- Pacific coal freight rates firm on steady demand, tighter vessel supply

- Atlantic rates ease amid limited fixtures and ample tonnage

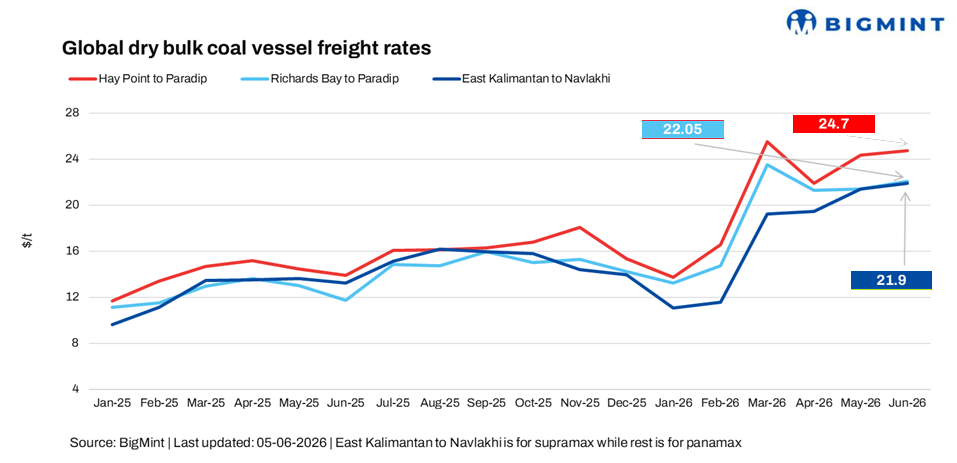

India’s dry bulk coal freight market displayed mixed trends in the week ended 5 June 2026, with Pacific basin routes remaining firm amid steady coal demand from Indian buyers and tighter vessel availability.

In contrast, Atlantic basin freight rates softened slightly due to limited fresh fixture activity and relatively ample tonnage supply, resulting in divergent market sentiment across key coal trade corridors.

A shipbroker said, “The Asia-Pacific Panamax freight market strengthened, supported by improving cargo demand and firmer sentiment. Meanwhile, freight derivatives declined during Asian trading hours, while bunker prices recorded a marginal increase.”

“Asia-Pacific Supramax freight rates were steady to firmer, supported by stable market sentiment, while bunker prices edged up slightly. Activity on the Indonesia-India coal route remained largely subdued, with limited fresh fixtures reported”, another shipbroker mentioned.

Route-wise update

Market highlights

- Baltic Dry Index (BDI) declines w-o-w: The BDI fell by 6% (189 points) w-o-w to 3,037 on 5 June, weighed down by weaker Capesize sentiment. The Panamax index dropped by 3% (77 points) to 2,254, and the Supramax index down by 1% (15 points) to 1,584, supported by steady minor bulk cargo demand.

- Bunker prices increase w-o-w: Bunker prices increased by $30/tonne (t) w-o-w to $792/t as of 5 June, supported by higher crude oil prices and concerns over tightening fuel supply.

- Brent crude futures rise w-o-w: Brent crude oil (August 2026 contract) was assessed at $95/barrel (bbl) on 5 June, up by $2.9/bbl w-o-w, driven by supply-side concerns, geopolitical tensions in key oil-producing regions, and expectations of stronger seasonal fuel demand.

Outlook

Coal freight rates to India are expected to remain firm in the near term, supported by steady import demand, particularly from power utilities and industrial consumers. In the Pacific basin, tighter vessel availability and healthy coal cargo volumes from Indonesia and Australia could lend further support to rates.

However, gains may be capped by cautious chartering activity, ample tonnage in some regions, and uncertainty surrounding global commodity demand.

Leave a Reply