- Firm iron ore market supports pellet export prices

- Only two sellers currently offering for exports

The Indian pellet export market remained rangebound this week weighed down by subdued buying interest from the seaborne market and weak sentiment in major regions. Despite suppliers actively offering pellets in the export market, buyers’ response remained muted.

Price update

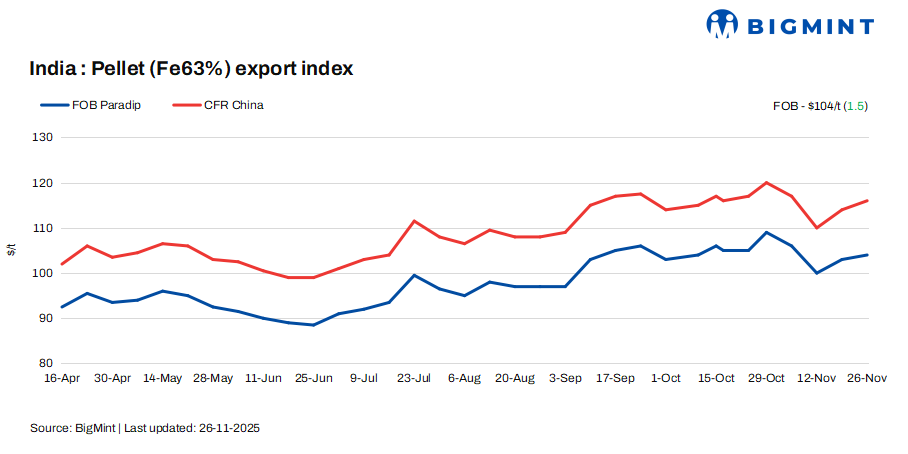

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index up by $1.5/tonne (t) w-o-w to $104/t FOB east coast on 26 November against 19 November.

No export deal was recorded in this publishing window amid weakened market sentiments. An export tender was heard recently, but did not fetch a firm response from buyers.

Market movements

Market participants noted that Chinese buyers are currently showing limited interest in pellet cargoes. An international trader commented, “Pellets are simply not the first choice for Chinese mills right now. Cheaper iron ore and cost-effective raw material blends are making pellet imports less attractive for mills trying to optimise margins.”

This shift in procurement behaviour has further dampened the market mood. No firm bids were received during the week, as the current offer levels quoted by Indian suppliers did not align with buyer expectations. Another source informed, “There is a clear gap between what suppliers are asking and what buyers are willing to pay. Until this narrows, we don’t expect much movement.”

On the supply side, most major pellet producers continue to prioritise the domestic market, driven by comparatively better realisations and existing supply commitments. Only a couple of suppliers were active in the export market, offering cargoes for near-term shipments, but with limited success so far.

A pellet supplier noted the absence of export deals in the sea market, while major producers are currently focused on domestic sales due to better prices and increased iron ore costs for sourcing raw materials.

Given the persistent demand weakness and market uncertainty, traders expect the export market to remain dull in the near term. However, some sources anticipate that a few shipment-based deals could still be concluded if suppliers adjust their offers to align with the current global pricing environment.

Domestic vs export market gap increases

Domestic prices exceeded export offers by around INR 1,200/t ($14/t), remaining stable w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,350/t ($95/t) exw, firm compared to last weekend. Meanwhile, the ex-plant realisation in exports from Barbil rose by INR 100/t ($1/t) w-o-w to INR 7,150/t ($81/t) exw.

Rationale

- No (0) confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was allotted zero % weightage for today’s price calculations. Click here for the detailed methodology.

- Ten (10) indicative prices were received, and eight (8) were considered for the calculation of the index and given the balance 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices rise w-o-w: The benchmark iron ore fines index rose $2/t w-o-w to $107/t CFR China on 25 November. The seaborne market saw active trading, with major miners offering cargoes and firmer buying interest for January shipments. Enquiries for January laycan cargoes increased, supported by improved sentiment on expectations of a US Fed rate cut, though unchanged fundamentals continue to limit overall buying.

- DCE iron ore futures up w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract closed at RMB 797/t ($112/t) on 26 November, edging up by RMB 5.5/t ($1/t) w-o-w.

Pellet inventories at major Chinese ports stood at 2.6 mnt on 20 November, inching down by 0.1 mnt w-o-w as per data published by SteelHome.

Outlook

Leave a Reply