- Global fines spot, futures prices increase

- Around $5-10/t gap in bid-offers in east coast

The Indian seaborne pellet market remained firm this week, supported by a positive shift in market sentiments, increase in freight rates and a sharp rise in global iron ore fines prices. The upbeat momentum, which has been building over the past two weeks, is now reflected in expectations for export pricing, particularly for August deliveries.

Price update

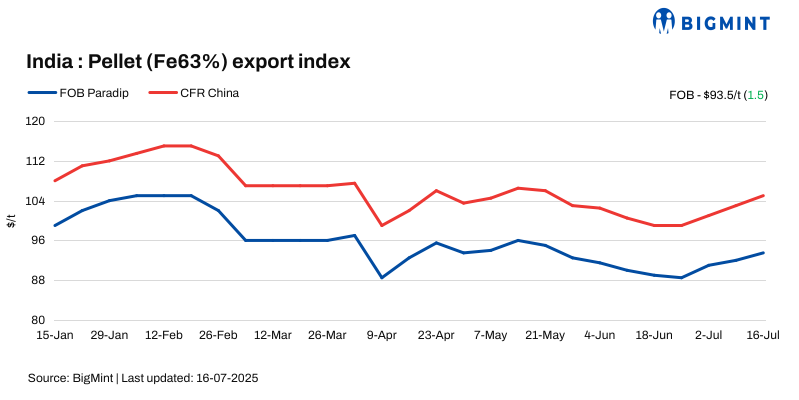

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index (FOB east coast) rose by $1.5/t w-o-w to $93.5/t on 16 July 2025 against 9 July. Notably, no pellet export deal was reported from India’s eastern coast this week. However, following the improving trend of seaborne prices, markets are optimistic about the pellet export deals.

Rising supramax vessel freight on the India-China route lifted CNF prices by $2/t w-o-w but limited the total hike in FOB values to $1.5/t.

An Odisha-based producer quoted, “We are receiving some inquiries and interest in purchasing the pellet; however, there is still a significant gap of $5-10/t between the bids and offers.”

Market comments

According to market sources, swaps for August shipments are hovering above the $100/t CFR China mark, which is providing support to Indian-origin pellets. A trader informed, “If the market gains another $5-7/t in the near term, we may see some export deals from the east coast.”

However, the overall demand from China remains selective, with buyers focusing primarily on low-alumina material. Several Indian cargoes reportedly remained unsold at Chinese ports due to unviable prices for steel mills. An international trader mentioned, “High-alumina pellets are finding it difficult to attract buyers at current offers.”

Indian exporters are currently targeting offers around $110-113/t CFR China. In the meantime, some suppliers have shifted focus to the domestic market amid logistical challenges and limited availability of iron ore fines, particularly due to heavy monsoon rainfall in the eastern regions.

A producer based in Odisha commented, “We’re holding back seaborne offers and participating in domestic bulk deals while waiting for tender outcomes. The domestic trade is giving better realisations compared to the export market.”

Domestic vs export market gap

Domestic prices exceeded export offers by around INR 1,650/t ($19/t), with a rise in both domestic and export prices. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 7,750/t ($90/t) exw, rose INR 200/t ($2.5/t) w-o-w. Meanwhile, the ex-plant realisation in exports from Barbil recorded firm at INR 6,100/t ($71/t) exw.

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and ten (10) were considered for the calculation of the index and given 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices up w-o-w: The benchmark iron ore fines index rose $3/t w-o-w at $98/t CFR China on 15 July. Market sentiment improved due to a positive outlook and increased trading activity. Strong demand for mid-grade fines contributed to this optimism. However, liquidity for Jul’25 seaborne cargoes decreased, and bullish expectations for the ferrous market in Aug’25 led to a further widening of the contango.

DCE iron ore futures climb w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract improved by RMB 36.5/t ($5/t) w-o-w to RMB 773/t ($108/t) on 16 July. Meanwhile, prices inched up by RMB 6.5/t ($1/t) d-o-d today.

Outlook

According to BigMint analysis, the pellet export market is expected to remain volatile in the short term. Without a significant upward price movement of at least $5-7/t, fresh export deals from India’s east coast are considered unlikely.

Leave a Reply