- Buyers focus on selective high-premium grades

- Participation cautious amid weak coal demand

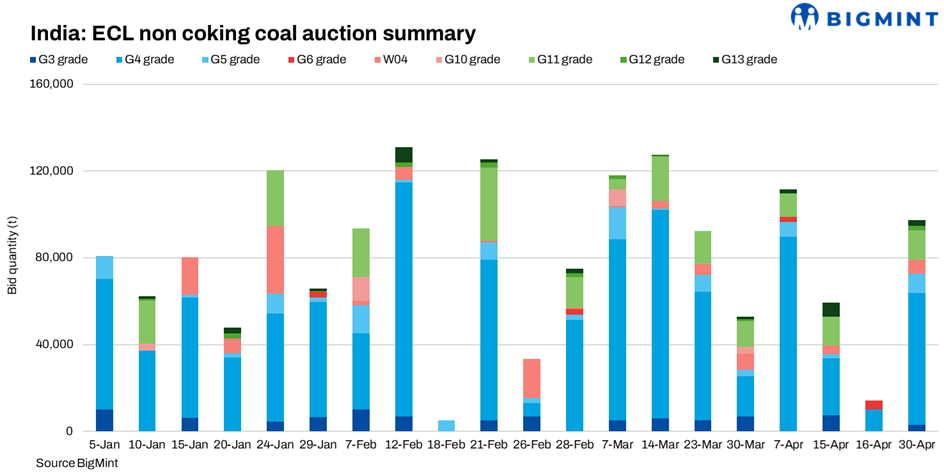

Eastern Coalfields Limited (ECL) conducted multiple non-coking coal auctions during April 2026, with participation trends remaining mixed despite significantly higher offered quantities. ECL offered around 895,250 tonnes (t) on 15 April, 25,000 t on 16 April, and sharply increased offered volumes to 1.41 million tonnes (mnt) on 30 April. However, allocations remained relatively limited compared with availability, reflecting cautious buying sentiment amid weak downstream demand and softer domestic coal prices.

G4 coal dominates auction activity

G4 remained the most actively traded grade across all three auctions, attracting strong interest from sponge iron and industrial consumers. On 15 April, G4 allocations stood at 26,200 t at an average bid price of INR 5,243/t. Premiums strengthened further in the 16 April auction, where G4 achieved INR 6,027/t for 10,000 t allocations despite limited overall participation.

In the 30 April auction, G4 allocations increased sharply to 60,900 t, though average bid prices moderated to INR 4,934/t as larger volumes were offered. Sonepur Bazari OC emerged as the key contributor with 50,000 t allocated at INR 5,926/t, indicating continued strong interest in quality mid-grade coal despite softer broader market conditions.

Higher-grade G3 coal witnessed selective but aggressive bidding. On 30 April, G3 prices surged to INR 6,453/t for 3,000 t from Khas Kajora UG, significantly higher than the notified prices, reflecting limited availability and niche industrial demand.

Meanwhile, lower-grade G11 and G13 coal remained relatively stable, with prices near INR 2,154/t and INR 1,716/t, respectively, across auctions.

Mine-wise trends reflect selective procurement

Mine-level allocation trends showed concentrated buying at select mines rather than broad-based participation. On 15 April, Rajmahal OC and Hura C OC dominated allocations, while premium realisations were recorded at underground mines such as Parbelia UG and Bansra UG.

The 16 April auction saw activity restricted largely to Chinakuri UG Mine and Gopinathpur OC, indicating highly selective procurement behaviour.

In the 30 April auction, Sonepur Bazari OC alone accounted for more than half of the total allocations, highlighting concentrated buying patterns. Other actively allocated mines included Hura C OC, Rajmahal OC, Amkola OC, and Khottadih UG.

Underground mines with limited quantities continued witnessing sharp premiums due to restricted availability and specific industrial suitability.

Bulk buyers drive auction participation

Buyer participation also reflected concentrated procurement by select industrial consumers and traders. On 30 April, Shakambhari Ispat and Power emerged as the largest buyer with 27,500 t of G4 coal at INR 5,867/t. Satyam Iron and Steel and Satyam Smelters also secured sizeable G4 volumes above INR 5,890/t, indicating continued demand from sponge iron producers despite weak finished steel sentiment.

On 15 April, participation was led by traders and smaller industrial buyers such as Godavari Commodities, K.S.K. Agencies, and Khemka Minerals.

The auctions reflected cautious but selective buying interest. While ECL significantly increased offered quantities toward the month-end, buyers largely focused on quality grades and requirement-based procurement rather than aggressive stock building.

Outlook

Auction participation is expected to remain selective in the near term amid adequate domestic coal availability, weak sponge iron margins, and subdued industrial demand. However, premium grades may continue attracting firm bids due to limited supply and operational suitability for sponge iron and industrial consumers.

Increasing offered quantities by coal companies may continue exerting pressure on auction premiums, particularly for lower and mid-grade coal, unless downstream steel and industrial demand improve meaningfully.

Leave a Reply