- Australia rates dip, South African freights surge

- Market activity slows sharply amid GST uncertainty

Dry bulk coal freights showed a mixed trend this week. Indonesia-India rates eased, while Panamax freights on the South Africa-India and Australia-India routes showed strength. Trading activity remained largely subdued, with the Australia-India lane being the only active route, though volatility in rates hinted at downside risks, leading to just a single fixture by an Indian steelmaker.

A source noted, “The Asia-Pacific Panamax market opened the week on a subdued tone, with freights holding flat to slightly softer amid slow trading in the Pacific basin. Freight derivatives also edged lower during Asian hours, while bunker prices stayed largely range-bound.”

Another source told BigMint, “Supramax freights held largely steady to softer, with the trading week opening on a subdued note across regions.”

Trades from South Africa and Indonesia remained subdued as uncertainty over the GST roll-out limited buying activity. At the same time, restrained industrial demand kept overall coal consumption at moderate levels.

India’s portside thermal coal inventories inched up 0.4% w-o-w to 11.93 million tonnes (mnt) in week 38 from 11.88 mnt in week 37, as per provisional BigMint data. Overall market activity remained subdued, though selective stocking at certain ports helped cushion declines in other regions.

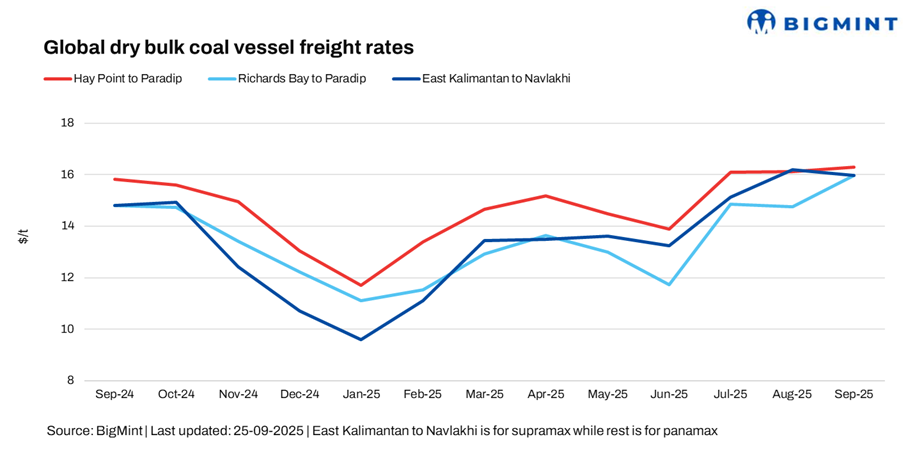

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged down by around 0.38/dry metric tonne (dmt) to $16.50/dmt. India’s imported coking coal market remained less active after aggressive bookings seen last week.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route rose sharply by $2.8/dmt w-o-w to $18/dmt. South Africa–India Panamax freights stayed elevated this week despite limited fresh fixtures, supported by tight vessel supply and firm owner sentiment. Positive cues from other regional routes and expectations of forward demand also kept levels high, even as muted activity limited immediate market movement.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route stood at $14.47/dmt, a significant w-o-w fall of $1.24/dmt. Indonesia-India freights eased this week as trading began on a quiet note across the Pacific basin and Indian Ocean. Market activity on the Indonesia-India coal route remained thin, with limited information available.

Market highlights

- Baltic index faces mixed signals as vessel rates diverge: The Baltic Exchange’s main dry bulk index rose by about 60 points w-o-w to 2,240 on 25 September 2025, supported by firm rates for certain vessels. However, the Panamax segment slipped sharply by 99 points w-o-w to 1,824, and the Supramax segment edged down 9 points w-o-w to around 1,483, reflecting uncertainty among market participants.

- DCE coal futures largely stable w-o-w: Coking coal futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract decreased slightly by RMB 0.15/t ($0.02/t) w-o-w to RMB 214.85/t ($30/t) on 25 September. DCE coal futures remained largely stable on a w-o-w basis, as market sentiment held steady amid moderate trading activity and balanced demand-supply dynamics.

- Brent crude oil futures inch up w-o-w: Brent crude oil futures rose marginally by around $0.54/barrel (bbl) w-o-w to $67.61/bbl, supported by easing concerns over global supply disruptions and slightly stronger-than-expected demand cues from key consuming regions.

Outlook

The near-term outlook for dry bulk coal freights remains mixed across key routes. Rates on the Australia-India and South Africa-India lanes are expected to stay firm, supported by steady demand and limited vessel availability, while the Indonesia-India route may continue to face pressure amid subdued trading and muted industrial activity.

Overall market activity is likely to remain cautious, influenced by uncertainty around regulatory developments, seasonal demand fluctuations, and liquidity constraints. Charterers may continue to adopt a selective approach, keeping upward pressure on freights limited despite occasional short-term spikes.

Leave a Reply