- Australia-India coal freights up; South Africa-India steady, Indonesia-India down

- Near-term outlook cautious, support mainly on Australia-India route

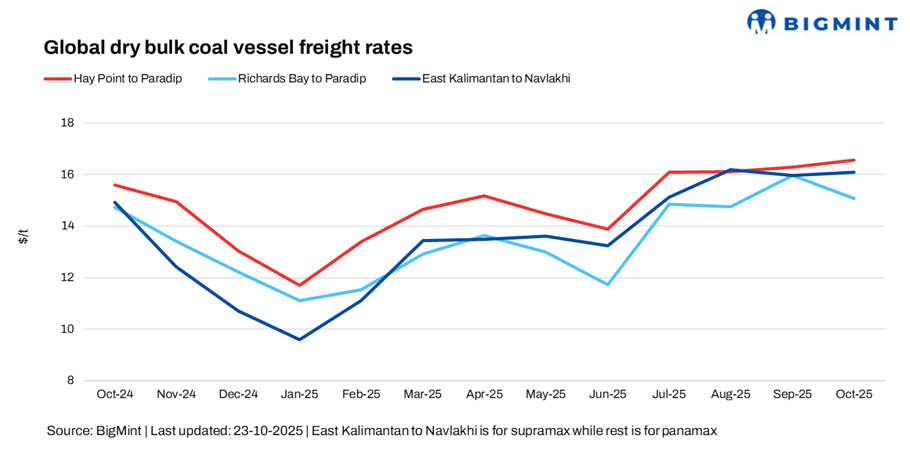

Dry bulk coal freight rates displayed a mixed trend this week amid continued market uncertainty and subdued trading activity. The Indonesia-India route eased slightly, weighed down by limited cargo demand and a lack of fresh fixtures. In contrast, the South Africa-India route inched higher, despite overall chartering activity remaining muted as market participants maintained a cautious, wait-and-see stance. Overall, market sentiment stayed guarded, with soft fundamentals and restrained buying interest keeping freight levels under pressure.

Coal freight rates on the Australia-India route rose this week, driven by active spot demand from Indian steelmakers who booked vessels consistently throughout the week. The upward momentum was reinforced by tighter vessel availability in the Pacific, as repositioning and selective chartering by owners reduced tonnage supply. While overall market sentiment remains cautious, the combination of short-term demand strength and constrained vessel availability supported higher freight levels on the route.

Freight rates on the South Africa-India route inched up slightly w-o-w, despite a continued lack of fresh coal cargo inquiries. Limited trading activity kept the market subdued, with charterers largely on the sidelines amid an uncertain demand outlook and steady vessel availability. Consequently, rate movements remained supportive, reflecting a balanced but inactive market environment.

Supramax freight rates on the Indonesia-India route continued to slide w-o-w. Activity out of the Indian Ocean remained subdued, with muted fresh cargo inquiries and overall market sentiment staying largely flat across most lanes.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up w-o-w by around 0.4/dry metric tonne (dmt) to $17.50/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route rose w-o-w by $0.08/dmt to $14.80/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $15.50/dmt, a w-o-w decrease of $0.69/dmt.

Meanwhile, Brent crude oil futures climbed by about $3.43/barrel to $65.51/bbl on 24 October 2025 compared with 15 October, marking a w-o-w gain driven by renewed supply concerns and improving global risk sentiment. Prices were supported by signs of tighter output from key producers and ongoing geopolitical tensions that stoked fears of potential disruptions. Additionally, expectations of firmer demand from major consuming nations, coupled with a softer U.S. dollar, lent further support to the rally. Overall, market sentiment remained cautiously bullish as traders weighed tightening fundamentals against lingering macroeconomic uncertainties.

Outlook

The near-term outlook for dry bulk coal freights to India remains mixed, with rates likely to stay supported on the Australia-India route due to active steelmaker demand and tighter vessel availability, while South Africa-India and Indonesia-India routes may see limited upside amid muted cargo inquiries and subdued trading activity. Overall, market sentiment is expected to remain cautious, with short-term fluctuations driven by spot demand and repositioning of vessels in key basins.

Leave a Reply