- Bid-offers disparity in the seaborne market with a lack of inquiries

- Lower buying interest from Chinese mills keeps export deals muted

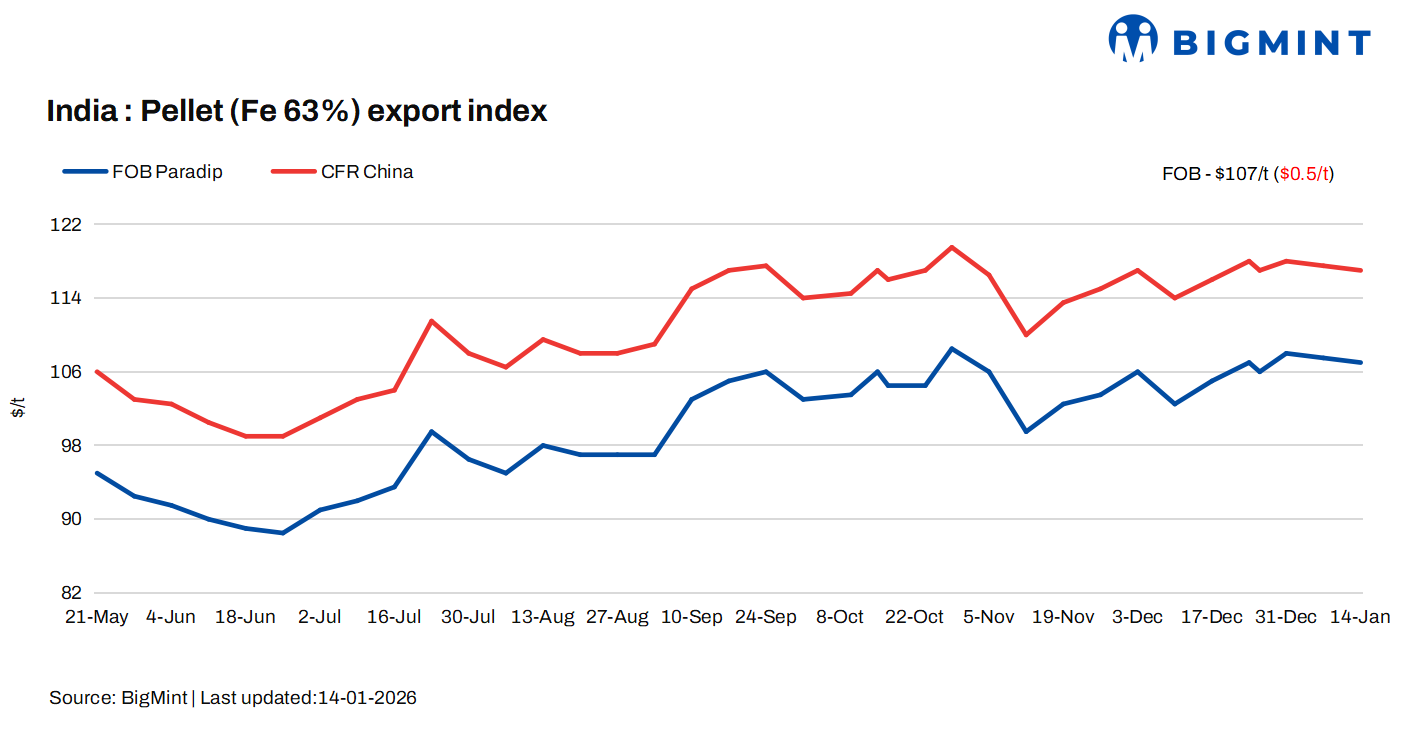

Pellet prices in the seaborne market remained largely rangebound over the past few days on 14 January 2026, though minor price fluctuations were observed amid subdued trading activity. Market sentiment continued to weaken in the Indian seaborne market, primarily due to elevated iron ore and pellet inventories at Chinese ports, which have restrained fresh buying interest from end-users.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index remained largely stable w-o-w at $107/t FOB east coast on Wednesday.

The suppliers are actively offering their pellet cargo for Fe 63-64% material, but due to limited inquiries and lower buying interest, the transactions have remained away from the market.

Market movement

Market participants noted that steel mills in China are prioritising cost efficiency, leading to cautious procurement strategies and limited spot inquiries. An international trader said, “With port stocks remaining high, buyers are not in a hurry to book cargoes, especially at current premium levels.”

Indian suppliers confirmed that pellet cargoes are being offered actively for export; however, buying interest remains muted, resulting in a noticeable bid-offer gap. “We are offering material, but counters from buyers are very limited, which is keeping the market inactive,” an Indian exporter commented.

According to market sources, the current workable price level is assessed at around $6-7/t premium over the global iron ore benchmark for 63% Fe pellet cargoes. However, achieving this premium has proven challenging under prevailing market conditions.

An international trader highlighted that Indian suppliers are currently asking $119-120/t CFR China, but no deals have been concluded at these levels so far.

Despite the near-term sluggishness, some participants expect demand to resurface post the Chinese holiday period. “A few deals could materialise for post-holiday laycan as mills may return to the market once clarity improves,” a market participant said.

Meanwhile, domestic market dynamics continue to influence export viability. Sources indicated that domestic pellet offers remain attractive, limiting export volumes. As a result, only port-based plants or higher-Fe pellet cargoes are considered economically viable for exports at present.

Domestic vs export market

Domestic prices exceeded export offers by around INR 300/t ($3/t), with the gap narrowing by INR 200/t w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,250/t ($91/t) exw, falling by INR 200/t ($2/t) last weekend. Meanwhile, the ex-plant realisation in exports from Barbil remained stable w-o-w at INR 7,950/t ($88/t) exw.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade. Thus, this category was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and seven (7) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices firm: The benchmark iron ore fines index was assessed at $108/t CFR China on 13 January. Trading was subdued, with activity limited to medium-grade fines. Restocking ahead of the Chinese New Year lent some support to prices, but rising input costs weighed on mill margins. As a result, most mills are on cautious stance, taking a wait-and-watch approach at current levels.

- DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 821/t ($118/t) on 14 January, dropping by RMB 7/t ($1/t) w-o-w.

Pellet inventories at major Chinese ports stood at 3.5 mnt on 8 January, increasing by 0.1 mnt w-o-w, as per data published by SteelHome. With this, port inventories have reached a three-month high reaching levels last seen in mid-September last year.

Outlook

Leave a Reply