- Better domestic realizations, bid-offer gaps keep sellers away

- Trade may pick up in 2nd half of Apr’26, export tenders expected

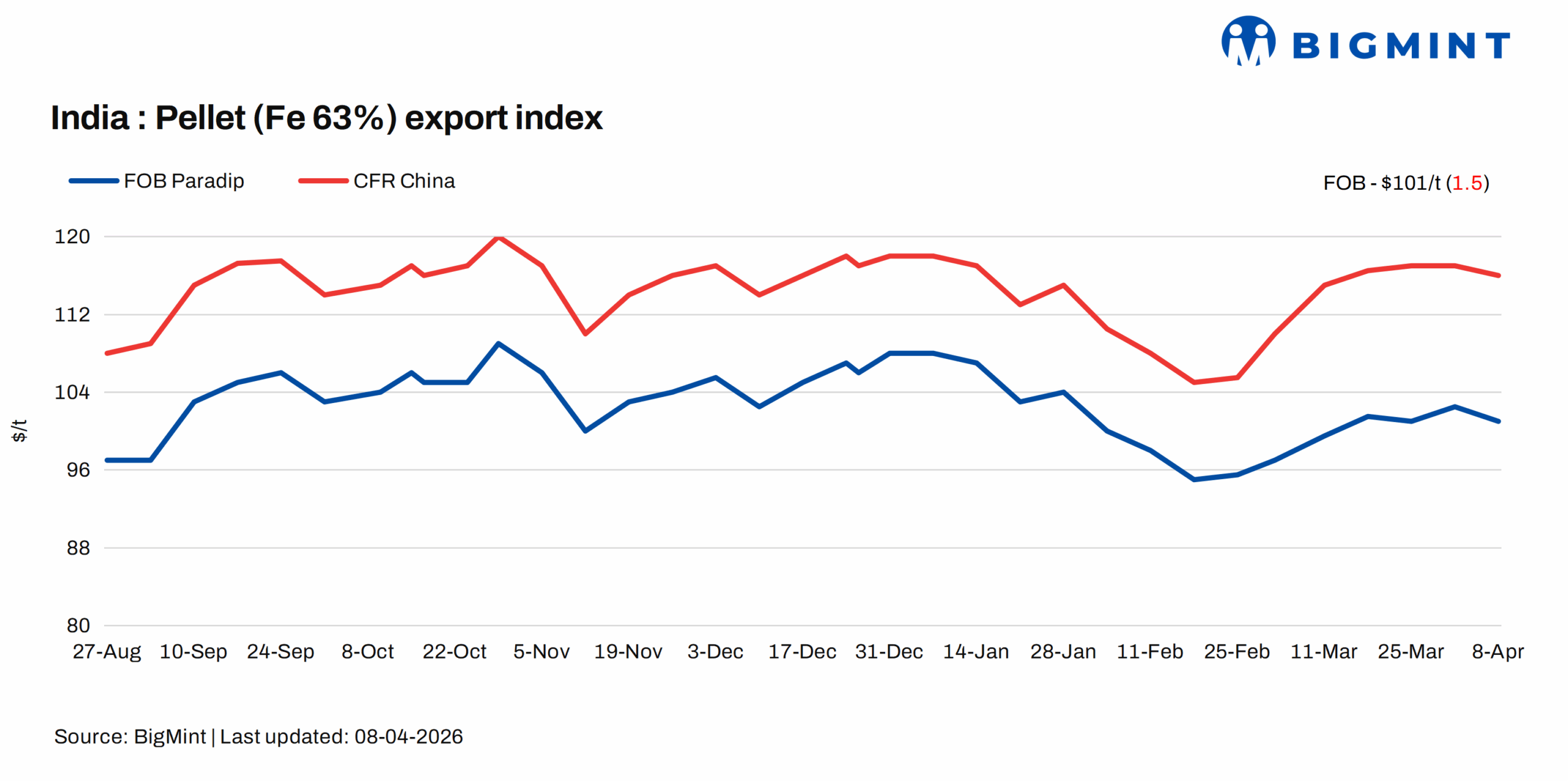

Pellet export prices in the seaborne market remained largely stable w-o-w on 8 April (Wednesday), with limited activity observed as only a few offers were floated by Indian exporters. Market sentiment was cautious amid pricing mismatches and better domestic realizations.

Prices and trades update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index edged down by around $1.5/t w-o-w to $101/t FOB east coast on 8 April against last week. No export deals were concluded from the east coast in this publishing window, with most buyers staying away from bidding.

According to sources, a central India-based supplier recently concluded a pellet export deal at around $135/t CFR China for Fe 64% grade material. Meanwhile, an east coast-based producer floated a tender for Fe 62.5% grade pellets, though the outcome of the tender is still awaited. Despite these developments, overall export activity has remained subdued.

Market updates

Market participants highlighted that while demand from China continued to be stable, Indian exporters were not aggressively participating in the export market. An international trader said, “Demand is there, but suppliers are limited. Export prices are not aligning with producer expectations, especially when domestic markets are offering better realizations.”

A pellet producer noted that a significant bid-offer gap persisted in the export market. He added, “Only port-based plants are currently in a position to match export parity due to their logistical advantage. For inland plants, export deals are leading to negative realizations, making domestic sales a more viable option.”

International traders echoed similar sentiments, stating that Chinese buyers showed a preference for higher-grade, low-alumina pellets but at slightly lower premiums. “This pricing expectation is not workable for Indian exporters at present levels,” another international trader said.

Additionally, several Indian suppliers prioritized domestic commitments and dispatches, further limiting export availability. However, market participants expect some pickup in activity later this month. A south Indian pellet exporter stated, “We may see a couple of export tenders in the second half of April.”

Freight rates were also a key concern, with elevated vessel costs putting pressure on FOB realizations. However, there is cautious optimism that freight rates may ease in the near term, supported by potential softening in fuel prices amid easing geopolitical tensions. This may boost trading momentum as the month progresses.

Domestic vs export market

Export realizations (Fe 63%) decreased to INR 7,200/t on 8 April, reflecting a w-o-w fall of INR 200/t. In contrast, domestic realizations (Fe 62.5%) held firm at INR 8,900/t exw. As a result, the spread between domestic and export prices stood at INR 1,700/t ($19/t), widening by INR 250/t w-o-w.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade, and, therefore, this category was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Eleven (11) indicative prices were received, and eight (8) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices remain stable w-o-w: The benchmark iron ore fines Fe 61% index remained stable w-o-w at $108/dmt CFR China on 7 April. Trading picked up after the holidays, helped by improved landing margins, with steady enquiries for blended ore. However, high port inventories kept prices from rising further. With steel production gradually increasing, trading is likely to gain momentum, though mills will focus on cost-efficient buying.

DCE iron ore futures prices drop: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 792/t ($119/t) on 8 April, falling by RMB 23.5/t ($3/t) w-o-w.

Vessel freights inch up w-o-w: Iron ore freights inched up by $0.2/dmt w-o-w to $15/dmt on 7 April 2026 despite limited fixture activity, with charterers continuing to adopt a cautious, wait-and-watch approach amid uncertain market direction. Ample vessel availability and the absence of strong bidding interest weighed on freights. Overall, the market remained soft, with minimal momentum expected in the near term unless demand shows a meaningful pickup.

Outlook

Pellet export prices are expected to hover at current levels till next week, with any significant movement likely contingent on fresh deal closures and ease in freight dynamics.

Leave a Reply