- Domestic price realization higher by INR 2,000/t

- Suppliers focus on pellet sales in domestic market

Pellet export prices have softened by $1-2/t in the seaborne market following the recent Chinese Politburo meeting, with market sentiments remaining subdued. Export demand for Indian pellets remains weak, primarily as overseas buyers are now focusing on procuring low-alumina pellets to optimize their cost structures.

Price update

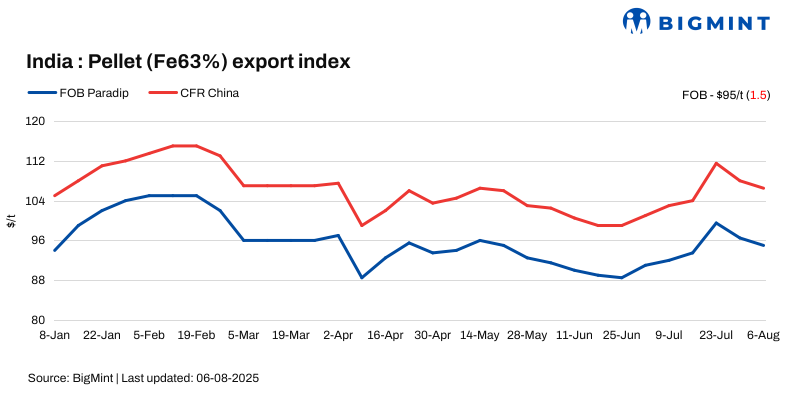

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index (FOB east coast) fell by $1.5/tonne (t) w-o-w to $95/t on 6 August 2025 against 30 July. Notably, no confirmed pellet export deal was reported from India’s eastern coast this week.

Market comments

Indian pellet suppliers are currently shifting focus toward the domestic market, where pricing and demand conditions are comparatively stronger. The domestic market is witnessing healthy buying interest, with bulk orders being concluded, making export offers less attractive for suppliers facing high pellet production costs.

A trader noted, “There is a clear mismatch between the desired export price and the actual market sentiment. With the current CFR target of $115/t, it is difficult to strike deals as global buyers are cautious. The suppliers are getting $8-10/t disparity in bid-offers.”

Adding to the complexity, several exporters are not offering in the export market altogether due to raw material shortages caused by heavy monsoon rainfall in the eastern coastal region. This has disrupted iron ore production and logistics, pushing domestic iron ore prices higher and impacting pellet production margins.

A market participant commented, “We’re focusing on fulfilling domestic orders as margins are better, and the supply challenges make it risky to commit to export deals.”

Meanwhile, the Chinese pellet market remains rangebound post-politburo, with no significant improvement in demand or pricing outlook, further dampening export prospects for Indian sellers. Until there is a shift in Chinese sentiment or domestic supply eases, Indian exporters are likely to stay on the sidelines in the seaborne market.

Domestic vs export gap widens

Domestic prices exceeded export offers by around INR 2,000/t ($23/t), widening by INR 200/t with stable domestic and a fall in export prices. Pellet (Fe 63%) prices in Odisha’s Barbil were recorded at INR 8,250/t ($94/t) exw, unchanged w-o-w. Meanwhile, the ex-plant realisation in exports from Barbil was lower INR 200/t ($2.5/t) w-o-w to INR 6,250/t ($71/t) exw.

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Thirteen (13) indicative prices were received, and twelve (12) were considered for the calculation of the index and given 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices stable w-o-w: The benchmark iron ore fines index remained stable w-o-w at $102/t CFR China on 5 August. Prices were firm due to sustained downstream activity and the upcoming holiday. The iron ore market remained resilient with firm demand for Sept’25 cargoes, as restocking efforts boosted the outlook. Chinese port stock prices increased despite low buying interest.

DCE iron ore futures firm w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract remained supportive w-o-w at RMB 794.5/t ($111/t) on 6 August.

Outlook

According to BigMint’s analysis, the recent bid-offer disparity is likely to remain in the market due to the still large gap in prices, which may keep exporters away from the sea market.

Leave a Reply