample supply in China, falling futures pressure sentiment

- Ukrainian supply disruptions may benefit Indian exporters

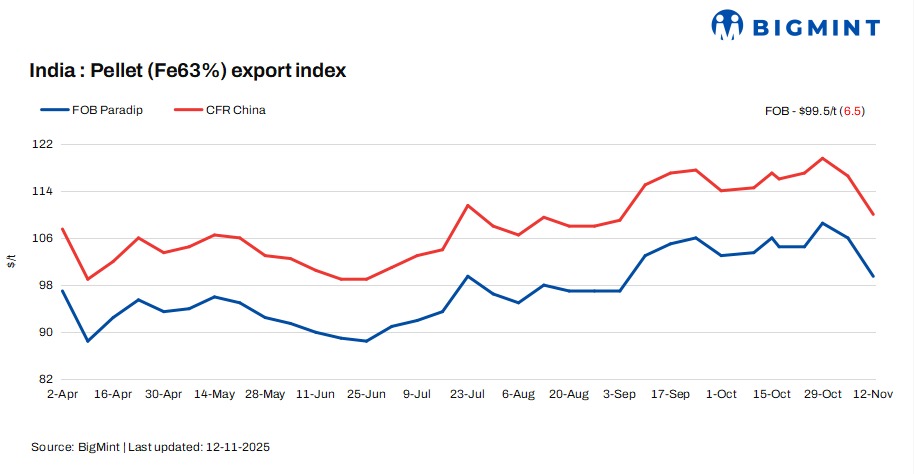

Indian pellet export prices declined this week, as market sentiment turned weak due to sluggish demand from Chinese buyers and a broader downturn in global iron ore tags. Market participants highlighted that limited trade inquiries and reduced restocking activity from Chinese mills weighed heavily on export offers.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index fell by $6.5/tonne (t) w-o-w to $99.5/t FOB east coast on 12 November against 5 November.

No confirmed export deals were recorded during the week. However, industry sources indicated that one major Indian pellet producer may have sold around 75,000 t of Fe 62% pellets at $115-116/t CFR China, though the transaction has yet to be officially confirmed. Meanwhile, another supplier offering higher-grade pellets struggled to secure deals, with the cargo remaining unsold due to wide bid-offer disparities.

Market movements

An international trader informed BigMint, “Chinese mills have already built sufficient inventories for December and January, leading to weaker fresh demand for imported pellets.” The oversupply in the domestic Chinese market, coupled with falling iron ore futures, pressured sentiment across the seaborne market.

Another international trader pointed out that the recent missile strike on Ferroexpo’s power unit in Ukraine could disrupt the country’s pellet supply to China, adding to global market uncertainty. “If Ukrainian shipments slow down, it may open a short-term opportunity for Indian suppliers, but clarity is still awaited regarding potential demand,” he remarked.

Chinese steelmakers have embraced advanced strategies to navigate the downturn in the market. Instead of shutting down operations completely, these mills are opting for extended maintenance periods and optimising their production rates. This strategic approach enables them to quickly respond to any improvements in market conditions while avoiding the substantial costs linked with fully restarting their facilities.

Consequently, Indian exporters remained cautious. One major supplier said, “We are selling our full production in the domestic market and have no plans for export cargoes at present.”

Overall, market participants expect more clarity on tradable levels over the next couple of weeks.

Domestic vs export market gap increases

Domestic prices exceeded export offers by around INR 1,400/t ($16/t), with the gap increasing by INR 600/t ($7/t) w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,200/t ($93/t) exw, largely stable compared to last weekend. Meanwhile, the ex-plant realisation in exports from Barbil dropped by INR 600/t ($7/t) w-o-w to INR 6,800/t ($77/t) exw.

Rationale

- No (0) confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was allotted zero % weightage for today’s price calculations. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and nine (9) were considered for the calculation of the index and given the balance 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices dip w-o-w: The benchmark iron ore fines index fell $3/t w-o-w to $102/t CFR China on 11 November. Prices softened as mid-grade fines saw limited trades at discounted levels. Port-stock prices fell further on weak buying, as mills stayed cautious and maintained low inventories, opting for need-based purchases. Preference for fines over lumps remained steady, further pressuring the lump market.

- DCE iron ore futures edge down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract closed at RMB 774/t ($109/t) on 12 November, edging down w-o-w.

- Pellet inventories at Chinese ports rise: Pellet inventories at major Chinese ports stood at 2.45 mnt on 6 November, inching up by 0.15 mnt w-o-w as per data published by SteelHome.

Outlook

Leave a Reply