- Pellet prices rise on firm global iron ore, recent deals from India

- Bid-offer gaps limit export trade, producers focus on domestic deals

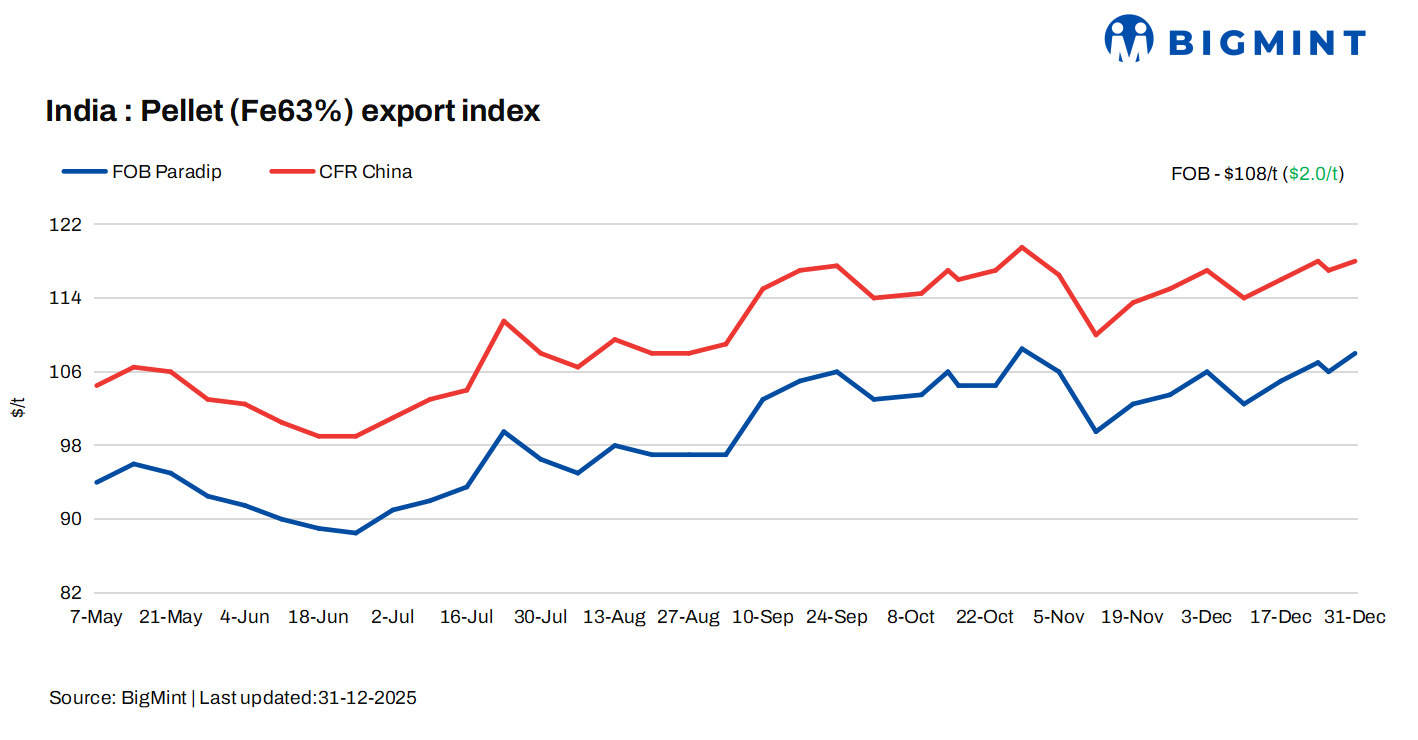

Indian pellet export prices rebounded by a modest $2-3/tonne (t) this week on 31 December, supported by firm global iron ore prices and a few deals concluded from the east coast. However, overall market activity remained subdued, as most transactions were finalised in the previous week, with no fresh inquiries heard during the current week due to the New Year holiday.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index increased by $2/t w-o-w to $108/t FOB east coast on Wednesday. Pellet export prices recovered due to deals concluded by an east coast-based seller over the last weekend. Additionally, a pellet producer recently sold around 75,000 t of 62% Fe pellets at $114-115/t CFR China a couple of days ago.

Meanwhile, another seller is offering high-grade, low-alumina pellets in the export market, but the response from buyers was poor due to a bid-offer disparity.

Market movements

The pellet export market remained largely silent during the week, impacted by the New Year holidays and the absence of fresh buying interest.

Market participants noted that sentiment continues to be subdued due to weak buying interest from China. According to trade sources, a significant volume of Indian pellet cargoes remains unsold at Chinese ports, primarily due to cost-effectiveness concerns among Chinese steel mills.

A market participant said, “Chinese mills are currently focusing on optimizing costs, which has resulted in lower bids to offers from the Indian east coast.”

An international trader highlighted that the Chinese market will remain closed during 1-4 January 2026 due to New Year holidays and is expected to reopen on 5 January, which has further limited market participation. He added, “Most buyers are in wait-and-watch mode until Chinese markets resume operations.”

Meanwhile, exporters pointed to a clear disparity between bids and offers. An exporter said, “Suppliers are seeking a $4-5/t premium over the Fe 65% global fines index for higher-grade low-alumina pellets, but buyers are not comfortable matching these levels at present.” As a result, negotiations have been limited.

Supply-side activity has also been restricted. A pellet producer stated, “Only 2-3 Indian pellet manufacturers are currently active in the export market, while others are prioritizing domestic commitments amid relatively stable local demand.”

Domestic vs export market gap remains stable w-o-w

Domestic prices exceeded export offers by around INR 650/t ($7/t), with the gap remaining unchanged w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,300/t ($93/t) exw, rising by INR 150/t ($2/t) last weekend. Meanwhile, the ex-plant realization in exports from Barbil rose by INR 175/t ($2/t) w-o-w to INR 7,775/t ($80/t) exw.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade. Thus, this category was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Ten (10) indicative prices were received, and seven (7) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices firm up w-o-w: The benchmark iron ore fines index inched up by $1/t w-o-w to $109/t CFR China on 30 December. Prices were supported by improved market sentiment, fresh medium-grade fines trades, policy optimism, and limited mill restarts after maintenance. However, weak fundamentals suggest the uptick may be short-lived, with port prices likely to face near-term pressure.

- DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract closed at RMB 789.5/t ($108/t) on 31 December, rising by RMB 20/t ($2/t) w-o-w.

Pellet inventories at major Chinese ports stood at 3 mnt on 31 December, increasing by 0.1 mnt w-o-w, as per data published by SteelHome. With this, port inventories reached a three-month high, last seen in mid September 2025.

Outlook

Leave a Reply